Early Retirement Healthcare: The $380,000 Problem

You ran the numbers. Your portfolio hit $2 million — maybe $3 million. Your 4% withdrawal rate checks out. You built the spreadsheet. You are ready to retire at 50.

Then someone mentions healthcare, and the math falls apart.

A 50-year-old couple retiring today faces an estimated $380,000 to $500,000 in healthcare costs before Medicare kicks in at 65. That is not a scare tactic from a financial advisor trying to keep you working. It is the actuarial reality of 15 years of premiums, deductibles, copays, and the prescriptions that accumulate as you age through your fifties and early sixties.

And in 2026, it just got worse.

The ACA Subsidy Cliff Is Back

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →From 2021 through 2025, the Affordable Care Act offered enhanced subsidies with no hard income cutoff. If you earned more, your subsidy shrank gradually. Manageable.

That ended on January 1, 2026.

The original ACA subsidy cliff is back. For a two-person household, the cutoff sits at approximately $84,600 (400% of the federal poverty level). Cross that line by even one dollar, and your entire premium tax credit vanishes.

The financial impact is brutal. One California-based advisor reported a client where earning $200 more — going from $84,500 to $84,700 — cost his household $27,000 per year in lost subsidies. That is not a typo. Two hundred dollars of income triggered twenty-seven thousand dollars in additional healthcare costs.

For early retirees managing their own income through withdrawals, this is not an abstract policy problem. It is the single largest variable in your annual budget.

Run your own numbers in the free calculator →

Why FIRE Calculators Get This Wrong

Most retirement calculators treat healthcare as a flat annual expense — plug in $15,000/year, run the simulation, move on. But healthcare costs for early retirees are not flat. They are:

- Income-dependent — your ACA subsidy (or lack thereof) is determined by your MAGI

- Age-dependent — premiums increase significantly as you move from 50 to 64

- Cliff-structured — one dollar of extra income can trigger $20,000+ in additional cost

- Interaction-heavy — Roth conversions, capital gains, dividends, and even municipal bond interest all count toward ACA MAGI

A Monte Carlo simulation that does not model the ACA cliff is modeling a different retirement than the one you will actually live. Your sequence of returns risk is real, but your sequence of healthcare costs risk may be larger.

The Five Income Sources That Trip the Cliff

Early retirees typically have income from multiple sources, and every one of them counts toward MAGI:

- Capital gains distributions from index funds in taxable accounts — these happen automatically whether you sell or not

- Roth conversion income — converting traditional IRA to Roth adds dollar-for-dollar to MAGI

- Dividend income — qualified and ordinary dividends both count

- Interest income — including, critically, tax-exempt municipal bond interest for ACA purposes

- Part-time or consulting income — the "barista FIRE" strategy adds W-2 or 1099 income directly to MAGI

The municipal bond trap deserves emphasis. Municipal bond interest is tax-free for federal income tax purposes but is included in ACA MAGI calculations. Early retirees holding municipal bonds for "tax efficiency" may be unknowingly pushing themselves over the subsidy cliff.

The Math: With and Without ACA Optimization

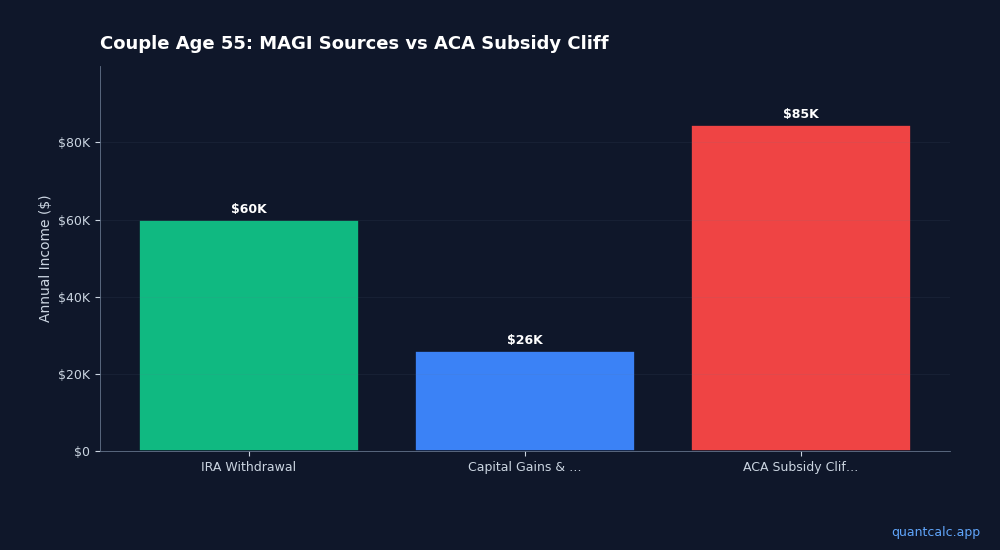

Consider a couple, both age 55, in a moderate cost-of-living area:

Without MAGI optimization:

- Traditional IRA withdrawal: $60,000

- Capital gains and dividends: $26,000

- Total MAGI: $86,000 (above 400% FPL)

- ACA premium (unsubsidized): ~$33,600/year

- Effective healthcare cost: $33,600

With MAGI optimization:

- Roth withdrawals (tax-free, not counted in MAGI): $40,000

- Traditional IRA withdrawal: $20,000

- Capital gains harvested in 0% bracket: $12,000

- Dividends: $10,000

- Total MAGI: $42,000 (well under 400% FPL)

- ACA premium (subsidized): ~$6,800/year

- Effective healthcare cost: $6,800

Annual savings: $26,800. Over 10 years to Medicare: $268,000.

That is not an optimization. That is the difference between a comfortable early retirement and one where healthcare consumes a third of your budget.

The Three Strategies That Actually Work

1. Build Your Roth Ladder Before You Retire

Roth withdrawals do not count toward ACA MAGI. If you are still working, aggressive Roth conversions now — while employer health insurance decouples your coverage from your income — build the tax-free withdrawal base you will need later.

The OBBBA made TCJA tax brackets permanent, so the conversion math is stable. Convert up to the top of your current bracket. Pay the tax while you have W-2 income to absorb it.

2. Control Your Capital Gains Timing

In taxable accounts, harvest gains strategically in years when your other income is low enough to stay under the cliff. The 0% long-term capital gains bracket applies to taxable income up to $98,900 (MFJ) in 2026.

But remember: capital gains harvesting requires careful coordination with your ACA MAGI budget. Harvest too aggressively and you blow past the cliff.

3. Use the Right Calculator

A retirement calculator that does not model the ACA cliff, IRMAA surcharges, and Roth conversion interactions is giving you a number that could be off by $200,000+ over your early retirement years. You need a tool that lets you model different withdrawal sequences and see the MAGI impact in real time.

QuantCalc's ACA Cliff Calculator models the full interaction: MAGI optimization, 400% FPL cliff detection, IRMAA avoidance, Roth conversion strategy, and capital gains harvesting — integrated with Monte Carlo simulation so you can stress-test the strategy across thousands of market scenarios.

The Bottom Line

Healthcare is not a line item. It is a dynamic, income-dependent, cliff-structured cost that interacts with every other financial decision you make in early retirement. The difference between optimizing for it and ignoring it is measured in hundreds of thousands of dollars.

If your retirement plan does not model the ACA subsidy cliff, it is not modeling your retirement. It is modeling someone else's.

Run your own ACA cliff analysis at quantcalc.app/aca — free, no signup required.