ACA Premium Tax Credit Repayment Caps 2026

If you received Advance Premium Tax Credits (APTC) in 2025 and your actual income came in higher than what you estimated on your Marketplace application, you may owe some or all of that subsidy back when you file your 2025 tax return by April 15, 2026.

The amount you owe depends on one critical factor: whether your income stayed below or exceeded 400% of the Federal Poverty Level (FPL).

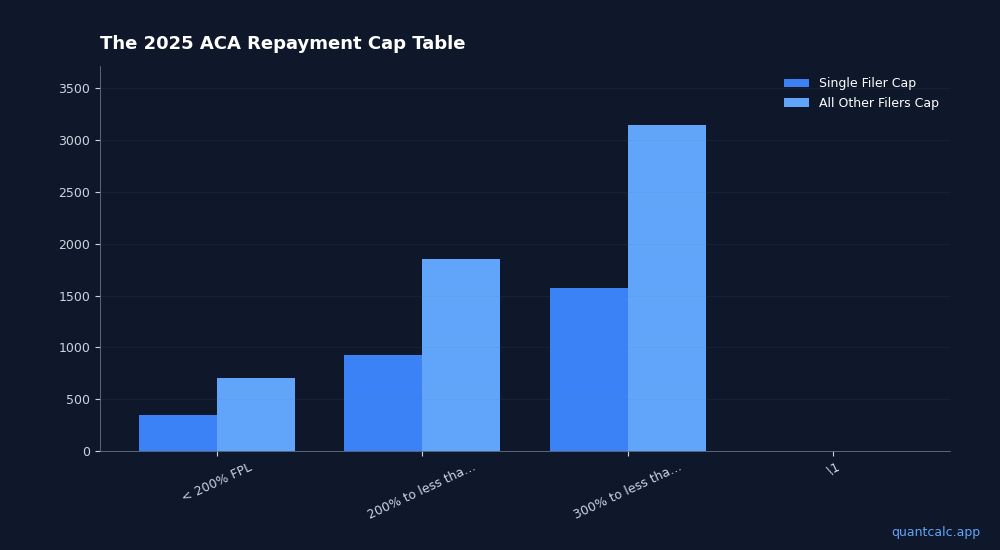

The 2025 ACA Repayment Cap Table

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →For tax returns filed in 2026 (tax year 2025), the IRS caps how much you must repay based on your household income relative to the FPL:

| Household Income (% of FPL) | Single Filer Cap | All Other Filers Cap |

|---|---|---|

| Under 200% FPL | $350 | $700 |

| 200% to less than 300% FPL | $925 | $1,850 |

| 300% to less than 400% FPL | $1,575 | $3,150 |

| 400% FPL and above | No cap | No cap |

Source: IRS Form 8962 instructions, Table 5.

The critical line is 400% FPL. Below it, your repayment is limited. Above it, you repay every dollar of excess APTC with no limit.

Run your own numbers in the free calculator →

What 400% FPL Looks Like in 2025 Dollars

For tax year 2025, the 400% FPL thresholds are approximately:

- Single: $62,600

- Couple (2-person household): $84,600

- Family of 4: $128,600

If your Modified Adjusted Gross Income (MAGI) even slightly exceeds these thresholds, you lose the repayment cap entirely. This is the ACA cliff that catches early retirees off guard.

Why Early Retirees Are Most at Risk

If you retired early and are managing income from multiple sources — taxable brokerage withdrawals, Roth conversions, capital gains, freelance consulting — your MAGI can creep above 400% FPL without obvious warning signs.

Common scenarios that trigger full repayment:

- An unexpected capital gain from rebalancing a taxable account pushes MAGI over the cliff.

- A Roth conversion that was slightly too large tips income above 400% FPL.

- Freelance or consulting income that exceeded the estimate on your Marketplace application.

- Required Minimum Distributions starting at age 73 that add taxable income you didn't account for when estimating.

In each case, the consequence is the same: you repay the full difference between the APTC you received and the Premium Tax Credit you actually qualify for. For a couple receiving $15,000-$20,000 in annual subsidies, full repayment can be devastating. Model your exact exposure with the free ACA cliff calculator before year-end to see how close you are to the threshold.

5 Strategies to Minimize ACA Repayment

1. Report Income Changes to the Marketplace Immediately

If your income increased mid-year, update your Marketplace application. The exchange will adjust your APTC going forward, reducing the gap between what you received and what you qualify for at filing time.

2. Use Roth Accounts for Spending (Not Traditional)

Roth IRA and Roth 401(k) withdrawals are not included in MAGI. If you need cash, pull from Roth accounts first during years when you're receiving ACA subsidies. Every dollar from a Roth account is a dollar that doesn't push you toward the cliff. See our guide on tax-efficient withdrawal strategies for the full sequencing framework.

3. Harvest Capital Losses Before Year-End

If you have unrealized losses in taxable accounts, harvest them before December 31 to offset gains that would increase MAGI. Up to $3,000 in net capital losses can offset ordinary income as well. Watch wash sale rules carefully — repurchasing substantially identical securities within 30 days disallows the loss.

4. Time Roth Conversions Carefully

Roth conversions add to MAGI dollar-for-dollar. If you're converting, calculate the maximum conversion amount that keeps your income below 400% FPL. Our ACA Cliff Calculator models this interaction directly — enter your conversion amount and see exactly where you land relative to the cliff.

5. Consider HSA Contributions to Reduce MAGI

If you're enrolled in a Bronze or high-deductible health plan, HSA contributions reduce MAGI. Under the OBBBA Bronze-HSA change, all ACA Bronze plans are now HSA-eligible starting January 1, 2026. For tax year 2025, the HSA contribution limit is $4,300 (self-only) or $8,550 (family). That's a direct MAGI reduction that could keep you below the cliff.

What If You Already Owe Repayment?

If you're filing your 2025 return and the numbers show you owe repayment:

- File Form 8962 with your return. This reconciles the APTC you received against the PTC you qualify for.

- Check the cap table above. If your income stayed below 400% FPL, your repayment is capped at the amounts shown.

- If you owe more than you can pay, file anyway. The IRS offers installment agreements for balances you can't pay in full. Filing late adds both failure-to-file AND failure-to-pay penalties. Filing on time with a payment plan triggers only the failure-to-pay penalty (0.5%/month vs. 5%/month).

Plan Ahead for 2026

The repayment caps remain in place for 2026, but the stakes are higher for FIRE planners because OBBBA made the enhanced ACA subsidies permanent. That means ACA subsidies will be a core part of early retirement healthcare planning indefinitely — and MAGI management around the 400% FPL cliff is a skill every early retiree needs.

Use the QuantCalc ACA Cliff Calculator to model your 2026 income, Roth conversions, and capital gains against the subsidy cliff. The tool shows exactly how much subsidy you lose at each income level and helps you find the optimal conversion amount.

For a broader view of how ACA subsidies interact with your full retirement plan — including Monte Carlo simulation, portfolio optimization, and forward-looking forecast comparisons — QuantCalc PRO integrates all of these into a single planning framework.

10 days until the April 15, 2026 filing deadline. If you haven't filed yet and received ACA subsidies, run the numbers now. A few hundred dollars in strategic Roth timing can save thousands in repayment.

Previously covered topics (do not repeat): USPS postmark change, last-minute tax moves April 15, SALT deduction $40K cap OBBBA, SS tax torpedo, Monte Carlo stress test 500 scenarios, portfolio stress test 2008 crash, freelancer vs W-2 tax difference, side hustle tax guide, best free retirement calculators comparison, ACA cliff early retirement, Roth conversion FIRE, IRMAA brackets, estimated tax payments early retirement, freelancer estimated tax mistakes, tax-efficient withdrawal strategies, HSA bronze plan OBBBA, wash sale rule, testing retirement plan assumptions, portfolio optimization retirement, monte carlo simulation retirement.