Sequence of Returns Risk: Why Order Matters More Than...

Here's a retirement planning fact that surprises most people:

Two retirees with the same starting balance, same withdrawal rate, and same average return over 20 years can end up with wildly different outcomes—one running out of money while the other dies with millions.

The difference? The order in which those returns happened.

This is called sequence of returns risk (or sequence risk), and it's one of the most important—and least understood—concepts in retirement planning.

The Basic Problem

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →When you're accumulating money (saving for retirement), volatility is annoying but not dangerous. Bad years early on hurt, but you have time to recover.

When you're decumulating money (spending in retirement), everything reverses. Bad years early on are devastating. You're selling shares at low prices to fund your spending, and those shares are gone forever—they can't participate in the recovery.

This asymmetry is sequence risk.

Run your own numbers in the free calculator →

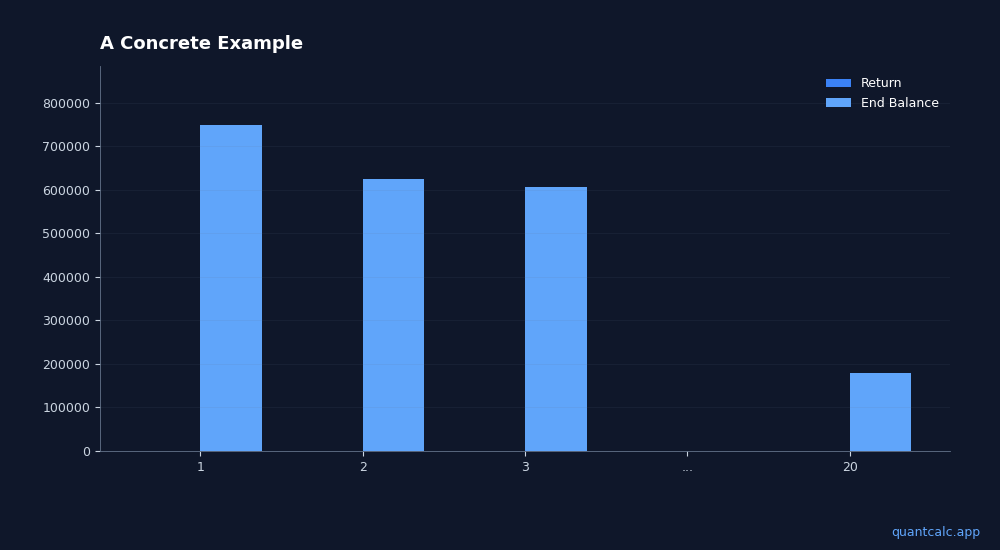

A Concrete Example

Let's compare two retirees:

Setup:

- Starting portfolio: $1,000,000

- Annual withdrawal: $50,000 (5%)

- Time period: 20 years

- Average annual return: 7% for both

Retiree A: Bad Start

| Year | Return | End Balance |

|---|---|---|

| 1 | -20% | $750,000 |

| 2 | -10% | $625,000 |

| 3 | +5% | $606,250 |

| ... | (improving) | ... |

| 20 | $180,000 |

Retiree B: Good Start

| Year | Return | End Balance |

|---|---|---|

| 1 | +20% | $1,150,000 |

| 2 | +15% | $1,272,500 |

| 3 | +10% | $1,349,750 |

| ... | (declining) | ... |

| 20 | $2,400,000 |

Same average return. Same withdrawal rate. One has $180K left. One has $2.4 million.

Why Does This Happen?

When you withdraw money during a down market:

- You sell more shares to get the same dollar amount

- Those shares are no longer in your portfolio

- They can't participate in the eventual recovery

- Your portfolio is permanently smaller

Early returns have an outsized impact because they affect a larger base of assets for a longer time.

The Math: Why Early Years Matter Most

| Year of Return | Impact on Final Wealth |

|---|---|

| Year 1 | Very High |

| Year 2-5 | High |

| Year 6-10 | Moderate |

| Year 11-15 | Lower |

| Year 16-20 | Lowest |

This is why the first 5-10 years of retirement are called the "danger zone."

How to Protect Against Sequence Risk

1. Build a Cash Buffer

Keep 1-3 years of expenses in cash or short-term bonds. During a market downturn, spend from the buffer instead of selling stocks at low prices.

2. Use a Flexible Withdrawal Strategy

Instead of fixed $50,000/year, use dynamic withdrawal strategies with guardrails:

- Normal year: Withdraw 4%

- Market down 15%+: Withdraw 3.5%

- Market up 20%+: Withdraw 4.5%

Any flexibility dramatically improves outcomes.

3. Reduce Equity Allocation Early in Retirement

Some research suggests starting retirement with lower equity (40-50%), then increasing over time (to 60-70%) — a strategy known as a rising equity glide path. Protect when most vulnerable.

4. Delay Social Security

If you can delay Social Security until 70, you get:

- 8% per year increase in benefits (guaranteed return)

- More guaranteed income later when portfolio is potentially depleted

- Less sequence risk exposure in early retirement years

How Monte Carlo Captures Sequence Risk

This is why Monte Carlo simulation matters for retirement planning.

A fixed return calculator assumes 7% every year. It completely ignores sequence risk.

Monte Carlo runs hundreds or thousands of scenarios with different sequences:

- Some start with crashes

- Some start with booms

- Some have crashes in the middle

The "success rate" (e.g., 85%) reflects how many of those sequences survived. A 15% failure rate means 15% of possible return sequences would bankrupt you.

This is exactly what sequence risk looks like in a model.

Testing Your Vulnerability

High Sequence Risk:

- Retiring at an all-time market high

- 80%+ equity allocation

- Fixed withdrawal strategy (the 4% rule alone won't protect you)

- No cash buffer

- No other income sources

Lower Sequence Risk:

- Retiring after a significant market decline

- 50-60% equity allocation

- Flexible withdrawal strategy

- 2-3 year cash buffer

- Social Security or pension covering basic expenses

The Bottom Line

Sequence of returns risk means that the order of market returns matters as much as the average—especially in retirement.

Key takeaways:

- Early retirement years are most vulnerable - Bad returns in years 1-10 can permanently damage a portfolio

- Same average return, different outcomes - Order matters more than average during decumulation

- Flexibility is protection - Ability to reduce spending during downturns is your best defense

- Monte Carlo captures this - Success rates reflect sequence risk; fixed calculators don't

See How Sequence Risk Affects Your Plan

Monte Carlo simulation is the only way to understand sequence risk. QuantCalc runs 1,000+ scenarios with different return sequences and shows you your true probability of success.

Frequently Asked Questions

What is sequence of returns risk?

Sequence of returns risk is the danger that poor market returns in the first few years of retirement will permanently deplete your portfolio, even if long-term average returns are acceptable. A retiree who experiences a 30% crash in year 1 needs a 43% gain just to break even — while simultaneously withdrawing living expenses. This is the primary reason Monte Carlo simulation matters more than average return assumptions.

How can I protect my retirement portfolio from sequence of returns risk?

Three main strategies: (1) Hold 2-3 years of expenses in cash or short-term bonds as a withdrawal buffer, so you never sell equities during a crash. (2) Use dynamic withdrawal strategies that reduce spending 10-15% during market downturns. (3) Build a bond tent — temporarily increasing bond allocation to 50-60% in the 5 years before and after retirement, then gradually shifting back to equities.

Frequently Asked Questions

Sequence of returns risk is the danger that poor market returns in the first few years of retirement will permanently deplete your portfolio, even if long-term average returns are acceptable. A retiree who experiences a 30% crash in year 1 needs a 43% gain just to break even — while simultaneously withdrawing living expenses. This is the primary reason Monte Carlo simulation matters more than average return assumptions.

Three main strategies: (1) Hold 2-3 years of expenses in cash or short-term bonds as a withdrawal buffer, so you never sell equities during a crash. (2) Use dynamic withdrawal strategies that reduce spending 10-15% during market downturns. (3) Build a bond tent — temporarily increasing bond allocation to 50-60% in the 5 years before and after retirement, then gradually shifting back to equities.