QuantCalc vs RetirePro vs Adviser.best: 2026 FIRE Calcs

If you are planning early retirement in 2026, picking the wrong calculator is not a minor inconvenience. It is a financial risk.

The ACA subsidy cliff is back. IRMAA surcharges have a two-year lookback. Roth conversions interact with both. A calculator that ignores these interactions will give you a success probability that means nothing in the real world.

We compared three free tools that early retirees are actually using in 2026: QuantCalc, RetirePro, and Adviser.best. Here is what each one does, what it misses, and which one fits your situation.

The Quick Comparison

Run your own numbers — FREE

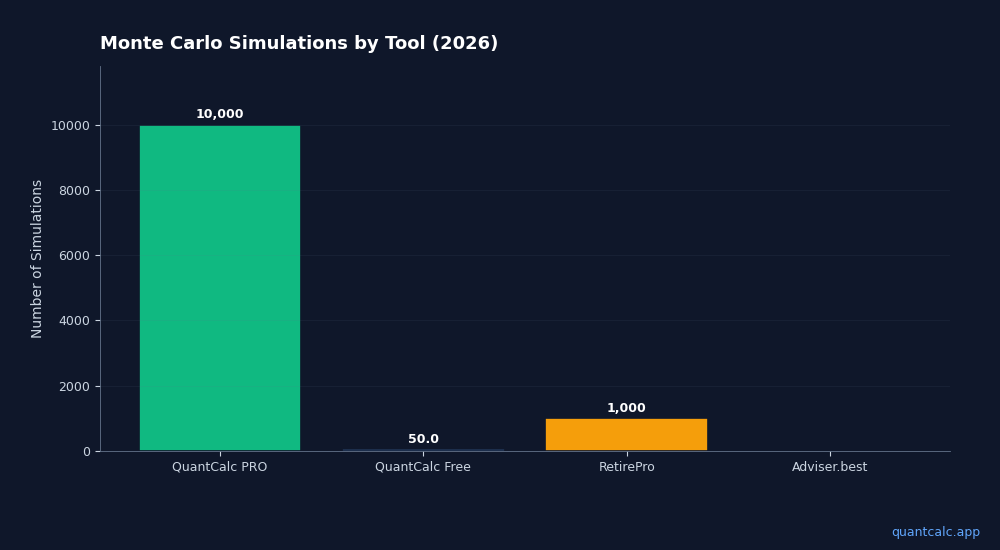

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →| Feature | QuantCalc | RetirePro | Adviser.best |

|---|---|---|---|

| Monte Carlo Simulation | 10,000 sims (PRO) / 100 (free) | 1,000 sims | None |

| ACA Cliff Calculator | Full MAGI modeling, cliff detection, subsidy amounts | Not available | ACA calculator (cliff analysis + Roth planning) |

| IRMAA Modeling | Yes (2-year lookback) | Not available | IRMAA calculator (multi-year) |

| Roth Conversion Analysis | Integrated with ACA + IRMAA | Basic Roth analysis | State-by-state optimizer |

| Portfolio Optimizer | Yes (mean-variance) | Not available | Not available |

| Glide Path Modeling | Yes (multi-period allocation shifts) | Not available | Not available |

| Forward-Looking Forecasts | 7 sources (CME, BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco) | Historical data only | Not available |

| Social Security | Yes | Yes | Not available |

| PDF Report Export | Yes (PRO) | Not available | Not available |

| Price | Free / $59 lifetime PRO | Free | Free |

Run your own numbers in the free calculator →

RetirePro (retirepro.io)

Best for: Quick sanity check with Monte Carlo simulation

RetirePro offers a clean, no-signup experience with 1,000 Monte Carlo simulations and 2026 tax bracket modeling. It handles Social Security optimization and basic Roth conversion analysis. For someone who wants a fast answer to "can I retire?", it works.

What it misses:

The ACA subsidy cliff does not exist in RetirePro's model. For an early retiree whose healthcare costs swing by $20,000+ depending on MAGI, this is not a minor omission — it is a structural gap. RetirePro also lacks IRMAA awareness, so if you are planning Roth conversions between ages 61-63, it cannot tell you how those conversions will increase your Medicare premiums two years later.

No portfolio optimizer means you cannot test whether your 60/40 allocation is actually optimal for your specific withdrawal timeline. No forward-looking forecast comparisons means you are relying on historical return assumptions that may not reflect current market conditions.

Verdict: Good for a first approximation. Not sufficient for tax-aware withdrawal planning.

Adviser.best

Best for: State-specific Roth conversion and ACA analysis

Adviser.best offers a suite of point calculators: ACA Subsidy Calculator (with cliff analysis and Roth conversion planning), IRMAA Calculator (multi-year), Roth Conversion Optimizer (state-by-state), and a Backdoor Roth Calculator. The tools are detailed and clearly built for financial advisors.

What it misses:

Each tool is standalone. There is no Monte Carlo simulation to test whether your plan survives bad market sequences. There is no portfolio optimizer. There is no glide path modeling. And critically, there is no way to see how a Roth conversion affects your ACA subsidies AND your IRMAA surcharges AND your portfolio success probability in a single view.

The state-by-state Roth optimization is a genuine differentiator — no other free tool offers this. But without Monte Carlo integration, you know the tax-optimal conversion amount without knowing whether your overall plan survives a 2008-style drawdown.

Verdict: Excellent for targeted tax questions. Not a comprehensive retirement planner.

QuantCalc (quantcalc.app)

Best for: Integrated retirement planning with tax-aware modeling

QuantCalc is the only tool in this comparison that combines Monte Carlo simulation with ACA cliff modeling, IRMAA awareness, and Roth conversion analysis in a single platform. The free tier runs 100 simulations across your full retirement timeline. PRO ($59 lifetime) unlocks 10,000 simulations, the portfolio optimizer, forward-looking forecast comparisons from multiple research firms, and PDF report export.

The integration advantage:

When you model a Roth conversion in QuantCalc, the tool simultaneously shows you:

- How the conversion affects your ACA subsidy eligibility (MAGI relative to 400% FPL)

- How the conversion affects your IRMAA surcharges two years later

- How the conversion affects your portfolio longevity across 10,000 market scenarios

- What the optimal conversion amount is given all three constraints

This matters because the "right" Roth conversion amount depends on all three factors simultaneously. Converting $50,000 might be tax-optimal in isolation but push you over the ACA cliff, costing $20,000 in subsidies. A tool that optimizes for tax alone without modeling healthcare costs gives you an answer that costs money.

What it does not have:

QuantCalc does not offer state-by-state Roth optimization (Adviser.best does). It does not have a dedicated backdoor Roth calculator. The free tier is limited to 100 simulations per run, which is enough to get a directional answer but not enough for statistically robust planning.

Verdict: The most complete integrated tool for early retirees managing ACA, IRMAA, and Roth interactions simultaneously.

Which Calculator Should You Use?

Use RetirePro if you are early in your planning process and want a quick Monte Carlo check without creating an account. Then graduate to a more comprehensive tool as your plan gets specific.

Use Adviser.best if you have a specific tax question — especially state-level Roth conversion optimization or IRMAA projection. Treat it as a specialized calculator, not a retirement planner.

Use QuantCalc if you are within 5-10 years of early retirement and need to model the interactions between Roth conversions, ACA subsidies, IRMAA, and portfolio longevity. The integration between these systems is where planning gets hard and where standalone calculators fall short.

The reality of early retirement planning in 2026 is that tax, healthcare, and investment decisions are deeply interconnected. A tool that handles one without the others is leaving money on the table — potentially tens of thousands of dollars per year in unnecessary healthcare costs or suboptimal tax positioning.

Related reading: