ACA Subsidy Repayment 2026: Why There's No Cap If You Go Over 400% FPL

Most early retirees know about the ACA subsidy cliff. Fewer understand what happens after you fall off it.

Here is the part that catches people: if your income exceeds 400% of the Federal Poverty Level in 2026, you must repay every dollar of premium tax credit you received. There is no cap on the repayment amount.

That is not a typo. Below 400% FPL, repayment caps range from $375 to $3,500 depending on income. Cross 400% FPL by even one dollar, and the cap vanishes entirely. You owe it all back. If you want to see what crossing the cliff would cost on your specific income, run it through the free ACA cliff calculator before you finalize a Roth conversion or a year-end withdrawal.

The Repayment Mechanics

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →When you enroll in a Marketplace health plan, you estimate your annual income. The government pays your insurer a premium tax credit (PTC) based on that estimate throughout the year. When you file your tax return, the IRS reconciles your actual income against the estimate.

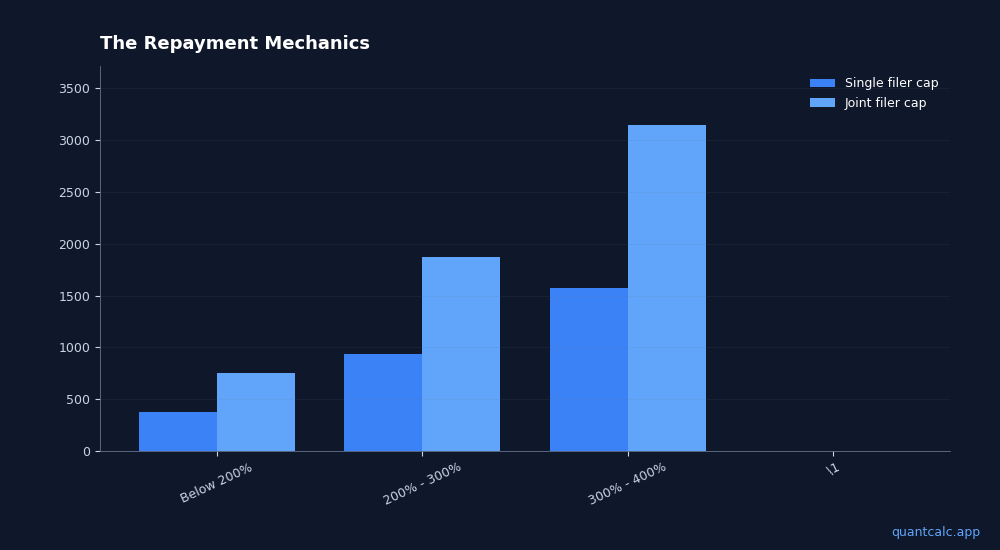

If your actual income lands below 400% FPL, any overpayment is subject to repayment caps set by the IRS:

| Income as % of FPL | Single filer cap | Joint filer cap |

|---|---|---|

| Below 200% | $375 | $750 |

| 200% - 300% | $937 | $1,875 |

| 300% - 400% | $1,575 | $3,150 |

| Above 400% | No cap | No cap |

That last row is where retirement plans get destroyed.

Run your own numbers in the free calculator →

Real Dollar Examples

For a 60-year-old couple in a mid-cost state, the 2026 benchmark Silver plan might cost $28,000-$33,000 per year before subsidies. If the household qualifies at 350% FPL, the premium tax credit could cover $20,000+ of that cost.

Scenario: $1,200 over the line

A couple estimates $82,000 income (below the $84,600 threshold for 400% FPL for a two-person household in 2026). Late in the year, an unexpected capital gains distribution from a mutual fund pushes actual income to $85,800.

- They exceeded 400% FPL by $1,200

- The repayment cap disappears

- They owe back the full $20,000+ premium tax credit

- Net cost of that $1,200 in extra income: approximately $20,000

That is an effective marginal tax rate of over 1,600%.

The Five Income Sources That Trip the Wire

The most dangerous income sources for ACA purposes are the ones you did not plan for — or forgot to count toward Modified Adjusted Gross Income (MAGI):

1. Mutual fund capital gains distributions (December surprise). Your fund manager sells winning positions in November or December. You get a distribution you never asked for. It counts as income. By the time you get the 1099, it is too late to offset it.

2. Roth conversions. Every dollar you convert from Traditional to Roth IRA adds to MAGI. A $30,000 Roth conversion that seemed tax-efficient could push you over 400% FPL and trigger full subsidy repayment.

3. Required Minimum Distributions (turning 73). If one spouse hits RMD age, those mandatory withdrawals add to household MAGI whether you need the money or not.

4. Part-time or consulting income. "I will just do a little freelancing" sounds harmless until it adds $8,000 to MAGI and costs you $20,000 in subsidies.

5. Interest and dividend income. Municipal bond interest is excluded from federal tax but included in MAGI for ACA purposes. This catches sophisticated investors who assume tax-exempt means ACA-exempt. It does not.

Why "Just Stay Under" Is Not Simple

The cliff is not just about knowing the number. It is about controlling income in a world where multiple sources are partially or fully outside your control:

- Capital gains distributions arrive in December — after you have already made every other income decision for the year

- Social Security COLAs increase your base income annually without any action on your part

- Interest rates on savings accounts and CDs generate MAGI you might not track closely

- A single Roth conversion miscalculation can erase an entire year of careful planning

The margin of safety shrinks every year as COLAs push baseline income higher.

Three Protective Strategies

1. Build a MAGI buffer of at least $5,000 below 400% FPL.

Do not plan to land at $83,000 when the threshold is $84,600. Plan for $79,000 and let the buffer absorb surprises. The cost of forgoing $5,000 in income is trivial compared to the cost of repaying $20,000 in subsidies.

2. Hold mutual funds in tax-deferred accounts.

Capital gains distributions from taxable accounts are the most common accidental MAGI spike. If your taxable brokerage holds actively managed funds, consider moving them to your IRA where distributions do not affect MAGI (until withdrawn).

3. Run the numbers before every income decision.

Before converting to Roth, before taking consulting work, before selling appreciated stock — model the impact on MAGI relative to 400% FPL. A free ACA cliff calculator can show you exactly where the threshold is and what crossing it costs.

The Timeline That Matters

CNBC reports that starting in early 2027, we will see the first wave of "astronomical tax bills" from people who received ACA subsidies in 2026 and unknowingly exceeded 400% FPL. By then it is too late — the income was earned, the subsidies were paid, and the repayment is due.

The window to plan is now. Every income decision you make between now and December 31, 2026 affects whether you keep your subsidies or repay them in full.

If you are an early retiree managing income across multiple accounts — taxable, Traditional IRA, Roth, HSA — the interactions between Roth conversions, capital gains harvesting, and ACA subsidies are too complex to track in a spreadsheet. Our ACA Cliff Calculator models these interactions and shows you the exact MAGI threshold where subsidies disappear, so you can plan with precision instead of hope.

Related reading: