MAGI Optimization in Retirement: Control Your Taxes and Benefits

MAGI drives the two biggest cost cliffs in retirement. In 2026, the ACA subsidy cliff sits at 400% of the federal poverty level — $62,600 for a single filer, $84,600 for a married couple — and crossing it by $1 can cost $15,000+ in annual subsidies. The first IRMAA Medicare surcharge bracket starts at $109,000 single / $218,000 married filing jointly. Roth withdrawals, tax-loss harvesting, and HSA contributions are the main levers that keep MAGI under your ceiling. Model your thresholds at quantcalc.app.

You've spent decades building your retirement nest egg. But here's the hard truth: how much you keep depends not just on how much you saved, but on how well you manage your Modified Adjusted Gross Income (MAGI).

MAGI is the invisible number that determines:

- Whether you pay $2,000 or $8,000 for Medicare premiums (IRMAA surcharges)

- Whether you get ACA health insurance subsidies worth $20,000 or zero

- Whether you pay 0% or 20% on capital gains

- How much of your Social Security is taxable (0%, 50%, or 85%)

This guide will show you exactly what MAGI is, why it matters so much in retirement, and most importantly—proven strategies to keep your MAGI low while maintaining your lifestyle.

What is MAGI and Why Does It Matter?

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →Modified Adjusted Gross Income (MAGI) is your Adjusted Gross Income (AGI) plus certain add-backs like tax-exempt interest and excluded foreign income.

For most retirees: MAGI ≈ AGI (the modifications rarely apply).

What counts toward MAGI:

- Wages and salary

- Traditional IRA and 401k withdrawals

- Taxable interest and dividends

- Capital gains

- Rental income

- Business income

- Taxable Social Security benefits

- Pension income

What does NOT count:

- Roth IRA withdrawals (huge advantage)

- Roth conversion amounts (for ACA purposes, but NOT for IRMAA—see below)

- Municipal bond interest

- HSA withdrawals for qualified medical expenses

- Return of principal from annuities

- Qualified charitable distributions (QCDs) from IRAs

Why MAGI matters: Federal and state programs use MAGI—not your actual spending or wealth—to determine eligibility and costs. You could have $5 million in the bank, spend $100k/year, and qualify for ACA subsidies if your MAGI is under $60k.

Run your own numbers in the free calculator →

The Three Major MAGI Thresholds in Retirement

1. ACA Subsidy Cliff (Under Age 65)

If you retire before Medicare eligibility, MAGI determines your health insurance costs.

2026 threshold:

- Singles: $62,600 (400% FPL)

- Married: $84,600

Cross that line by $1 and you lose subsidies worth $15,000-$30,000/year.

(Full guide to navigating the ACA cliff)

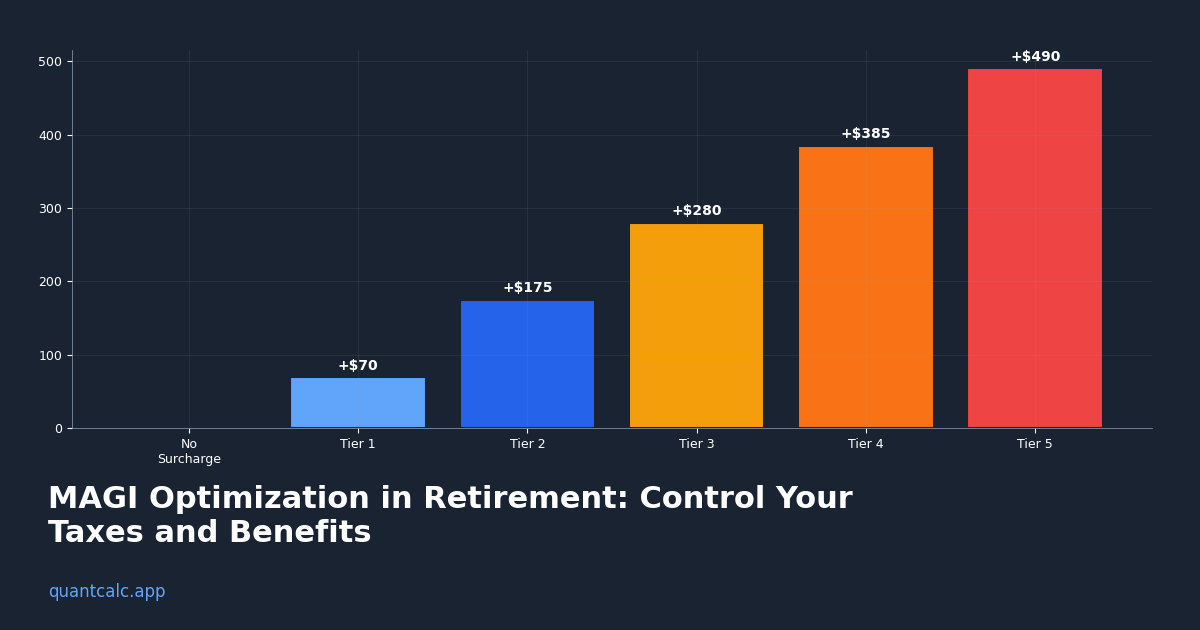

2. IRMAA Surcharges (Medicare Premiums)

Once you're on Medicare (age 65+), MAGI determines your Part B and Part D premiums through Income-Related Monthly Adjustment Amounts (IRMAA).

2026 IRMAA brackets (married filing jointly):

| MAGI | Part B Premium | Part D Surcharge | Total Annual Extra Cost |

|---|---|---|---|

| <$218,000 | $202.90/month | $0 | $0 (baseline) |

| $218,000-$274,000 | $284.10 | $14.50 | $1,148/year extra |

| $274,000-$342,000 | $405.80 | $37.50 | $2,885/year extra |

| $342,000-$410,000 | $527.50 | $60.40 | $4,620/year extra |

| $410,000-$750,000 | $649.20 | $83.30 | $6,355/year extra |

| ≥$750,000 | $689.90 | $91.00 | $6,936/year extra |

Key insight: Crossing from $217,000 to $219,000 in MAGI costs you $1,148/year in extra premiums. That's a 57% marginal penalty on $2,000 of income.

3. Capital Gains Tax Brackets

Long-term capital gains rates depend on taxable income (which is driven by MAGI).

2026 brackets (married filing jointly):

- 0% rate: Income up to $89,250

- 15% rate: $89,250 - $553,850

- 20% rate: Above $553,850

The opportunity: Retirees with low MAGI can harvest capital gains at 0% tax—free money.

MAGI Optimization Strategy #1: Live Off Roth Withdrawals

The single most powerful MAGI tool: Roth IRA withdrawals don't count toward MAGI.

Example:

- Spending needs: $70k/year

- Social Security: $30k (but $25.5k is taxable due to provisional income formulas)

- Withdraw from Roth IRA: $40k

- MAGI: $25.5k (only taxable Social Security)

Result: Despite $70k spending, MAGI is $25.5k—well under every threshold.

How to build Roth balances:

- Contribute directly while working (if income allows)

- Use backdoor Roth (for high earners)

- Do Roth conversions in low-income years (early retirement, before RMDs kick in)

(Step-by-step guide to Roth conversion ladders)

MAGI Optimization Strategy #2: Tax-Loss Harvesting

If you hold investments in taxable brokerage accounts, tax-loss harvesting is a powerful MAGI reduction tool.

How it works:

- Sell losing positions to realize capital losses

- Losses offset gains dollar-for-dollar

- Excess losses offset up to $3,000 of ordinary income per year

- Carryforward unused losses indefinitely

Example:

- You need to sell $50k of stocks for living expenses

- Half your holdings are winners (+$10k gains), half are losers (-$10k losses)

- Sell both: $50k cash, $0 net gains

- MAGI impact: $0

Advanced move: Harvest losses in December, then immediately buy similar (but not identical) assets to maintain market exposure. Example: Sell VTI (Vanguard Total Stock Market), buy ITOT (iShares Total Market). Economically identical, but avoids wash sale rules.

MAGI Optimization Strategy #3: 0% Capital Gains Harvesting

If your MAGI is under $89,250 (married) or $44,625 (single), long-term capital gains are taxed at 0%.

The strategy:

- Deliberately sell appreciated assets to "harvest" gains at 0% tax

- Immediately buy back the same securities (no wash sale rule for gains)

- This "resets" your cost basis, reducing future capital gains

Example:

- MAGI before harvesting: $60k

- Room left in 0% bracket: $29,250

- Sell $29,250 of appreciated stock (cost basis $20k, gains $9,250)

- Immediately buy back the same stock

- Pay $0 in taxes

- New cost basis: $29,250 (vs. old $20k)

- Future gains reduced by $9,250

When to do this: Every year your MAGI is in the 0% bracket. This is "free" basis step-up that reduces future MAGI from capital gains.

MAGI Optimization Strategy #4: Qualified Charitable Distributions (QCDs)

If you're 70½+ and charitably inclined, QCDs are a powerful MAGI reduction tool.

How it works:

- Donate directly from your IRA to a qualified charity (up to $111,000/year in 2026)

- The donation satisfies your Required Minimum Distribution (RMD)

- BUT: it doesn't count as income (doesn't increase MAGI)

Example without QCD:

- RMD: $40k (must withdraw)

- Charity donation: $10k (from checking account)

- MAGI: $40k

Example with QCD:

- RMD: $40k, but $10k goes directly to charity via QCD

- Withdraw only $30k to your account

- Charity donation: $10k (via QCD)

- MAGI: $30k (only the $30k you withdrew counts)

Benefit: $10k lower MAGI, which could save thousands in IRMAA surcharges or ACA subsidies.

Limitation: QCDs only work for IRAs, not 401ks (though you can roll 401k to IRA first). And you can't take the charitable deduction (but most retirees take standard deduction anyway, so this doesn't matter).

MAGI Optimization Strategy #5: Strategic Roth Conversions

Roth conversions are a trade-off:

- Short-term: Conversions increase MAGI in the conversion year (bad for IRMAA, ACA)

- Long-term: More Roth balance means lower MAGI forever (good for future years)

Optimal timing for conversions:

Before Age 65 (Pre-Medicare)

Do conversions ONLY if:

- Your MAGI is already above the ACA cliff (so conversions don't cost you subsidies)

- OR you're on employer/spouse insurance (ACA doesn't apply)

- OR you're in an unusually low-income year (sabbatical, business loss)

Warning: Do NOT do Roth conversions if it pushes you over the ACA cliff ($60k single, $81k married). The subsidy loss ($15-20k) far exceeds the tax benefit of conversion.

Age 65-72 (Medicare, Pre-RMD)

This is the golden window for Roth conversions:

- No more ACA cliff concerns

- Not yet forced to take RMDs (which spike MAGI)

- Can control MAGI precisely

Strategy: Convert up to the top of the 12% or 22% tax bracket, but watch IRMAA thresholds. If you're close to $218k (first IRMAA tier for married filing jointly), consider stopping at $217k.

Advanced move: IRMAA is based on MAGI from 2 years ago. So 2026 Medicare premiums use 2024 MAGI. You can "plan ahead" and spread conversions to avoid IRMAA tiers.

Age 73+ (RMD Years)

Conversions are harder (RMDs already pushing MAGI up), but still valuable if:

- You're in the 12% bracket and RMDs will push you to 22%+

- You want to leave Roth assets to heirs (they inherit tax-free)

MAGI Optimization Strategy #6: Control Social Security Timing

Social Security taxation is based on "provisional income" (AGI + 50% of Social Security + tax-exempt interest).

Thresholds for taxation (married filing jointly):

- Provisional income <$32k: 0% of Social Security is taxable

- $32k-$44k: 50% is taxable

- >$44k: 85% is taxable

The transition zone between these tiers creates the Social Security tax torpedo — a hidden 22.2%–40.7% effective marginal rate you can locate with the free calculator.

Strategy: If your MAGI is close to these thresholds, delaying Social Security from 62 to 70 can dramatically improve your tax situation in your 60s.

Example:

- Age 62-70: Live off Roth withdrawals ($50k/year MAGI)

- Avoid Social Security (which would add $20k+ to MAGI)

- Do Roth conversions during these low-MAGI years

- Age 70: Start Social Security at maximum benefit (76% higher than age 62)

- Higher Social Security partially offsets by now having large Roth balance to supplement

MAGI Optimization Strategy #7: Bunch Income and Deductions

Some years you'll spike MAGI no matter what (stock options vest, sell rental property, etc.). When this happens, BUNCH additional income into that year.

The logic: If you're already over the IRMAA or ACA threshold, adding more income to that year has lower marginal cost. Save your low-MAGI years for other purposes.

What to bunch:

- Extra Roth conversions (you're already paying IRMAA, might as well convert more)

- Capital gains realization (rebalance portfolio, sell appreciated assets)

- Rental property sale (1031 exchange to defer, or just sell and pay the tax)

Corresponding strategy: Bunch deductions in low-income years (when they're worth less) to save them for high-income years.

How to Track and Optimize Your MAGI

Step 1: Calculate Your Current MAGI Trajectory

Project your MAGI for the next 10 years:

- What are your planned withdrawals?

- When does Social Security start?

- When do RMDs kick in (age 73)?

- Any big one-time events (property sales, inheritances)?

Step 2: Identify Threshold Risks

- Will you cross ACA cliff (under 65)?

- Will you cross IRMAA tiers (65+)?

- Are you leaving 0% capital gains bracket unused?

Step 3: Optimize Withdrawal Sequencing

Determine which accounts to tap each year:

- Taxable brokerage (lower MAGI via gains vs. IRA ordinary income)

- Roth IRA (zero MAGI impact)

- Traditional IRA (full MAGI impact)

(Full guide to tax-efficient withdrawal strategies)

Step 4: Model It

Use Monte Carlo simulation to test different withdrawal sequences across thousands of market scenarios. See which approach keeps MAGI lowest while maintaining spending.

QuantCalc models:

- MAGI impact of different withdrawal strategies

- Roth conversion scenarios

- Tax-efficient withdrawal sequencing

- ACA and IRMAA threshold planning

Run 10,000 simulations to find the optimal strategy for YOUR portfolio and income needs.

Real-World Example: Cutting MAGI by $40,000

Scenario: Married couple, ages 64-65, $1.2M portfolio, needs $80k/year spending.

Naive approach:

- Withdraw $50k from traditional IRA

- Social Security: $30k ($25.5k taxable)

- MAGI: $75.5k

Problems:

- Just under ACA cliff ($81.7k), but no room for error

- Once on Medicare, will trigger first IRMAA tier ($75k is close to $218k threshold when combined with future RMDs)

Optimized approach:

- Withdraw $40k from Roth IRA (MAGI: $0)

- Withdraw $15k from taxable brokerage, harvest $10k in losses (MAGI: $5k in net gains)

- Social Security: $30k, but only $10k is taxable (due to lower provisional income from Roth strategy)

- Total MAGI: $15k

Result:

- $60k lower MAGI

- Qualifies for maximum ACA subsidies (saving $20k/year until Medicare)

- Avoids IRMAA entirely once on Medicare

- Preserves 0% capital gains bracket for future harvesting

5-year benefit: $100k+ in subsidies and avoided IRMAA surcharges, just from better withdrawal sequencing.

Common MAGI Optimization Mistakes

Mistake 1: Ignoring the 2-Year IRMAA Lookback

IRMAA uses MAGI from 2 years ago. So a $300k one-time income spike in 2024 will hit you with IRMAA surcharges in 2026-2027 (2 years of penalties for 1 year of income).

Mistake 2: Roth Converting Too Aggressively Before 65

Conversions can cost you $20k/year in lost ACA subsidies. Do the math: paying 12% tax to convert might save $3k, but losing the subsidy costs $20k. Bad trade.

Mistake 3: Not Using QCDs After 70½

If you're charitably inclined and not using QCDs, you're voluntarily increasing MAGI and paying unnecessary taxes.

Mistake 4: Forgetting About State Taxes

MAGI optimization often focuses on federal thresholds, but some states have their own income-based penalties (California, New York, etc.). Factor in state tax brackets when planning.

Mistake 5: Over-Optimizing for MAGI at the Expense of Total Tax Bill

Sometimes it's worth increasing MAGI to reduce lifetime taxes. Example: Taking a $1k IRMAA hit to do a $50k Roth conversion that saves $12k in future taxes.

Always optimize for total after-tax wealth, not just lowest MAGI.

The Bottom Line

MAGI is the most important number in retirement that nobody talks about. It determines your healthcare costs, your subsidy eligibility, and your tax bill—often more than your actual investment returns.

With the right strategies—Roth withdrawals, tax-loss harvesting, QCDs, strategic conversions—you can cut your MAGI by tens of thousands of dollars while maintaining your lifestyle.

The difference between optimized and un-optimized MAGI strategies can be $200k-$500k over a 30-year retirement. That's worth planning for.

Ready to optimize your MAGI and maximize your after-tax retirement income? Model your withdrawal strategy with QuantCalc and see how different approaches affect your taxes and benefits.

Further Reading: