2026 Tax Brackets Did NOT Revert — FIRE Planning Update

If you've been researching 2026 tax planning for your early retirement, you've probably seen some alarming headlines. "Tax rates going up in 2026!" "The 12% bracket jumps to 15%!" "Your Roth conversion window is closing!"

None of that happened. And if you're building your FIRE withdrawal strategy around those claims, your numbers are wrong.

What Actually Happened

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

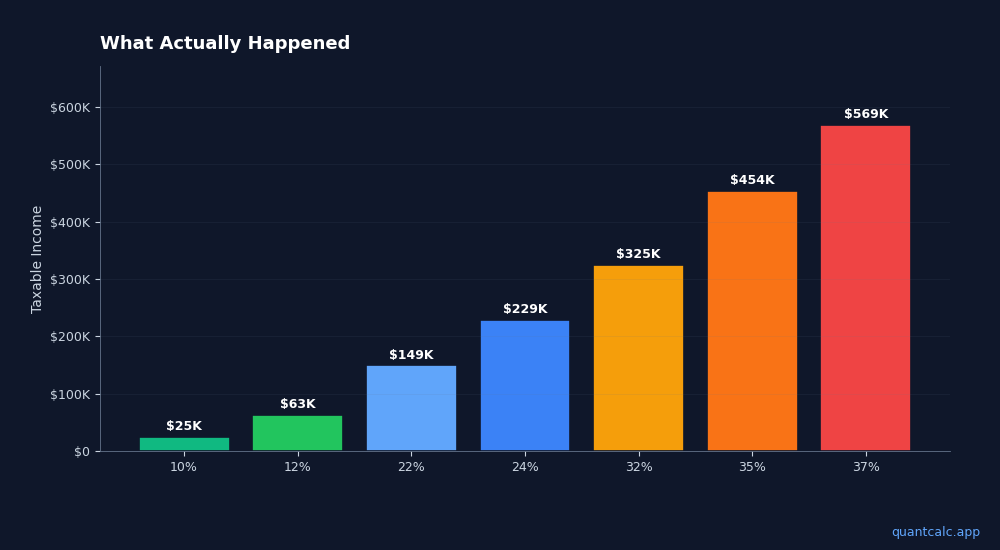

Try QuantCalc Free →The Tax Cuts and Jobs Act (TCJA) of 2017 was originally set to expire at the end of 2025. That was real. The lower brackets — 10%, 12%, 22%, 24%, 32%, 35%, 37% — were scheduled to revert to pre-2017 levels.

Then the One Big Beautiful Bill Act (OBBBA) was signed on July 4, 2025. It made the TCJA tax brackets permanent. The brackets did not revert. The 12% bracket is still 12%. The 22% bracket is still 22%.

Here are the actual 2026 federal income tax brackets for married filing jointly:

| Rate | Taxable Income |

|---|---|

| 10% | Up to $24,800 |

| 12% | $24,801 – $100,800 |

| 22% | $100,801 – $211,400 |

| 24% | $211,401 – $403,550 |

| 32% | $403,551 – $512,450 |

| 35% | $512,451 – $768,700 |

| 37% | Over $768,700 |

These are inflation-adjusted from 2025. No reversion. No rate increase.

Run your own numbers in the free calculator →

Why So Many Sites Got This Wrong

Most of the articles claiming brackets reverted were written in late 2024 or early 2025, before the OBBBA passed. That was reasonable forecasting at the time — the TCJA was expiring.

The problem is that many of these articles were never updated. Major financial sites, tax preparation companies, and even some financial planning blogs still have 2024-era predictions live on their sites in March 2026. If you're reading a "2026 tax planning" article that mentions the 15% or 25% bracket, check the publication date. It's stale.

What OBBBA Actually Changed That Matters for FIRE

While the brackets stayed the same, OBBBA did make changes worth tracking:

1. SALT Cap Raised to $40,400

The state and local tax deduction cap jumped from $10,000 to $40,400 (with a phaseout above $500,000 MAGI). If you're in a high-tax state doing Roth conversions, this changes your optimal conversion amount. You can now deduct more state income tax, which lowers the effective federal cost of a conversion.

2. Standard Deduction: $32,200 MFJ

Slightly higher than 2025. For an early retiree couple with no mortgage interest, this remains the default choice over itemizing in most cases — unless your SALT + charitable giving exceeds $32,200.

3. New $1,000 Charitable Deduction

Even if you take the standard deduction, OBBBA allows a $1,000 above-the-line deduction for charitable contributions. Small, but it reduces MAGI — which matters for ACA subsidy calculations.

4. Estate Exemption: $15M / $30M

Doubled and made permanent. Most early retirees won't hit this, but if your FIRE number is in the $5M+ range, estate planning just got simpler.

How This Affects Your Roth Conversion Strategy

The old argument for accelerating Roth conversions was: "Convert now at 22% before the bracket reverts to 25% in 2026." That urgency is gone. Brackets are the same in 2026 as they were in 2025.

But Roth conversions still make sense for early retirees — just for different reasons:

- ACA cliff management. The enhanced premium tax credits expired. In 2026, earning $1 over 400% FPL ($84,600 for a couple) means losing all ACA subsidies — potentially a $15,000-$25,000 hit depending on your age and state. Roth withdrawals don't count toward MAGI. Every dollar you convert now (before Medicare at 65) is a dollar you can withdraw tax-free during your ACA years without triggering the cliff.

- IRMAA lookback. Medicare uses your income from 2 years prior to set premiums. Large Roth conversions in your early 60s can trigger IRMAA surcharges of $1,000-$4,000/year per person. Plan conversions before the lookback window matters.

- RMD reduction. Required minimum distributions start at 75. Every dollar converted reduces your future RMD — which reduces future taxable income, which reduces future Medicare premiums and ACA exposure if you retire before 75.

The case for Roth conversions in 2026 is about MAGI management, not bracket arbitrage.

The Real 2026 Planning Challenge

The brackets didn't change. What changed is the ACA subsidy structure. That's the variable that makes 2026 fundamentally different for early retirees.

A couple retiring at 55 with $2M in traditional IRAs needs to thread a needle: convert enough to Roth each year to reduce future RMDs, but not so much that MAGI exceeds 400% FPL and triggers a $20,000+ healthcare cost increase.

That optimization problem — balancing Roth conversions, capital gains harvesting, ACA cliff avoidance, and IRMAA prevention across a 10-15 year pre-Medicare window — is exactly what QuantCalc's ACA Cliff Calculator was built for.

No spreadsheet captures all the interactions. The ACA cliff, IRMAA lookback, capital gains tax bump, Social Security taxation thresholds, and RMD projections all interact. Getting one wrong cascades through the others.

What To Do Now

- Stop reading 2024 tax planning articles. If it mentions the 25% bracket for 2026, it's wrong.

- Know your ACA ceiling. For 2026: $62,600 (single), $84,600 (couple) at 400% FPL. Stay under this or accept losing all subsidies.

- Model your Roth conversion amount. The optimal conversion fills your current bracket and keeps MAGI below the ACA cliff. Run the numbers here.

- Plan your capital gains harvesting. The 0% long-term capital gains bracket applies up to $98,900 taxable income (MFJ). But capital gains count toward ACA MAGI — harvest carefully.

- Check your HSA eligibility. Starting in 2026, all ACA Bronze plans qualify for HSAs. Contribute $8,750 (family) to reduce MAGI.

The 2026 tax landscape is more complex than "brackets went up" — it's actually "brackets stayed the same but healthcare subsidies got harder." Plan accordingly.