The Withdrawal-Order Traps That Silently Cost Retirees

Retirement planning isn't just about accumulating wealth—it's about keeping more of what you've saved. The difference between a tax-efficient withdrawal strategy and a haphazard approach can cost you hundreds of thousands of dollars over a 30-year retirement.

Most retirees leave money on the table because they withdraw from their accounts in the wrong order, push themselves into higher tax brackets unnecessarily, or trigger penalties they could have avoided. This guide will show you exactly how to structure your withdrawals to minimize your lifetime tax bill.

Why Withdrawal Strategy Matters More Than You Think

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →Check your MAGI ceiling before contributing to your IRA. A single dollar over 400% FPL can trigger full ACA subsidy repayment.

Check Your MAGI Ceiling Now

Consider two retirees, both with $2 million in savings. One withdraws randomly from whatever account is convenient. The other uses a tax-optimized sequence. After 25 years, the strategic retiree could have $300,000 to $500,000 more in after-tax wealth—simply by being smart about which accounts to tap and when.

The stakes are even higher in 2026 because of:

- The ACA subsidy cliff (more on this below)

- IRMAA surcharges on Medicare premiums

- Pending changes to RMD ages

- State tax considerations for retirees

Run your own numbers in the free calculator →

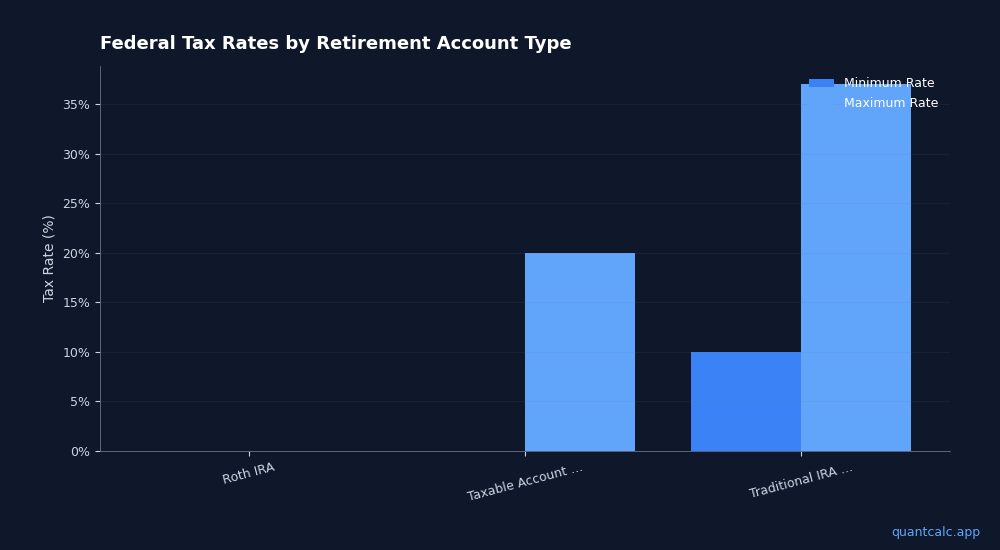

The Three Account Types and How They're Taxed

Before building your strategy, understand how each account type is taxed:

Taxable Accounts (Brokerage)

- Dividends and interest taxed annually

- Capital gains taxed when you sell

- Long-term capital gains rates (0%, 15%, or 20%) are usually lower than ordinary income rates

- Most flexible—no penalties, no required distributions

Tax-Deferred Accounts (Traditional IRA, 401k)

- No taxes while money grows

- Withdrawals taxed as ordinary income (10%-37% federal)

- Required Minimum Distributions (RMDs) start at age 73 (as of 2026)

- Early withdrawal penalties before age 59½ (with exceptions)

Tax-Free Accounts (Roth IRA, Roth 401k)

- Contributions made with after-tax dollars

- Withdrawals in retirement are 100% tax-free

- No RMDs during owner's lifetime

- Greatest flexibility and tax advantage

The Standard Withdrawal Sequence (And Why It's Wrong)

Financial advisors often recommend withdrawing in this order:

- Taxable accounts first

- Tax-deferred accounts second

- Roth accounts last

The logic: preserve tax-advantaged growth as long as possible, leave Roth for emergencies or heirs.

The problem: This one-size-fits-all approach ignores your specific tax situation and misses massive optimization opportunities.

The Optimal Withdrawal Strategy: A Dynamic Approach

The best strategy isn't static—it changes based on your age, income, tax bracket, and legislative environment. Here's the framework:

Phase 1: Early Retirement (Before Age 59½)

If you retire early, you need cash flow without the 10% early withdrawal penalty. Your options:

Roth Conversion Ladder

Convert traditional IRA money to Roth IRA. After 5 years, you can withdraw the converted principal penalty-free. This requires planning 5 years ahead but provides tax-free income later.

72(t) SEPP Withdrawals

Take "substantially equal periodic payments" from your IRA based on IRS calculations. No penalty, but you must continue for 5 years or until age 59½, whichever is longer.

Taxable Account Harvesting

Live off your brokerage account while doing Roth conversions in low-tax years. Harvest capital gains at the 0% rate if your income allows (up to $89,250 married filing jointly in 2026).

Phase 2: The Gap Years (Age 59½ to 73)

This is your golden window for tax optimization. You can access all accounts penalty-free but aren't forced to take RMDs yet.

Fill Your Tax Bracket

Deliberately take traditional IRA withdrawals to "fill up" the 12% or 22% bracket, even if you don't need the cash. Why? Because RMDs later might push you into 24% or higher.

Roth Conversions

Convert traditional IRA money to Roth up to the top of your target bracket. Yes, you pay taxes now—but you're paying at 12% or 22% instead of 24% or 32% later.

Manage MAGI for ACA Subsidies

If you're under 65 and buying health insurance on the ACA marketplace, keep your Modified Adjusted Gross Income (MAGI) below 400% of the Federal Poverty Level to avoid the subsidy cliff. In 2026, that's about $60,000 for singles or $81,000 for couples. (Learn more about optimizing ACA subsidies)

Strategic Roth Withdrawals

Since Roth withdrawals don't count as income, use them to cover expenses in years when you're doing large Roth conversions or managing MAGI.

Phase 3: RMD Years (Age 73+)

Once RMDs kick in, you lose some control—but you can still optimize.

QCDs (Qualified Charitable Distributions)

If you're charitably inclined, donate directly from your IRA (up to $111,000 in 2026). This satisfies your RMD but doesn't count as taxable income.

IRMAA Management

Medicare Part B and D premiums have income-based surcharges (IRMAA). These kick in at $109,000 (single) or $218,000 (married) MAGI. Time your capital gains and Roth conversions to avoid pushing yourself over the threshold.

Spend Down Traditional First

By now, your Roth accounts should be substantial from earlier conversions. Use traditional IRA withdrawals to meet RMDs and living expenses, preserve Roth for later years (or heirs, since Roth IRAs pass tax-free).

Advanced Tactics: Taking It to the Next Level

Tax-Loss Harvesting

Sell losing positions in your taxable account to offset capital gains (and up to $3,000 of ordinary income per year). Carryforward unused losses indefinitely.

Asset Location Optimization

Hold tax-inefficient investments (bonds, REITs) in tax-deferred accounts. Hold tax-efficient investments (index funds, municipal bonds) in taxable accounts. This can add 0.2%-0.5% annual returns through tax savings alone.

State Tax Arbitrage

Some states don't tax retirement income (Social Security, pensions, even IRA withdrawals in states like Mississippi or Pennsylvania). If you're planning to move in retirement, time large withdrawals or Roth conversions for after your move.

Bracket Arbitrage

If you know you'll have a low-income year (sabbatical, career transition, business loss), accelerate income into that year through Roth conversions or harvesting gains at 0%.

How to Model Your Personal Strategy

Every retirement is different. Your optimal strategy depends on:

- Account balances across taxable, tax-deferred, and Roth

- Current age and retirement timeline

- Expected longevity

- Spending needs (fixed vs. flexible)

- Tax bracket now vs. expected bracket in retirement

- State tax situation

- Legacy goals

The only way to truly optimize is to model multiple scenarios using Monte Carlo simulation, which accounts for market uncertainty, sequence of returns risk, and changing tax laws.

QuantCalc lets you model tax-efficient withdrawal strategies with up to 10,000 Monte Carlo simulations. You can compare different withdrawal sequences, test Roth conversion scenarios, and see how taxes impact your probability of success over 30+ year retirements.

Common Mistakes to Avoid

Ignoring Roth conversions entirely

"I don't want to pay taxes now" is emotional, not rational. Paying 12% now beats paying 24% later.

Converting too much too fast

Roth conversions make sense—until they push you into a higher bracket or trigger IRMAA. Model the break-even point.

Forgetting about state taxes

Federal optimization is useless if you're paying 13% California state tax. Some strategies (like QCDs) save federal but not state taxes.

Withdrawing from Roth too early

Your Roth is your most valuable asset. Don't drain it in your 60s when you could use it to avoid RMDs in your 80s.

Not updating your plan

Tax laws change. Your spending changes. Your health changes. Review your strategy annually.

Action Steps: Build Your Plan Today

- Inventory your accounts — How much is in taxable, tax-deferred, and Roth?

- Estimate your tax bracket — Both now and in retirement (factor in Social Security, pensions, RMDs)

- Model different scenarios — What if you convert $50k/year to Roth? What if you delay Social Security? What if markets crash early?

- Stress-test with Monte Carlo — Don't rely on average returns. See your probability of success across thousands of potential market scenarios.

- Review annually — Adjust based on market performance, tax law changes, and life circumstances.

Tax-efficient withdrawal isn't about perfectly timing the market—it's about keeping more of what you've earned by being strategic about which accounts you tap and when. The difference between good and great execution is often $250,000+ in after-tax wealth over a retirement.

Ready to optimize your withdrawal strategy? Try QuantCalc's Monte Carlo retirement planner to model your personal tax situation across thousands of market scenarios.

Frequently Asked Questions

What is the most tax-efficient order to withdraw retirement funds?

The conventional wisdom is to withdraw from taxable accounts first, then tax-deferred (Traditional IRA/401k), then tax-free (Roth) last. However, the optimal order depends on your specific situation — ACA subsidy eligibility, IRMAA thresholds, Roth conversion opportunities, and state taxes can all change the best sequence.

Should I do Roth conversions before taking Social Security?

Often yes. The years between retirement and Social Security (or age 72 for RMDs) are typically your lowest-income years. Converting Traditional IRA money to Roth during this window can fill low tax brackets cheaply, reduce future RMDs, and keep your MAGI low enough to qualify for ACA subsidies.

What is the tax torpedo in retirement?

The tax torpedo occurs when rising income (from RMDs, Social Security, or other sources) pushes you into a zone where up to 85% of Social Security becomes taxable. This creates an effective marginal tax rate of 40-50% on the next dollar of income. Strategic withdrawals and Roth conversions can help you avoid this trap.

How do IRMAA surcharges affect retirement withdrawals?

IRMAA (Income-Related Monthly Adjustment Amount) adds surcharges to Medicare Parts B and D premiums when your MAGI exceeds certain thresholds. In 2026, the first IRMAA tier starts at $109,000 for single filers. A single dollar over the threshold can increase your Medicare premiums by $1,000+ per year. Withdrawal planning must account for these cliff effects.

Can tax-loss harvesting help in retirement?

Yes. Harvesting losses in taxable accounts can offset capital gains and up to $3,000 of ordinary income per year. For early retirees managing ACA subsidies, tax-loss harvesting directly reduces MAGI, potentially saving thousands in subsidy clawbacks. The key is maintaining your target allocation while harvesting — buy a similar (not identical) fund to avoid wash sale rules.

What is the best withdrawal strategy for early retirees before age 59.5?

Before 59.5, you cannot access 401(k) or IRA funds without a 10% penalty unless you use specific exceptions: Rule of 55 (employer plans), 72(t) SEPP distributions, or Roth contribution basis withdrawals. Most early retirees bridge the gap with taxable brokerage accounts while doing strategic Roth conversions in low-income years.

Further Reading:

- ACA Subsidy Cliff 2026: How to Optimize Your Retirement Income

- MAGI Optimization in Retirement: Lower Your Taxes and Keep Your Benefits

- Roth Conversion Ladder Strategy: A Step-by-Step Guide

Frequently Asked Questions

The conventional wisdom is to withdraw from taxable accounts first, then tax-deferred (Traditional IRA/401k), then tax-free (Roth) last. However, the optimal order depends on your specific situation — ACA subsidy eligibility, IRMAA thresholds, Roth conversion opportunities, and state taxes can all change the best sequence.

Often yes. The years between retirement and Social Security (or age 72 for RMDs) are typically your lowest-income years. Converting Traditional IRA money to Roth during this window can fill low tax brackets cheaply, reduce future RMDs, and keep your MAGI low enough to qualify for ACA subsidies.

The tax torpedo occurs when rising income (from RMDs, Social Security, or other sources) pushes you into a zone where up to 85% of Social Security becomes taxable. This creates an effective marginal tax rate of 40-50% on the next dollar of income. Strategic withdrawals and Roth conversions can help you avoid this trap.

IRMAA (Income-Related Monthly Adjustment Amount) adds surcharges to Medicare Parts B and D premiums when your MAGI exceeds certain thresholds. In 2026, the first IRMAA tier starts at $109,000 for single filers. A single dollar over the threshold can increase your Medicare premiums by $1,000+ per year. Withdrawal planning must account for these cliff effects.

Yes. Harvesting losses in taxable accounts can offset capital gains and up to $3,000 of ordinary income per year. For early retirees managing ACA subsidies, tax-loss harvesting directly reduces MAGI, potentially saving thousands in subsidy clawbacks. The key is maintaining your target allocation while harvesting — buy a similar (not identical) fund to avoid wash sale rules.

Before 59.5, you cannot access 401(k) or IRA funds without a 10% penalty unless you use specific exceptions: Rule of 55 (employer plans), 72(t) SEPP distributions, or Roth contribution basis withdrawals. Most early retirees bridge the gap with taxable brokerage accounts while doing strategic Roth conversions in low-income years.