ACA Subsidy Cliff 2026: Keep Healthcare Affordable

If you're planning to retire before age 65, there's a financial landmine you need to know about: the ACA subsidy cliff. In 2026, earning just $1 too much can cost you $15,000 to $30,000 per year in health insurance premiums. No, that's not a typo.

This guide will show you exactly how the cliff works, who's affected, and most importantly—how to structure your retirement income to keep your subsidies without sacrificing your lifestyle.

What is the ACA Subsidy Cliff?

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →The Affordable Care Act (ACA) provides premium tax credits to help people afford health insurance. These subsidies are generous—often reducing premiums by 80% or more for early retirees.

But there's a hard cutoff: if your Modified Adjusted Gross Income (MAGI) exceeds 400% of the Federal Poverty Level (FPL), you lose the entire subsidy. Not a gradual reduction—complete elimination.

For 2026, the cliff is:

- Singles: $62,600 (400% FPL)

- Married couples: $84,600 (400% FPL)

- Add $20,880 per additional family member

Cross that line by even $1, and you pay full price for insurance. To stress-test your own MAGI against these thresholds, run your numbers through the free ACA cliff calculator.

Run your own numbers in the free calculator →

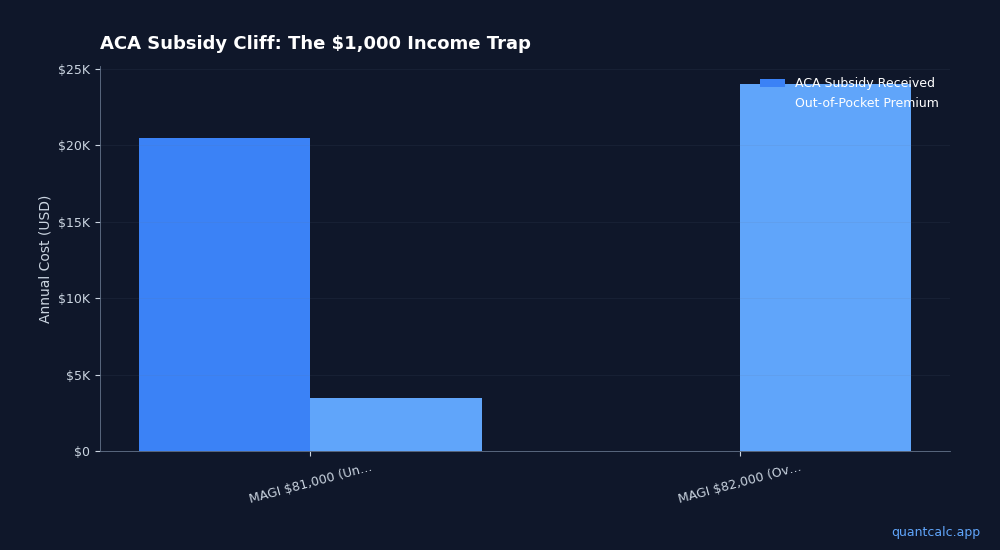

How Much Does the Cliff Cost?

Let's run the numbers for a 62-year-old couple in Denver, Colorado:

Scenario 1: MAGI of $81,000 (just under the cliff)

- Silver plan premium: $24,000/year

- ACA subsidy: $20,500

- Out-of-pocket: $3,500/year

Scenario 2: MAGI of $82,000 (just over the cliff)

- Silver plan premium: $24,000/year

- ACA subsidy: $0

- Out-of-pocket: $24,000/year

That extra $1,000 in income cost them $20,500 in subsidies. That's a 2,050% marginal tax rate.

For couples in expensive states (California, New York, Massachusetts), the cliff can exceed $30,000. For older early retirees (ages 60-64), premiums are even higher because insurers charge more before Medicare eligibility.

Why This Matters for Retirement Planning

Most retirement calculators ignore the ACA cliff entirely. They'll tell you that a 4% withdrawal rate on a $2M portfolio ($80k/year) is "safe"—but they won't mention that earning $81k instead of $80k could cost you $20,000 in health insurance.

This creates bizarre optimization problems:

The "marginal dollar" problem: Should you work part-time in early retirement? Not if that $10k salary costs you $20k in subsidies.

The "Roth conversion" problem: Should you convert $30k from traditional IRA to Roth this year? Not if it pushes you over the cliff.

The "capital gains" problem: Should you rebalance your portfolio? Not if selling winners triggers $2,000 in gains that costs you $20,000 in subsidies.

Understanding the cliff is non-negotiable if you're retiring before 65.

How to Calculate Your MAGI for ACA Purposes

MAGI for ACA subsidies is close to your Adjusted Gross Income (AGI), with a few modifications:

What counts as income:

- Wages and salary

- Traditional IRA and 401k withdrawals

- Taxable interest and dividends

- Capital gains (including from rebalancing)

- Rental income

- Business income

- Taxable Social Security (if applicable)

- Pension income

What doesn't count:

- Roth IRA withdrawals (contributions or earnings)

- Roth conversion amounts (this is a quirk—conversions add to MAGI for IRMAA but not ACA)

- Municipal bond interest

- HSA withdrawals for qualified medical expenses

- Qualified charitable distributions (QCDs) from IRAs

- Return of principal from non-qualified annuities

The non-qualified items are your toolkit for staying under the cliff.

Strategy 1: Live Off Roth Withdrawals

If you've been funding a Roth IRA for years, you have a massive advantage: Roth withdrawals don't count toward MAGI.

Example: You need $75,000/year to live. Instead of withdrawing from your traditional IRA (which counts as income), you:

- Withdraw $60,000 from Roth IRA (not counted)

- Withdraw $15,000 from traditional IRA (counted)

- MAGI: $15,000

- Result: Maximum ACA subsidies

This only works if you have sufficient Roth balances. If you don't, it's not too late—start Roth conversions now, but be strategic about timing (see below).

Strategy 2: Roth Conversion Ladder (Before Retirement)

If you're still working or in the early years of retirement with other income sources, build your Roth balance aggressively.

How it works:

- Convert traditional IRA funds to Roth IRA each year

- Pay taxes on the conversion at your current rate (12% or 22%)

- Wait 5 years (Roth seasoning rule)

- Withdraw converted principal tax- and penalty-free

Why it works:

By the time you hit the ACA cliff years (typically ages 55-64), you have a large pool of Roth money to live on without triggering MAGI.

Timing tip: Do conversions in low-income years (career gap, sabbatical, first year of retirement) when you're in the 12% bracket. Paying 12% now to avoid the cliff later is a 10:1 return.

(Full guide to Roth conversion ladders here)

Strategy 3: Taxable Account Tax-Loss Harvesting

If you have a brokerage account, you can engineer your income to stay under the cliff.

Tax-loss harvesting:

Sell losing positions to offset gains from winners. Losses offset gains dollar-for-dollar, reducing your MAGI.

Example:

- You need to sell $50k of stock to fund living expenses

- Half your holdings are winners (+$10k gains), half are losers (-$10k losses)

- Sell both: $50k cash, $0 net gains, $0 added to MAGI

0% capital gains harvesting:

If your MAGI is low enough (under $89,250 married in 2026), you can sell winners and pay 0% long-term capital gains tax. Then immediately buy back the same stocks (no wash sale rule for gains). This "resets" your cost basis and future gains without increasing MAGI.

Strategy 4: Timing Capital Events

Some income is unavoidable but controllable in timing. If you're going to have a high-income year that pushes you over the cliff, consider:

Skip the ACA that year: If you know you'll earn $120k in 2027 (stock options vesting, business sale, etc.), don't buy ACA coverage for 2027. Instead:

- Buy a short-term health plan (cheaper, less comprehensive)

- Self-insure if you're healthy

- Time the income for a year when you're still on employer insurance or already on Medicare

Bunch income into one year: If you're going to blow past the cliff anyway, might as well blow past it by a lot. Sell all appreciated assets, do Roth conversions, take bonuses—all in one year. Then stay under the cliff for the next 2-3 years.

Strategy 5: Adjust Spending Flexibility

The simplest solution: spend less in ACA years.

If the cliff is $84,600 and you're at $80,000, resist the urge to "just earn a little more." That extra $2,000 costs you $20,000. Better options:

- Cut discretionary spending by $2k-3k/year (travel less, eat out less)

- Delay major expenses (new car, home renovations) until after age 65

- Use home equity line of credit (borrowed money isn't income) to fund large expenses, pay it back after Medicare kicks in

Yes, this feels like lifestyle compromise. But $20k/year in subsidies buys a lot of future flexibility.

Advanced Tactic: The "Controllable Income" Retirement

The optimal ACA strategy is designing a retirement where 80% of your income is "invisible" to MAGI.

Example portfolio:

- $500k in Roth IRA (withdraw $30k/year, $0 MAGI impact)

- $300k in taxable brokerage (harvest gains at 0%, minimal MAGI impact)

- $1.2M in traditional IRA (leave untouched until RMDs at age 73)

- Result: $30k/year spending, $5k/year MAGI, maximum ACA subsidies

This requires planning 5-10 years before retirement, but the payoff is enormous: $150k-$200k in total subsidy value over a 10-year early retirement (age 55-65).

What If Congress Fixes the Cliff?

The subsidy cliff exists because the enhanced ACA subsidies (passed during COVID) expired. There's ongoing debate about restoring them, which would eliminate the cliff and provide subsidies on a sliding scale above 400% FPL.

Should you plan as if the cliff will be fixed?

No. Hope is not a strategy. Congressional action is unpredictable, especially in divided government. Plan assuming the cliff remains. If it gets fixed, great—you'll have more flexibility. But if it doesn't, you're protected.

The Bottom Line: Model Before You Retire

The ACA subsidy cliff is a high-stakes optimization problem. The difference between earning $81,000 and $82,000 can be $20,000/year in after-tax wealth—more than most investment strategies will ever generate.

You can't optimize this with spreadsheets alone. You need to model:

- Different withdrawal sequences (taxable vs. Roth vs. traditional)

- Income timing across multiple years

- Market scenarios (what if your portfolio drops 30% and you need to sell more shares?)

- Tax law changes (what if the cliff gets fixed in year 3 of your retirement?)

QuantCalc's Monte Carlo retirement planner lets you model ACA-optimized withdrawal strategies across thousands of market scenarios. You can see exactly how different income levels affect your subsidy eligibility and long-term success probability.

The cliff is real, the stakes are high, and the solutions are counterintuitive. But with the right planning, you can retire early, keep your subsidies, and avoid leaving $100k+ on the table.

Ready to optimize your early retirement income? Run your ACA cliff analysis with QuantCalc today.

Further Reading:

- The Complete Guide to Tax-Efficient Withdrawal Strategies in Retirement

- MAGI Optimization in Retirement: Lower Your Taxes and Keep Your Benefits

- Roth Conversion Ladder Strategy: A Step-by-Step Guide

Frequently Asked Questions

What is the ACA subsidy cliff in 2026?

The ACA subsidy cliff is the income threshold at 400% of the Federal Poverty Level ($62,160 for an individual, $83,520 for a family of 2 in 2026) above which you lose ALL premium tax credit subsidies — not just the marginal amount. Going $1 over the cliff can cost $5,000-22,000 in lost subsidies depending on age and location. The OBBBA removed the repayment caps that previously limited clawback exposure, making this cliff even more dangerous in 2026.

How do early retirees avoid the ACA subsidy cliff?

MAGI (Modified Adjusted Gross Income) management is the key strategy. Techniques include: Roth conversions sized to stay below the cliff, traditional IRA contributions to reduce MAGI, harvesting capital gains in years when you have headroom, timing asset sales across tax years, and using HSA contributions if eligible. Every dollar of MAGI reduction near the cliff can be worth $2-4 in preserved subsidies.

What happens if my income goes over the ACA cliff at tax time?

You must repay the full premium tax credit you received during the year. Since 2026, there is no repayment cap — the full amount is owed regardless of income level. For a 60-year-old couple, this can exceed $20,000 in a single year. This repayment is due with your tax return on April 15.

Frequently Asked Questions

The ACA subsidy cliff is the income threshold at 400% of the Federal Poverty Level ($62,160 for an individual, $83,520 for a family of 2 in 2026) above which you lose ALL premium tax credit subsidies — not just the marginal amount. Going $1 over the cliff can cost $5,000-22,000 in lost subsidies depending on age and location. The OBBBA removed the repayment caps that previously limited clawback exposure, making this cliff even more dangerous in 2026.

MAGI (Modified Adjusted Gross Income) management is the key strategy. Techniques include: Roth conversions sized to stay below the cliff, traditional IRA contributions to reduce MAGI, harvesting capital gains in years when you have headroom, timing asset sales across tax years, and using HSA contributions if eligible. Every dollar of MAGI reduction near the cliff can be worth $2-4 in preserved subsidies.

You must repay the full premium tax credit you received during the year. Since 2026, there is no repayment cap — the full amount is owed regardless of income level. For a 60-year-old couple, this can exceed $20,000 in a single year. This repayment is due with your tax return on April 15.