The 4% Rule Is Wrong (Here's What to Use Instead)

The 4% rule is simple: withdraw 4% of your portfolio in year one, adjust for inflation each year, and you won't run out of money for 30 years.

It's also dangerously misleading.

Where the 4% Rule Came From

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →In 1994, financial planner William Bengen analyzed historical returns going back to 1926. He found that a 4% initial withdrawal rate survived every 30-year period in his dataset.

The study was groundbreaking. But it was also backward-looking, US-only, and based on a specific bond/stock allocation.

Run your own numbers in the free calculator →

The Three Problems With the 4% Rule

Problem 1: It gives you a single number, not a probability

The 4% rule says "this worked historically." It doesn't tell you the odds it will work for your retirement.

A Monte Carlo simulation might show that 4% has an 87% success rate given current market assumptions. That's useful information. "It worked before" is not.

Problem 2: Historical returns may not repeat

The 4% rule was tested on a period that included:

- Post-WWII economic boom

- 1980s-90s bull market

- Falling interest rates from 15% to near zero

Major asset managers publish forward-looking forecasts that typically project 4-7% nominal for US equity over the next decade — meaningfully below the 10% historical average. See our overview of published forecasts. If they're right, historical safe withdrawal rates don't apply.

Problem 3: It ignores sequence of returns risk

Two retirees can have identical average returns and completely different outcomes. If your portfolio drops 30% in year one of retirement, a 4% withdrawal becomes a 5.7% withdrawal from your reduced balance. This is sequence of returns risk in action.

The 4% rule assumes average returns. Retirement happens in specific sequences.

What to Use Instead

Probability-based planning with Monte Carlo simulation.

Instead of asking "did this work before?" ask "what are the odds this works given realistic assumptions?"

A Monte Carlo simulation runs thousands of possible market scenarios—good years, bad years, crashes, recoveries—and tells you what percentage of those scenarios leave you with money at the end.

This gives you:

- A success probability (e.g., 87% chance of not running out)

- Range of outcomes (best case, worst case, median)

- Ability to test different withdrawal rates and see the tradeoff

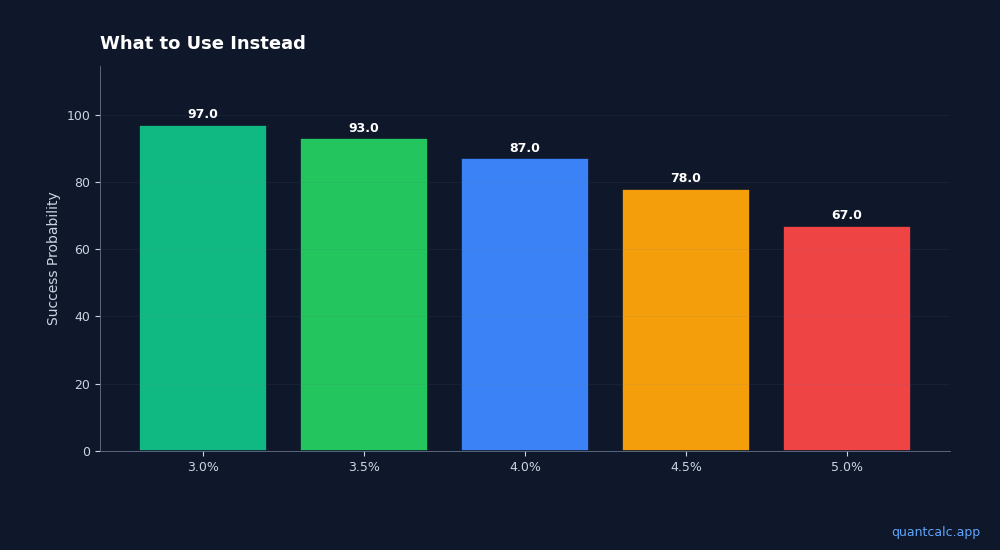

Example:

| Withdrawal Rate | Success Probability |

|---|---|

| 3.0% | 97% |

| 3.5% | 93% |

| 4.0% | 87% |

| 4.5% | 78% |

| 5.0% | 67% |

Now you can make an informed decision. Maybe 87% is acceptable to you. Maybe you want 95%+ and will withdraw less. The point is you know the odds.

The Bottom Line

The 4% rule isn't useless—it's a reasonable starting point. But treating it as a guarantee is a mistake.

Your retirement plan deserves better than "this worked for people who retired in 1966." It deserves a probability.

Know Your Actual Odds

Run Monte Carlo simulations with published assumptions from BlackRock, Vanguard, and JPMorgan. See your probability of success, not just a historical rule.

Frequently Asked Questions

What are the biggest problems with the 4% rule?

The 4% rule assumes fixed spending, a 30-year horizon, and historical US market returns. It ignores taxes, healthcare costs, inflation spikes, and sequence of returns risk. For early retirees with 40-50 year horizons, the 4% rule can overstate safety by 15-20%. Monte Carlo simulation with forward-looking return forecasts provides a more realistic probability of success.

Is the 4% rule still valid in 2026?

Major asset managers project lower returns for the next decade — Vanguard forecasts 4.2-6.2% for US equities vs the historical 10% average. With lower expected returns, a 4% withdrawal rate has roughly a 75-80% success probability over 30 years, down from the original 95%. Many financial planners now recommend 3.3-3.5% for early retirees.

What should I use instead of the 4% rule?

Monte Carlo simulation tests your plan against thousands of possible market scenarios, giving you a probability of success rather than a single number. Dynamic withdrawal strategies (guardrails, variable percentage) adjust spending based on portfolio performance. Tools like QuantCalc run 10,000 simulations using forward-looking published forecasts rather than relying solely on historical data.

Frequently Asked Questions

The 4% rule assumes fixed spending, a 30-year horizon, and historical US market returns. It ignores taxes, healthcare costs, inflation spikes, and sequence of returns risk. For early retirees with 40-50 year horizons, the 4% rule can overstate safety by 15-20%. Monte Carlo simulation with forward-looking return forecasts provides a more realistic probability of success.

Major asset managers project lower returns for the next decade — Vanguard forecasts 4.2-6.2% for US equities vs the historical 10% average. With lower expected returns, a 4% withdrawal rate has roughly a 75-80% success probability over 30 years, down from the original 95%. Many financial planners now recommend 3.3-3.5% for early retirees.

Monte Carlo simulation tests your plan against thousands of possible market scenarios, giving you a probability of success rather than a single number. Dynamic withdrawal strategies (guardrails, variable percentage) adjust spending based on portfolio performance. Tools like QuantCalc run 10,000 simulations using forward-looking published forecasts rather than relying solely on historical data.