ACA March 31 Deadline 2026: Don't Miss Your Payment

If you auto-renewed your ACA Marketplace plan for 2026 and haven't paid your first premium yet, you have until March 31, 2026 before your coverage is retroactively terminated.

That's four days from now.

This deadline is hitting early retirees especially hard. Here's why — and what you can do about it.

Why 2026 Premiums Shocked So Many People

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

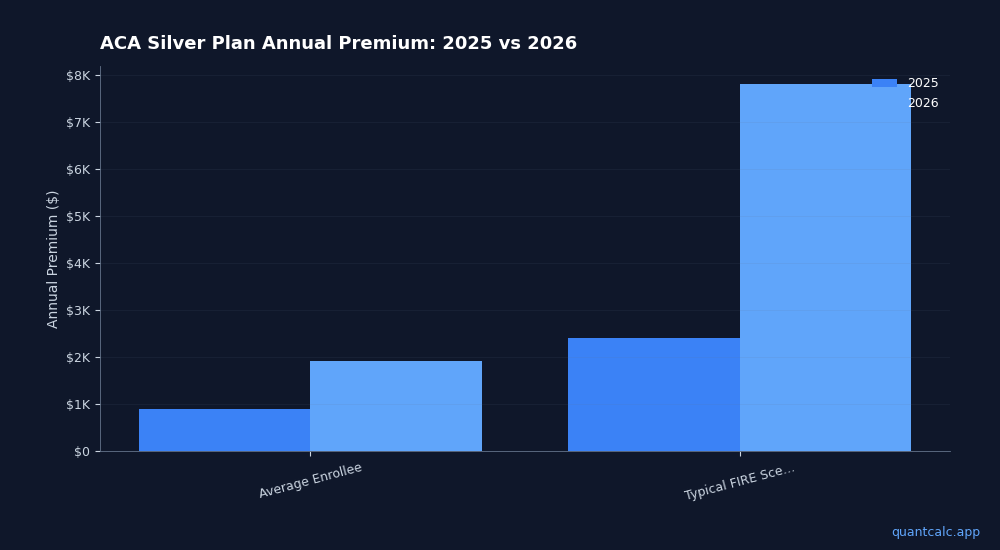

Try QuantCalc Free →The enhanced Premium Tax Credits that kept ACA premiums artificially low from 2021 through 2025 expired on December 31, 2025. Congress did not renew them.

The impact was immediate. According to KFF's analysis, ACA Marketplace enrollment dropped by approximately 1.2 million people after four consecutive years of record growth. The average enrollee receiving Premium Tax Credits saw their out-of-pocket cost for the second-lowest-cost Silver plan more than double — from $888 per year in 2025 to $1,904 in 2026.

For early retirees living on investment income, the math is worse. The 2026 ACA subsidy cliff returned in full force: earn one dollar over 400% of the Federal Poverty Level, and you owe back every dollar of subsidy you received. No cap. No phase-out. A binary cliff. Before the deadline forces your hand, use the free ACA cliff calculator to confirm whether your projected MAGI keeps you on the subsidized side of the line.

Run your own numbers in the free calculator →

The March 31 Deadline: What Actually Happens

If you were auto-renewed into a 2026 Marketplace plan but haven't made your first premium payment:

- Before March 31: You can still pay and activate your coverage retroactively to January 1.

- After March 31: Your plan is terminated. Coverage is cancelled as if it never started. You are uninsured for 2026 unless you qualify for a Special Enrollment Period.

This isn't a grace period for late payments on active coverage. This is the final window for people who were auto-renewed but never confirmed by paying.

Why Early Retirees Are Caught Off Guard

Three scenarios are playing out right now in the FIRE community:

Scenario 1: Sticker shock. You had a $200/month Silver plan in 2025 thanks to enhanced subsidies. Your 2026 auto-renewal came through at $650/month. You didn't pay because you're still figuring out alternatives. March 31 is your decision deadline.

Scenario 2: The MAGI miscalculation. You estimated your 2026 income at $70,000 for a couple (safely under the 400% FPL cliff at $81,920 for a household of two). But you forgot that your December 2025 mutual fund capital gains distributions hit your 2026 tax return indirectly — and a Roth conversion you planned for January pushed your projected MAGI over the cliff. Now you're questioning whether ACA coverage is worth it at full price.

Scenario 3: The coverage gap strategy. You're 58, healthy, and thinking about going uninsured until Medicare at 65. Seven years without coverage. This is almost always a mistake — one emergency room visit can cost more than seven years of premiums.

Your Options Before March 31

Option 1: Pay and Keep Your Plan

If your 2026 premium is manageable — even if higher than 2025 — pay it. You maintain continuous coverage. You can adjust your plan during 2027 Open Enrollment once you have a clearer picture of your income and subsidy eligibility.

Option 2: Pay, Then Optimize Your MAGI

The smarter play for most early retirees: activate your coverage now, then spend the rest of 2026 managing your MAGI to stay under the 400% FPL cliff. If your income comes in lower than estimated, you'll get the excess Premium Tax Credit back as a refund when you file your 2026 taxes.

Key MAGI levers for early retirees:

- Time your Roth conversions carefully. Every dollar converted counts as income. Use our ACA Cliff Calculator to model exactly how much you can convert before triggering the cliff.

- Harvest capital gains in the right year. If you're close to the cliff, defer realized gains to a year where you've already exceeded 400% FPL.

- Watch for surprise income sources — mutual fund distributions in December, interest income, even municipal bond interest (which counts toward MAGI despite being tax-exempt).

Option 3: Let Coverage Lapse (Risky)

If you let March 31 pass without paying, you lose your 2026 plan. You would need a qualifying life event (marriage, move, income change, etc.) to get a Special Enrollment Period. Otherwise, you wait until November 2026 Open Enrollment for 2027 coverage.

For early retirees under 65, this creates a dangerous gap. Healthcare costs in early retirement average $380,000 to $500,000 before Medicare eligibility. One major medical event without coverage can wipe out years of careful FIRE planning.

The Real Question: Can You Afford the Cliff?

The 2026 ACA landscape forces early retirees into a calculation that didn't exist before:

If your MAGI stays under 400% FPL: ACA coverage is heavily subsidized. A couple at 300% FPL might pay $400-600/month for a Silver plan.

If your MAGI exceeds 400% FPL by even $1: You owe back the full subsidy. That's potentially $20,000+ in repayment on your tax return — with no cap on the amount.

This isn't a decision you can make by guessing. You need to model your specific income sources, Roth conversion plans, and capital gains timing against the cliff threshold. Our ACA Cliff Calculator does exactly this — input your income sources and see where you stand relative to the 400% FPL threshold in real time.

What to Do This Weekend

- If you haven't paid your 2026 premium: Pay it before Monday. March 31 is Tuesday. Don't let coverage lapse by accident.

- If you're debating whether ACA is worth it: Run your numbers through the ACA Cliff Calculator. See your actual subsidy amount at your projected income.

- If you already paid but your premium doubled: Start MAGI planning now. You have nine months to manage your 2026 income. Roth conversion timing, capital gains harvesting, and income smoothing can recover thousands in subsidies.

The March 31 deadline is a forcing function. Use it.

QuantCalc's ACA Cliff Calculator models your specific income against the 2026 subsidy cliff — including Roth conversions, capital gains, Social Security, and IRMAA thresholds. Free to use, no signup required.