The ACA Subsidy Cliff Is a $15K Tax Bomb for Early Retirees

The Affordable Care Act enhanced subsidies expired December 31, 2025. If you're early-retired and buying marketplace insurance, the math just changed dramatically.

The Cliff Is Back

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

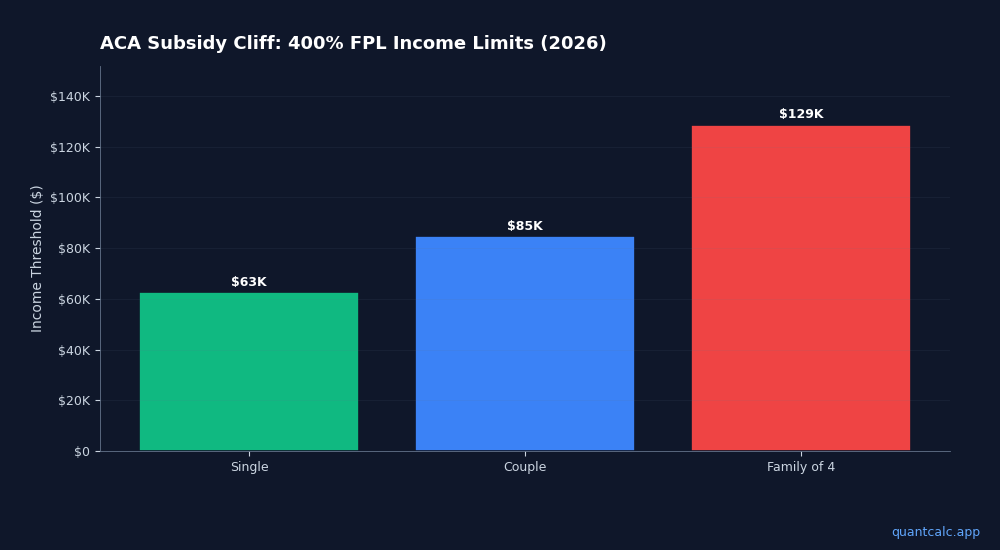

Try QuantCalc Free →Before 2021, ACA premium tax credits had a hard income cutoff at 400% of the Federal Poverty Level. The American Rescue Plan and subsequent extensions removed this cliff — subsidies phased out gradually regardless of income. That's over now.

2026 thresholds (400% FPL):

- Single: $62,600

- Couple: $84,600

- Family of 4: $128,600

Exceed these by $1 and you get zero premium tax credits. The average recipient saw premiums more than double overnight. About 22 million people were receiving enhanced subsidies. If you want a concrete picture of how close you are to the threshold, run your household through the free ACA cliff calculator — it shows the exact dollar amount you can earn before triggering the subsidy clawback.

Run your own numbers in the free calculator →

Why This Is a Software Problem

For early retirees managing their own income (no employer paycheck), every financial decision affects MAGI:

- A Roth conversion adds to MAGI

- Selling appreciated stock adds to MAGI

- Even Social Security benefits count toward MAGI

- Your MAGI this year determines your Medicare IRMAA surcharges two years from now

This creates a multi-variable optimization problem that spreadsheets handle poorly because the interactions cascade across years:

- Convert $5K too much to Roth → blow ACA subsidy → $15K+ cost

- Harvest capital gains in December → push MAGI over IRMAA bracket → higher Medicare premiums in 2028

- Delay Social Security to reduce MAGI → preserve ACA subsidies but miss out on years of SS income

No single calculator handles all three simultaneously.

What I Built

I got frustrated tracking this across 15 spreadsheet tabs, so I built two things:

1. ACA Cliff Calculator (free, browser-based): quantcalc.app/aca

Enter your income sources and it shows exactly where you stand relative to the 400% FPL cliff. Calculates your subsidy amount, shows IRMAA brackets, and models Roth conversion scenarios — all client-side, no data leaves your browser.

2. Monte Carlo Retirement Planner (free tier available): quantcalc.app

Runs up to 10,000 Monte Carlo simulations using forward-looking forecast data from CME, BlackRock, JPMorgan, Vanguard, GMO, Schwab, and Invesco. Models multi-period asset allocation, glide paths, Social Security timing, and pension income. The PRO version ($59 lifetime) includes a portfolio optimizer and PDF export.

Neither tool needs an account, and your inputs are never stored or sold — the ACA calculator runs in your browser; the Monte Carlo planner sends inputs over HTTPS to run the simulation and doesn't retain them.

The Tax Season Angle

April 15 is 26 days away. Three deadlines are converging:

- IRA contribution deadline — you can still make 2025 contributions

- First RMD deadline (April 1) — if you turned 73 in 2025

- Q1 estimated tax payment — if you're no longer having taxes withheld

Each of these affects your 2026 MAGI, which determines your ACA subsidies and future IRMAA premiums. Planning now — not in December — gives you 9 months to adjust.

Not financial advice. I'm a developer who got tired of not having good tools for this problem.