Glide Path Optimization: How to Adjust Your Allocation...

"100 minus your age in stocks" is terrible advice. Here's why—and what actually works.

What Is a Glide Path?

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →A glide path is how your asset allocation changes over time. Instead of a static 60/40 portfolio forever, you adjust the mix as you approach and move through retirement.

Target date funds use glide paths. So do smart retirees.

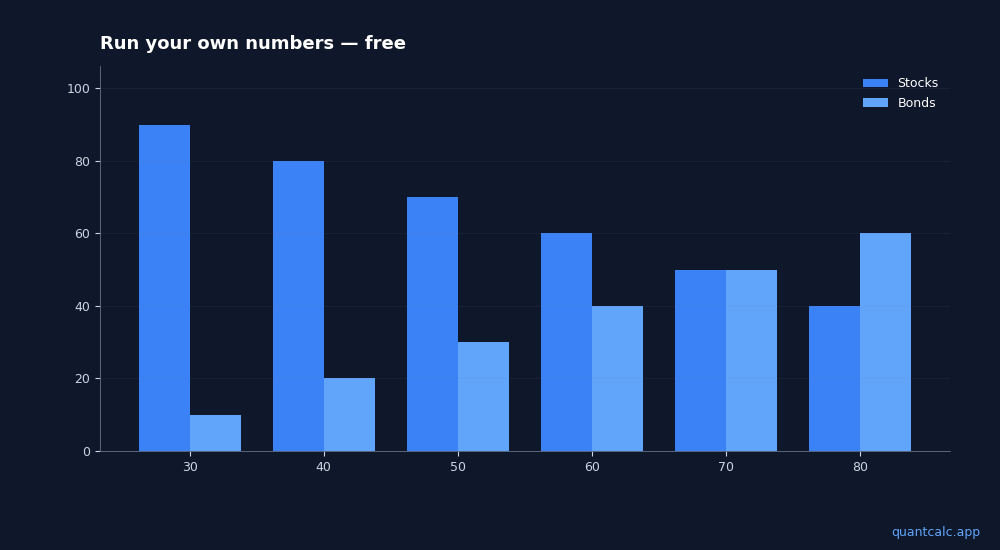

Example glide path:

| Age | Stocks | Bonds |

|---|---|---|

| 30 | 90% | 10% |

| 40 | 80% | 20% |

| 50 | 70% | 30% |

| 60 | 60% | 40% |

| 70 | 50% | 50% |

| 80 | 40% | 60% |

The logic: reduce risk as you have less time to recover from crashes. For more on how to think about asset allocation at different life stages, the key is matching risk to your time horizon.

But this conventional wisdom has a problem.

Run your own numbers in the free calculator →

The "100 Minus Age" Problem

The standard declining glide path (more conservative as you age) actually increases your chance of running out of money.

Why? Sequence of returns risk cuts both ways.

A crash early in retirement is devastating. But so is being too conservative when you're 80 and might live another 20 years.

Research by Wade Pfau and Michael Kitces found that a rising equity glide path—starting conservative and becoming more aggressive—actually improved success rates in many scenarios.

Three Glide Path Strategies

1. Declining (Traditional)

- Start aggressive, end conservative

- 90% to 40% stocks over time

- Intuitive but not always optimal

2. Static

- Maintain same allocation throughout

- e.g., 60/40 forever

- Simple but ignores sequence risk

3. Rising (Research-Backed)

- Start conservative at retirement

- Increase stocks over time

- 40% to 70% stocks

- Counter-intuitive but often superior — also known as a bond tent strategy

Why rising works:

If you retire with 40% stocks and the market crashes in year 1, you lose less. Then you gradually increase stocks when your portfolio has survived the danger zone.

If the market does well early, you miss some upside—but you were never at risk of the worst-case scenario.

How to Find Your Optimal Glide Path

The "best" glide path depends on:

- Your retirement length

- Withdrawal rate

- Expected returns and volatility

- Risk tolerance

Monte Carlo simulation can test different glide paths and show which one maximizes your success probability.

Example comparison:

| Glide Path | 30-Year Success Rate |

|---|---|

| Static 60/40 | 82% |

| Declining 80 to 40 | 79% |

| Rising 40 to 70 | 87% |

In this scenario, the rising glide path wins—but your numbers might be different depending on assumptions.

Implementing a Glide Path

Option 1: Target Date Fund

Vanguard, Fidelity, and Schwab offer target date funds with built-in glide paths. Easy but inflexible—you get their glide path, not one optimized for your situation.

Option 2: Manual Rebalancing

Set calendar reminders to adjust allocation annually. Check your target, rebalance, done.

Option 3: Optimization Tool

Use a calculator that can test multiple glide paths against Monte Carlo simulation. Find the one that maximizes success for your numbers.

Key Takeaways

- Static allocation ("set and forget") ignores sequence of returns risk

- Traditional declining glide paths aren't always optimal

- Rising glide paths (more stocks over time in retirement) often improve success rates

- The best glide path is personal—test different options with simulation

Don't just pick a number. Test it.

Optimize Your Glide Path

QuantCalc's glide path optimizer tests allocation strategies and finds the one that maximizes your success probability.

Frequently Asked Questions

What is a glide path in retirement investing?

A glide path is a planned schedule for changing your stock-to-bond allocation over time. In the accumulation phase, you typically hold more stocks and gradually shift toward bonds as retirement approaches. Some research supports a 'rising equity' glide path in retirement — starting with 30-40% stocks at retirement and increasing to 60-70% by age 80 — to reduce sequence of returns risk while maintaining growth for a 30+ year retirement.

Should I use a target-date fund glide path or customize my own?

Target-date funds use a one-size-fits-all glide path that ignores your personal tax situation, ACA subsidies, Social Security timing, and pension income. Customizing your glide path based on these factors can improve after-tax outcomes by 10-20% over a 30-year retirement. Monte Carlo simulation with multi-period asset allocation lets you test different glide paths against thousands of market scenarios.

Frequently Asked Questions

A glide path is a planned schedule for changing your stock-to-bond allocation over time. In the accumulation phase, you typically hold more stocks and gradually shift toward bonds as retirement approaches. Some research supports a 'rising equity' glide path in retirement — starting with 30-40% stocks at retirement and increasing to 60-70% by age 80 — to reduce sequence of returns risk while maintaining growth for a 30+ year retirement.

Target-date funds use a one-size-fits-all glide path that ignores your personal tax situation, ACA subsidies, Social Security timing, and pension income. Customizing your glide path based on these factors can improve after-tax outcomes by 10-20% over a 30-year retirement. Monte Carlo simulation with multi-period asset allocation lets you test different glide paths against thousands of market scenarios.