Sequence of Returns Risk: The Retirement Killer No One Talks About

Sequence of returns risk is the danger that poor market returns in the first 5-10 years of retirement deplete a portfolio before it can recover, even when long-term average returns are identical. Two retirees with the same $1M portfolio, $40,000 annual withdrawals, and 8% average return can end with $2.8M remaining or run out of money in year 23 — purely from the order of returns. Historical analysis shows a 40-60% outcome gap between lucky and unlucky retirees. See your own risk at quantcalc.app.

Two retirees. Same portfolio size. Same withdrawal strategy. Same average market returns over 30 years.

One dies with $3 million. The other runs out of money at age 80.

What made the difference? Sequence of returns risk—the single most dangerous threat to retirement security that almost no one understands until it's too late.

This guide will show you exactly what sequence risk is, why it can destroy even well-funded retirements, and—most importantly—how to protect yourself before it's too late.

What is Sequence of Returns Risk?

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →Sequence of returns risk is the danger that bad investment returns early in retirement will deplete your portfolio before markets can recover, even if long-term average returns are strong.

The math: When you're withdrawing money regularly, the ORDER of returns matters just as much as the AVERAGE return.

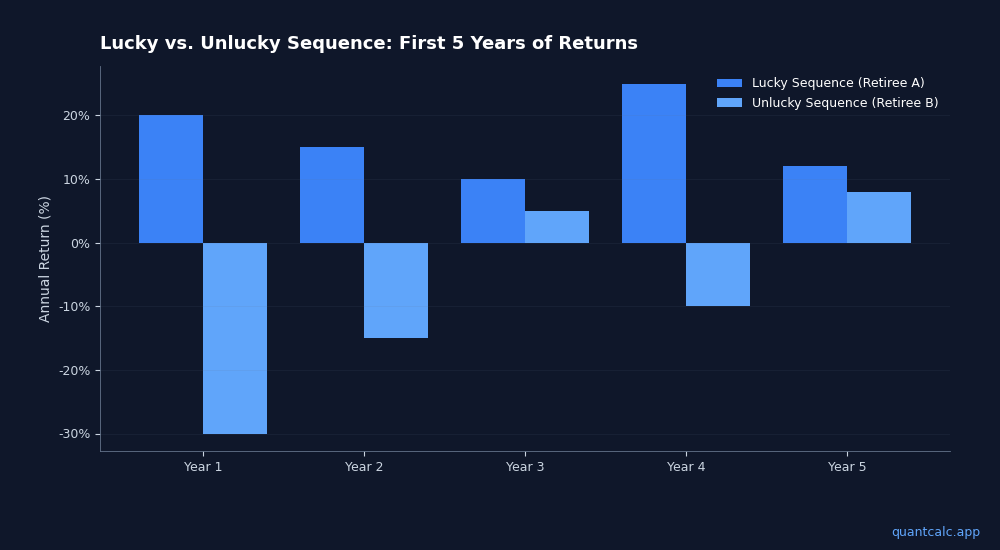

Example:

Retiree A (lucky sequence):

- Year 1-5: +20%, +15%, +10%, +25%, +12% (strong start)

- Year 6-30: Mix of ups and downs

- 30-year average: 8%

- Outcome: $2.8M remaining

Retiree B (unlucky sequence):

- Year 1-5: -30%, -15%, +5%, -10%, +8% (terrible start)

- Year 6-30: Strong recovery (same returns as Retiree A, just reversed)

- 30-year average: 8% (same as Retiree A!)

- Outcome: $0 remaining at year 23 (ran out of money)

Same average returns. Completely different outcomes. This is sequence risk.

Run your own numbers in the free calculator →

Why Early Returns Matter So Much in Retirement

During accumulation (your working years), sequence doesn't matter much. Whether you experience -30% in year 1 or year 20 of saving, you end up roughly the same—you're buying shares at different prices, which averages out.

But in retirement, you're SELLING shares to fund withdrawals. And selling into a crash is permanently destructive.

The mechanics:

Bad scenario (crash early):

- Start: $1M portfolio, withdraw $40k/year

- Year 1: Market drops 30% → portfolio now $700k

- You still withdraw $40k → down to $660k

- Market needs to gain 52% just to get back to $1M

- Meanwhile you're withdrawing $40k+ every year

- The hole gets deeper and deeper

Good scenario (crash later):

- Start: $1M portfolio, withdraw $40k/year

- Years 1-10: Strong markets, portfolio grows to $1.8M despite withdrawals

- Year 11: Market drops 30% → portfolio falls to $1.26M

- You still have a $1.26M cushion—plenty of room to recover

The difference: In the first 5-10 years of retirement, your portfolio is most vulnerable. Big losses early create a "hole" you can never climb out of, because you're taking withdrawals the entire time.

Real-World Example: 2000 vs. 2009 Retirees

Retiree who started in 2000:

- Experienced the dot-com crash immediately (2000-2002: -10%, -12%, -22%)

- Then 2008 financial crisis (2008: -37%)

- Despite two brutal crashes in first decade, anyone who withdrew 4% and stuck to their plan ran out of money or came dangerously close by 2020

- Why? The double-whammy of crashes while taking withdrawals was devastating

Retiree who started in 2009:

- Started right after the 2008 crash (perfect timing, though unintentional)

- Experienced the entire 2009-2020 bull market during critical early years

- Portfolio more than doubled despite taking 4% withdrawals

- COVID crash in 2020 barely dented their wealth

Same retirement strategies, but 9 years of starting date difference = completely different financial security.

How Big is the Risk?

Historical analysis shows sequence risk can cause a 40-60% difference in retirement outcomes between "lucky" and "unlucky" retirees with identical portfolios and withdrawal strategies.

Monte Carlo simulations (which test thousands of return sequences) consistently show:

- 4% withdrawal rate: ~85-95% success rate

- Meaning: 5-15% of retirees run out of money NOT because the strategy is bad, but because they got unlucky with return sequence

The retirees who fail aren't doing anything wrong—they just retired at the wrong time.

When Are You Most Vulnerable?

Sequence risk is highest in three situations:

1. Early Retirement (First 5-10 Years)

The "fragile decade"—a 30% market drop in year 3 of retirement is far more damaging than the same drop in year 20.

Why: Your portfolio is at its largest (you haven't spent much yet), so dollar losses are biggest. And you have many withdrawal years ahead where you're "selling low" continuously.

2. High Withdrawal Rates

- 3% withdrawal rate: Sequence risk is minimal (even bad sequences rarely cause failure)

- 5% withdrawal rate: Sequence risk is HUGE (bad sequences almost always cause failure)

Higher withdrawals mean you're selling more shares during downturns, deepening the hole.

3. Aggressive Portfolios (High Stock Allocation)

- 100% stocks: Maximum sequence risk (highest volatility)

- 50/50 stocks/bonds: Moderate sequence risk

- 30/70 stocks/bonds: Lower sequence risk (but lower growth)

The trade-off: Stocks have higher long-term returns but create more sequence risk. Bonds provide stability during crashes but lower long-term growth.

Strategy 1: The Bond Tent (Rising Equity Glide Path)

One of the most effective defenses against sequence risk is temporarily reducing stock exposure in early retirement, then increasing it later.

How it works:

Years 1-5 (high vulnerability):

- 40-50% stocks, 50-60% bonds

- Lower volatility = less damage if crash occurs

- Bonds provide cash for withdrawals, avoiding selling stocks at low prices

Years 6-15 (transition):

- Gradually increase stocks to 60-70%

- Market has (hopefully) recovered from early crashes

- You've survived the fragile decade

Years 16+ (lower vulnerability):

- 70-80% stocks

- Portfolio needs growth to last 30+ years

- Less worried about sequence risk (portfolio has aged, less money left)

This is called a "bond tent" because bond allocation is highest at retirement, then declines—shaped like a tent.

Research: Studies show bond tents increase success rates by 5-10 percentage points compared to static allocations.

(Deep dive on glide path strategies)

Strategy 2: Dynamic Spending (Guardrails)

Instead of withdrawing a fixed percentage regardless of market conditions, adjust spending based on portfolio performance.

How it works:

- Set withdrawal "guardrails" (upper and lower bounds)

- If portfolio drops below lower guardrail (e.g., 80% of expected value): Cut spending by 10%

- If portfolio exceeds upper guardrail (e.g., 130% of expected value): Increase spending by 10%

Why it works: By cutting spending during downturns, you sell fewer shares at depressed prices. This preserves capital and allows recovery when markets rebound.

Example:

- Planned spending: $50k/year

- Market crashes 35% in year 2

- Guardrail triggers: Cut spending to $45k

- You now sell 15% fewer shares during the crash

- Portfolio recovers faster when market rebounds

Trade-off: Less predictable spending. But sequence risk is a bigger threat to retirement security than minor lifestyle adjustments.

(Full guide to dynamic withdrawal strategies)

Strategy 3: Build a Cash Buffer

Keep 1-3 years of expenses in cash or short-term bonds. During market crashes, live off this buffer instead of selling stocks at low prices.

How it works:

- Portfolio: $1M total

- Buffer: $120k in cash (3 years of $40k expenses)

- Invested assets: $880k in 70/30 stocks/bonds

During normal markets:

- Withdraw from invested portfolio, refill buffer annually

During crashes:

- Stop withdrawals from invested portfolio

- Live off buffer for 1-3 years

- Allows stocks to recover without selling at the bottom

Why it works: By avoiding forced selling during crashes, you eliminate the most damaging aspect of sequence risk.

Cost: Cash earns lower returns (~3% vs. 7%+ for stocks), so this creates a small long-term drag. But the insurance value outweighs the cost.

Strategy 4: Flexible Spending (The Ultimate Defense)

The retirees least vulnerable to sequence risk are those with highly flexible spending.

Core concept:

- Fixed essential expenses (housing, food, healthcare): Covered by guaranteed income (Social Security, pensions, annuities)

- Discretionary expenses (travel, dining, hobbies): Funded by portfolio withdrawals

During crashes:

- Essential expenses are protected (guaranteed income doesn't fluctuate)

- Cut discretionary spending by 20-50% temporarily

- Resume normal spending when markets recover

Example:

- Essential expenses: $35k/year (covered by Social Security)

- Discretionary: $25k/year (from portfolio)

- Crash year: Cut discretionary to $15k

- Effective withdrawal rate drops from 4.8% to 4%

This flexibility is the difference between running out of money and surviving indefinitely.

Strategy 5: Delay Retirement (Or Work Part-Time)

Brutal honesty: If markets crash right before your planned retirement, delaying by 1-2 years can dramatically improve your long-term outcome.

The math:

- Delaying 1 year = 1 extra year of portfolio growth WITHOUT withdrawals

- Plus 1 more year of contributions

- Plus 1 fewer year of withdrawals

- Net effect: ~5% increase in starting portfolio size

For a $1M portfolio retiring at 4% withdrawal:

- Original plan: $1M, withdraw $40k/year

- Delay 1 year: $1.05M+, withdraw $40k/year (same dollar amount, lower percentage)

- Success probability increases by ~8-10 percentage points

Alternative: Retire as planned but work part-time for 2-3 years earning $20-30k. This reduces portfolio withdrawals during the fragile decade.

Strategy 6: Annuity Floor for Essential Expenses

Eliminate sequence risk for your baseline expenses by purchasing an immediate annuity (or delaying Social Security to maximize benefits).

How it works:

- Essential expenses: $40k/year

- Social Security: $25k/year

- Gap: $15k/year

- Solution: Buy immediate annuity paying $15k/year for life (costs ~$300k at age 65)

- Result: Zero sequence risk for essentials (guaranteed regardless of markets)

- Remaining portfolio ($700k): Invested aggressively for discretionary spending

Why it works: Annuities transfer sequence risk to an insurance company. They guarantee income regardless of market returns.

Trade-off: Annuities are expensive, irreversible, and reduce legacy (you can't leave the principal to heirs).

(Learn more about floor-and-ceiling strategies)

Testing Your Sequence Risk Exposure

You can't eliminate sequence risk entirely, but you can quantify it and reduce it.

Use Monte Carlo simulation to model your retirement across thousands of return sequences:

- What's your success rate with current plan?

- What's your worst-case outcome (5th percentile)?

- How sensitive are you to early crashes?

Key outputs:

- Success rate: Higher = less sequence risk

- Percentile spread: Narrow spread (10th to 90th percentile) = lower sequence risk, wide spread = high risk

- Failure timing: Do failures happen in years 5-15 (sequence risk) or years 25-30 (longevity risk)?

Adjustments to test:

- Lower withdrawal rate (4% → 3.5%): How much does success rate improve?

- Bond tent (reduce stocks early): Does this help enough to justify lower growth?

- Cash buffer: Does 2 years of expenses in cash meaningfully reduce ruin probability?

QuantCalc's Monte Carlo planner runs up to 10,000 simulations showing:

- Success rate across all sequences

- Distribution of outcomes (best case, worst case, median)

- Sensitivity to early market crashes

- Impact of different asset allocations and withdrawal strategies

You'll see exactly how vulnerable you are and which mitigation strategies work best for your situation.

The Bottom Line: You Can't Control Markets, But You Can Control Your Risk

Sequence of returns risk is real, it's dangerous, and it's random—you can't predict whether you'll retire at a lucky time or unlucky time.

But you can structure your retirement to survive bad luck:

- Reduce stock exposure in early years (bond tent)

- Build spending flexibility (guardrails, discretionary cuts)

- Maintain a cash buffer (avoid forced selling)

- Stress-test with Monte Carlo (model the worst cases)

The retirees who run out of money aren't the ones who saved too little—they're the ones who got unlucky AND didn't have a plan to handle bad sequences.

Don't let sequence risk destroy your retirement. Test your plan across thousands of scenarios before you commit.

Ready to stress-test your retirement? Run a Monte Carlo analysis with QuantCalc and see how your plan handles bad market sequences.

Further Reading:

- Retirement Asset Allocation by Age: The Glide Path Strategy

- Retirement Spending Strategies: Beyond the 4% Rule

- What is Monte Carlo Simulation for Retirement Planning?

Frequently Asked Questions

What is sequence of returns risk?

Sequence risk is the danger that poor market returns early in retirement deplete your portfolio before it can recover, even if long-term average returns are good.

Why does sequence risk matter more in retirement?

Because you're withdrawing money during downturns instead of adding to the portfolio, locking in losses and reducing future compound growth.

How do you protect against sequence risk?

Dynamic withdrawal strategies, cash buffers, glide path allocation shifts, and stress testing your portfolio against historical bear markets.

Frequently Asked Questions

Sequence risk is the danger that poor market returns early in retirement deplete your portfolio before it can recover, even if long-term average returns are good.

Because you're withdrawing money during downturns instead of adding to the portfolio, locking in losses and reducing future compound growth.

Dynamic withdrawal strategies, cash buffers, glide path allocation shifts, and stress testing your portfolio against historical bear markets.