The ACA Subsidy Cliff Is Back in 2026: What Early Retirees Must Do Now

The enhanced ACA subsidies that made marketplace health insurance affordable for early retirees expired at the end of 2025. The cliff is back — and the numbers are brutal.

What Changed

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

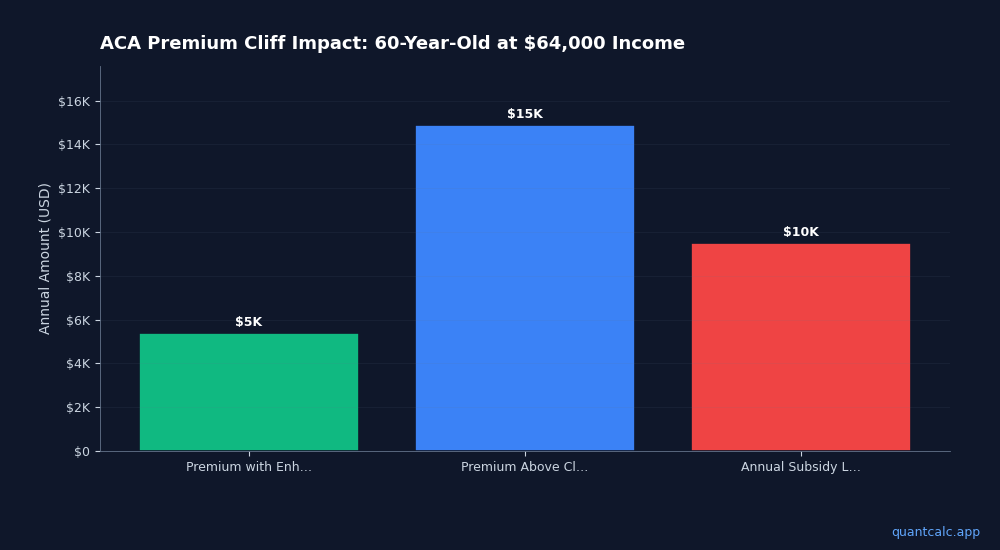

Try QuantCalc Free →From 2021 through 2025, the American Rescue Plan and Inflation Reduction Act capped marketplace premiums at 8.5% of income for everyone, regardless of how much they earned. That cap is gone.

In 2026, the old rules are back: if your Modified Adjusted Gross Income (MAGI) exceeds 400% of the Federal Poverty Level — roughly $62,160 for an individual or $84,640 for a couple — you lose ALL premium subsidies. Not a gradual reduction. A cliff.

Run your own numbers in the free calculator →

The Real Cost

Here's what that cliff looks like in dollars, according to recent analyses:

- A 60-year-old earning $64,000 (just 3% above the cliff): annual premiums jump from around $5,400 under the old enhanced subsidies to roughly $14,900. That's a $9,500/year hit.

- A 55-year-old couple with $2M saved faces up to $288,000 in total healthcare costs before Medicare kicks in at 65, according to a recent 24/7 Wall Street analysis.

- An estimated 1.5 million people have already dropped ACA marketplace coverage in 2026, with projections suggesting the number could reach 5 million.

For early retirees living off portfolio withdrawals, these numbers can wreck a retirement plan. For a detailed breakdown of what early retirement healthcare actually costs in 2026, see our comprehensive cost analysis.

Why MAGI Management Is Now Critical

The difference between $84,000 and $85,000 in household income could mean $12,000+ in lost subsidies. This makes MAGI management the single most important tax planning skill for early retirees in 2026.

Strategies that keep your MAGI below 400% FPL:

1. Prioritize Roth withdrawals during bridge years. Roth IRA distributions don't count toward MAGI. If you're between 55 and 65, pulling from Roth accounts first can keep your reported income below the cliff.

2. Harvest capital gains strategically. Long-term capital gains count toward MAGI. Selling appreciated assets in a year when your other income is low — or spreading sales across multiple years — can prevent a cliff breach.

3. Limit Roth conversions to the gap. Roth conversions are smart for long-term tax planning, but conversion income counts as MAGI. Convert only up to the point where you approach — but don't exceed — 400% FPL.

4. Watch for IRMAA too. If you're close to 65, Medicare Part B and D premiums have their own income-related surcharges (IRMAA) at different thresholds. Getting hit by both the ACA cliff and IRMAA in different years requires careful multi-year planning.

5. Model it before you withdraw. The interaction between withdrawal sequencing, Roth conversions, ACA subsidies, and IRMAA creates a four-dimensional optimization problem. Getting it wrong by even $1 over the cliff costs thousands.

For more on navigating this calculation, see our guide to ACA subsidy cliff exposure and protection strategies.

Run Your Numbers

The QuantCalc ACA Cliff Calculator models all of these interactions in one place. Input your accounts (taxable, traditional IRA, Roth), set your expected spending, and it shows you:

- Exactly where your MAGI lands relative to the 400% FPL cliff

- How much you save (or lose) by adjusting withdrawal sources

- The optimal Roth conversion amount that maximizes savings without breaching the cliff

- IRMAA bracket impacts for those approaching Medicare age

It's free to use. No account required. Learn more about the calculator's features and methodology.

The Bottom Line

The ACA subsidy cliff isn't a hypothetical risk anymore — it's current law affecting millions of people right now. If you're retired or planning to retire before 65, your healthcare costs just became the single biggest variable in your financial plan.

The retirees who come out ahead will be the ones who manage their MAGI proactively, not the ones who find out they owe $12,000 in premium repayments when they file their taxes.

Start modeling your numbers now. April 15 is 25 days away, and your 2025 tax decisions inform your 2026 strategy.

Frequently Asked Questions

What is the ACA subsidy cliff?

The ACA subsidy cliff is the income threshold (400% FPL) where premium tax credits drop to zero. In 2026, that's $62,600 for individuals and $84,600 for couples.

What happens if I earn $1 over the ACA cliff?

If your MAGI exceeds 400% FPL by even $1, you lose ALL premium tax credits and pay full marketplace insurance premiums.

Can early retirees avoid the ACA cliff?

Yes, through strategic income management: traditional IRA contributions, Roth conversion timing, capital gains harvesting, and MAGI planning.

Sources: CNBC, 24/7 Wall Street, MoneyGeek, Kiplinger

Frequently Asked Questions

The ACA subsidy cliff is the income threshold (400% FPL) where premium tax credits drop to zero. In 2026, that's $62,600 for individuals and $84,600 for couples.

If your MAGI exceeds 400% FPL by even $1, you lose ALL premium tax credits and pay full marketplace insurance premiums.

Yes, through strategic income management: traditional IRA contributions, Roth conversion timing, capital gains harvesting, and MAGI planning. Sources: CNBC, 24/7 Wall Street, MoneyGeek, Kiplinger