FIRE Calculator Assumptions That Actually Matter | QuantCalc

Every FIRE calculator asks for the same inputs. Most people guess.

Here's which assumptions actually move the needle—and how to set them without fooling yourself.

The Inputs That Matter Most

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

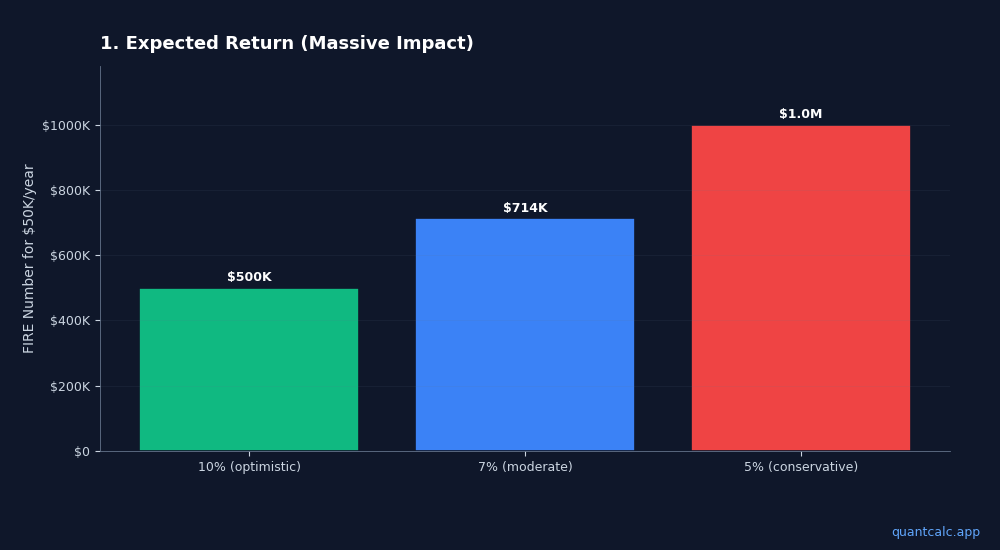

Try QuantCalc Free →1. Expected Return (Massive Impact)

This single number changes everything.

| Expected Return | FIRE Number for $50K/year |

|---|---|

| 10% (optimistic) | $500,000 |

| 7% (moderate) | $714,000 |

| 5% (conservative) | $1,000,000 |

That's a 2x difference based on one assumption.

What to use:

- Historical US stocks: ~10% nominal, ~7% real (after inflation)

- Forward-looking forecasts from major asset managers: typically 4-7% nominal for US equity over 10 years (see our overview of published forecasts)

- Conservative approach: 5-6% real returns

Don't use: The 10% number without adjusting for inflation, unless your expenses are also in future dollars.

2. Inflation Rate (Often Ignored)

Many calculators assume 2-3% inflation. Recent years showed us 6-8% is possible.

Inflation affects:

- Your future expenses

- Real returns (returns minus inflation)

- Whether your "number" actually buys what you need

What to use: 2.5-3% for long-term planning. But run a scenario at 4% to see how sensitive your plan is.

3. Withdrawal Rate (The Famous 4%)

The 4% rule is a starting point, not a law.

| Withdrawal Rate | Success Rate (Monte Carlo) |

|---|---|

| 3.0% | 97% |

| 3.5% | 93% |

| 4.0% | 85% |

| 4.5% | 75% |

Your acceptable success rate determines your withdrawal rate, which determines your FIRE number.

What to use:

- 4% if you have flexibility (can cut spending, earn some income)

- 3.5% if you want more cushion

- 3% if you want near-certainty

4. Volatility (The Hidden Variable)

Most simple calculators ignore volatility. They assume you get 7% every year.

Reality: you might get +25%, -15%, +12%, -30%, +8%... averaging 7%.

The path matters as much as the average. That's sequence of returns risk.

What to use: 15-20% standard deviation for a stock-heavy portfolio. Monte Carlo calculators handle this; simple calculators don't.

Run your own numbers in the free calculator →

The Inputs That Matter Less

Social Security: Matters, but arrives late. Plan to FIRE without it; treat it as bonus.

Tax Rate: Important for accuracy, but most people's effective rate in early retirement is low anyway (qualified dividends, capital gains harvesting).

Exact Retirement Date: Don't optimize to the month. Markets don't care about your timeline.

The Sensitivity Test

Before trusting any FIRE number, stress-test it:

| Scenario | Your FIRE Number |

|---|---|

| Base case (7% return, 4% withdrawal) | $1,250,000 |

| Lower returns (5%) | $1,500,000 |

| Higher inflation (4%) | $1,400,000 |

| Both bad | $1,750,000 |

If you can handle the worst-case scenario, your plan is robust. If you're counting on best-case, you're gambling.

What "Success Rate" Should You Target?

Monte Carlo gives you a probability. What's acceptable?

- 95%+: Very conservative. You'll likely die with too much money. Maybe that's fine.

- 85-95%: Reasonable. Some risk but manageable with flexibility.

- 75-85%: Aggressive. Requires willingness to adjust spending or earn income.

- Below 75%: Rethink the plan.

There's no right answer—it depends on your flexibility, backup plans, and risk tolerance.

Key Takeaways

- Expected return is the biggest lever—get it wrong and everything else is noise

- Use published forecasts (5-7%) not historical highs (10%)

- Volatility matters—use Monte Carlo, not simple calculators

- Stress-test with pessimistic assumptions before trusting your number

- Pick a success probability you can live with

Your FIRE number is only as good as your assumptions. Get them right.

Test Your Assumptions

QuantCalc lets you run Monte Carlo simulations with different return assumptions from BlackRock, Vanguard, JPMorgan, and GMO. See how your plan holds up.