Best Retirement Calculators 2026: Free Planning Tools Compared

The best retirement calculators in 2026 share three must-have features: Monte Carlo simulation (thousands of randomized return sequences, not one average), inflation adjustment, and tax awareness. Tools that assume a flat 7% return every year can swing your projected lifetime outcome by $500,000 or more. This guide walks through each category of free planning tool, the hidden assumptions that matter, and how to choose the right one. Run a free 10,000-scenario simulation at quantcalc.app.

You Google "retirement calculator," and you get 50 million results. Most are garbage — oversimplified tools that assume 7% returns every year and tell you "you're on track!" without accounting for market crashes, inflation variability, or tax considerations.

The difference between a good retirement calculator and a bad one can be $500,000+ in lifetime outcomes. Use the wrong tool, and you might retire too early (running out of money at 80) or too late (dying with $3M you never spent).

This guide explains what makes a great retirement calculator, what categories of tools are available in 2026, and how to choose the right one for your needs.

What Makes a Great Retirement Calculator?

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →Before diving into specific tools, here's what separates excellent calculators from junk:

Must-Have Features

1. Monte Carlo simulation

Simple average-return calculators are useless. You need Monte Carlo (thousands of simulations with randomized return sequences) to see your actual probability of success.

(Learn more about Monte Carlo simulation)

2. Inflation adjustment

Your $50k/year spending today will be $90k+ in 30 years. Tools that ignore inflation are dangerously optimistic.

3. Tax awareness

Withdrawals from traditional IRAs, Roth IRAs, and taxable accounts are taxed differently. Tools that ignore this overestimate your spending power by 15-30%.

4. Asset allocation options

100% stocks, 100% bonds, and 60/40 are completely different risk profiles. Good calculators let you model multiple allocations.

5. Social Security integration

For most retirees, Social Security is 30-50% of income. Calculators that don't account for it are incomplete.

Nice-to-Have Features

- RMD (Required Minimum Distribution) modeling

- Dynamic withdrawal strategies (guardrails, percentage-based)

- Portfolio optimization

- Multiple scenarios (what-if testing)

- Forward-looking forecast data (not just historical averages)

- ACA subsidy cliff modeling

- IRMAA surcharge awareness

- Stochastic inflation modeling

Run your own numbers in the free calculator →

Categories of Retirement Calculators

Free Monte Carlo Simulators

These are purpose-built for probabilistic retirement planning. They focus on simulation depth and may include features like forward-looking forecasts, tax-aware withdrawals, and portfolio optimization. The best ones in this category run thousands of simulations with correlated asset returns and let you compare across multiple forecast assumptions.

Best for: DIY planners who want professional-grade analysis without advisor fees.

Historical Backtesting Tools

These test your plan against every historical period since the 1870s. They show how your plan would have survived every past market environment — useful for understanding sequence-of-returns risk.

Strengths: Free, real data, good for stress-testing against actual historical crashes.

Limitations: Backward-looking only. No Monte Carlo simulation. No tax modeling. Can't model forward-looking scenarios. Interface is often dated.

Best for: FIRE community members who want historical validation as a second opinion.

Dynamic Withdrawal Strategy Tools

Some free tools specialize in testing dynamic spending rules — guardrails, percentage-based, floor-and-ceiling strategies. If you plan to adjust spending based on portfolio performance (rather than withdrawing a fixed amount), these are worth exploring.

Best for: Sophisticated planners who want to test withdrawal strategies beyond the 4% rule.

Brokerage-Provided Calculators

Major brokerages (Fidelity, Vanguard, Schwab, T. Rowe Price) offer free retirement planners that pull your actual account balances.

Strengths: From trusted brands. Simple, clean interfaces. Good for quick estimates.

Limitations: Limited customization. Require brokerage accounts. No advanced features like tax-aware withdrawal modeling or forward-looking forecasts. Return assumptions are proprietary and cannot be overridden.

Best for: Quick sanity checks.

Professional Advisor-Tier Platforms

Tools like eMoney Advisor ($3,600-$6,000/year), MoneyGuidePro ($1,500-$3,000/year), and RightCapital ($1,200-$2,400/year) are the industry standard for financial advisors.

Strengths: Extremely comprehensive. Beautiful client presentations. Tax planning, estate planning, insurance analysis. Monte Carlo simulation.

Limitations: Only available through financial advisors. Expensive. Overkill for simple planning.

Best for: High-net-worth individuals working with financial advisors.

QuantCalc: Where It Fits

URL: quantcalc.app

QuantCalc is a free Monte Carlo simulator designed for the gap between simple calculators and advisor-tier software. Here is what it does:

- Monte Carlo simulation (50 to 10,000 runs depending on tier)

- Multi-period asset allocation with glide path modeling

- Portfolio optimizer (mean-variance, efficient frontier)

- Forward-looking forecasts derived from publicly available research by BlackRock, JPMorgan, Vanguard, GMO, Schwab, and Invesco

- ACA subsidy cliff modeling with MAGI optimization

- IRMAA surcharge awareness with 2-year look-back

- Roth conversion strategy with bracket-fill optimization

- Capital gains harvesting integrated with ACA/IRMAA constraints

- Stochastic inflation (4 models)

- 8 named stress test scenarios plus custom shock modeling

- Life event modeling (property, income changes, healthcare shifts)

- PDF report export with white-label option for advisors

- 51-state tax modeling

- Tax-aware withdrawal sequencing

- No account required, no tracking, no data sold

Free tier:

- 100 Monte Carlo simulations

- Basic features (enough for most people)

- No credit card required

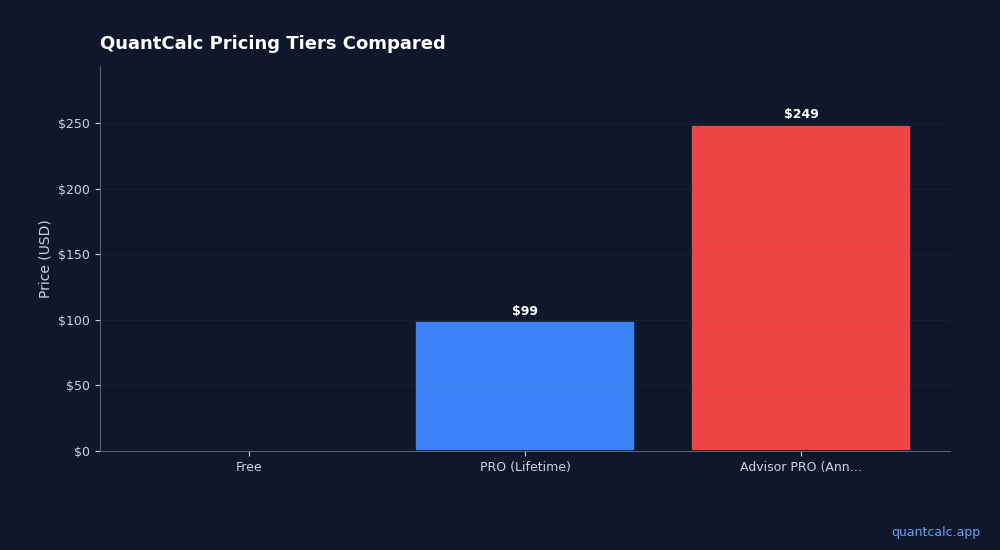

PRO tier ($59 lifetime):

- Up to 10,000 simulations

- Portfolio optimizer

- Forward-looking forecast comparisons

- PDF export

Advisor PRO ($249/year):

- Everything in Personal PRO

- Client-facing reports

- White-label branding

Strengths:

- Most comprehensive free Monte Carlo tool available

- Forward-looking forecast comparisons (6 published sources)

- ACA cliff and IRMAA modeling — rare among free tools

- Clean, modern interface

- No ads, no account required for basic use

Weaknesses:

- Newer tool (less brand recognition than established names)

- Advanced features require PRO upgrade

- Does not pull account balances automatically

- No estate planning or insurance analysis

Best for: Anyone who wants professional-grade retirement planning without paying $1,000+ for financial advisor software. Especially valuable for early retirees managing ACA subsidies and tax-aware withdrawals.

How to Choose the Right Calculator for You

If you want free, comprehensive, and DIY:

Use a Monte Carlo simulator with tax awareness and forward-looking forecasts. QuantCalc has the best balance of features and usability in this category.

If you're a FIRE early retiree who loves data:

Use a historical backtesting tool for validation alongside a Monte Carlo tool for forward-looking analysis.

If you want to test dynamic withdrawal strategies:

Look for tools that support guardrail, percentage-based, and floor-and-ceiling spending rules.

If you work with a financial advisor:

Ask which software they use (eMoney, MoneyGuidePro, RightCapital are all excellent).

If you just want a quick check:

Your brokerage's built-in calculator will give you a ballpark.

Common Calculator Mistakes to Avoid

Mistake 1: Using Only One Calculator

Different calculators use different assumptions. Run your plan through 2-3 tools to see if results align.

Mistake 2: Trusting "You're on Track!" Without Seeing Assumptions

Many calculators assume 7-8% returns. In today's market (high valuations, lower forward projections), 5-6% might be more realistic.

Mistake 3: Ignoring Taxes

A calculator that says you need $1M might actually mean you need $1.3M after taxes.

Mistake 4: Not Stress-Testing

Don't just look at "average" outcomes. Check:

- What's your success rate? (should be 85%+ for comfort)

- What's the worst-case scenario (10th percentile)?

- How sensitive are you to early market crashes?

Mistake 5: Set It and Forget It

Rerun your calculations annually. Markets change, your spending changes, tax laws change. Update your plan accordingly.

The Bottom Line

The retirement calculator you choose matters. A lot.

Overly simple calculators give you false confidence. They'll tell you "you're fine" based on 7% returns and no taxes, then you run out of money at 82.

Overly complex (professional) tools are powerful but inaccessible unless you're working with (and paying) a financial advisor.

The sweet spot in 2026: A free Monte Carlo simulator with tax-aware modeling, forward-looking forecasts, and ACA cliff awareness. QuantCalc hits this sweet spot — free for basics, $59 lifetime for professional features.

Ready to run a professional-grade retirement analysis? Try QuantCalc for free — no credit card, no signup required. Upgrade to PRO for 10,000 Monte Carlo simulations and forward-looking forecasts.

Further Reading: