Tax-Loss Harvesting in 2026: A Practical Guide for DIY Investors

You have winners and losers in your portfolio. The losers feel bad. But they have a hidden value most investors ignore: each unrealized loss is a potential tax deduction sitting in your brokerage account, waiting to be used.

Tax-loss harvesting is the practice of selling investments at a loss to offset capital gains taxes on your winners. Done right, it can save you thousands per year. Done wrong, it triggers IRS wash sale rules and costs you the deduction entirely.

Here is how it actually works in 2026, including the brackets, thresholds, and traps that matter.

How Tax-Loss Harvesting Works

The concept is simple:

- You sell an investment that has declined below your purchase price, realizing a loss.

- You use that loss to offset capital gains you realized elsewhere in the same year.

- If your losses exceed your gains, you can deduct up to $3,000 against ordinary income.

- Any remaining losses carry forward to future tax years indefinitely.

The key insight: you are not losing money by selling. You already lost it when the investment declined. Harvesting the loss simply converts that paper loss into a tax benefit.

Run your own numbers in the free calculator →

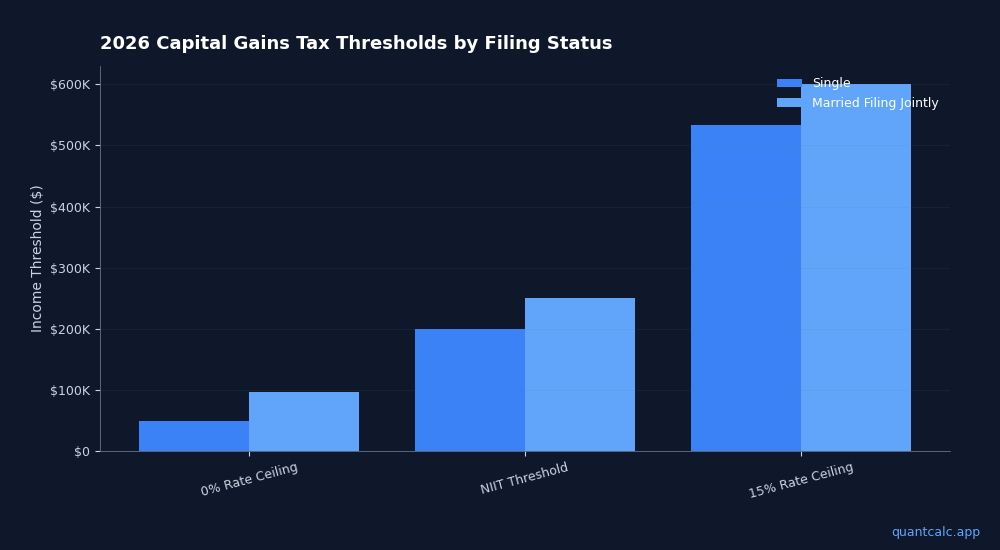

2026 Capital Gains Tax Brackets

Under the OBBBA (One Big Beautiful Bill Act), which made TCJA tax brackets permanent, the 2026 long-term capital gains rates are:

Single filers:

- 0% on taxable income up to $48,475

- 15% on income from $48,476 to $533,400

- 20% on income above $533,400

Married filing jointly:

- 0% on taxable income up to $96,950

- 15% on income from $96,951 to $600,050

- 20% on income above $600,050

On top of these rates, the Net Investment Income Tax (NIIT) adds 3.8% for singles with modified AGI above $200,000 or married couples above $250,000. This means the effective top rate on long-term capital gains is 23.8%.

Short-term capital gains (assets held less than one year) are taxed as ordinary income at rates up to 37%.

Why this matters for harvesting: Every dollar of realized loss offsets a dollar of realized gain. If you are in the 15% LTCG bracket with NIIT exposure, a $10,000 harvested loss saves you $1,880 in federal taxes. In the 20% + NIIT bracket, that same loss saves $2,380.

The Wash Sale Rule: The One Trap That Kills the Strategy

The IRS wash sale rule (Section 1091) prohibits you from claiming a loss if you buy a "substantially identical" security within 30 days before or after the sale. The rule applies across all your accounts, including your spouse's accounts, IRAs, and 401(k)s.

What counts as substantially identical:

- The exact same stock or ETF (obviously)

- Options on the same security

- Mutual funds tracking the same index from the same fund family (debated, but risky)

What does NOT count as substantially identical:

- A different ETF tracking a similar but distinct index (e.g., selling a total market ETF and buying an S&P 500 ETF)

- Individual stocks in the same sector (selling Apple and buying Microsoft)

- A mutual fund and an ETF from different providers tracking different indexes

The penalty for violating it: Your loss is disallowed. It gets added to the cost basis of the replacement shares, which defers the tax benefit but does not eliminate it entirely. The problem is losing the deduction in the current tax year when you need it.

Practical approach: When you harvest a loss, immediately replace the position with a similar but not identical investment to maintain your portfolio allocation. Wait 31 days, then switch back to your original holding if desired.

Run your own harvest before reading on

Full Schedule D netting, the $3,000 limit, wash-sale checking and multi-year carryforward — free, in your browser.

Open the harvesting calculator →When Tax-Loss Harvesting Makes Sense

Not every loss is worth harvesting. Consider these situations:

High-value scenarios:

- You have large realized capital gains from selling a property, exercising stock options, or rebalancing

- You are in the 15%+ LTCG bracket and want to offset gains dollar-for-dollar

- You have recurring capital gains from dividend reinvestment or fund distributions

- You are approaching retirement and want to reduce taxable income for ACA premium subsidy eligibility

Low-value scenarios:

- Your total income puts you in the 0% LTCG bracket (you would pay zero tax on gains anyway)

- The transaction costs of selling and rebuying exceed the tax savings

- You are harvesting a loss on a position you believe will recover soon, and you cannot find a suitable replacement

Tax-Loss Harvesting for Early Retirees

If you are planning for or currently in early retirement, tax-loss harvesting becomes a strategic tool beyond simple tax reduction:

MAGI management. Your modified adjusted gross income determines your ACA health insurance subsidy. Every dollar of realized capital gains increases your MAGI. Harvesting losses to offset gains keeps your MAGI below the 400% FPL cliff where subsidies disappear entirely.

Roth conversion optimization. If you are running a Roth conversion ladder, harvested losses can offset the conversion income, effectively reducing the tax cost of moving money from traditional to Roth accounts.

IRMAA avoidance. For retirees approaching Medicare age, MAGI above certain thresholds triggers Income-Related Monthly Adjustment Amounts that increase your Medicare premiums. Harvested losses help keep MAGI below these thresholds.

A Year-Round Strategy, Not a December Rush

The best time to harvest losses is whenever they appear, not December 31. Markets dip throughout the year. A position that is down 15% in March might recover by October, eliminating the harvesting opportunity.

Quarterly review cadence:

- Q1 (now): Review any positions that dropped during market volatility. Harvest losses before April 15 to offset any gains from rebalancing.

- Q2-Q3: Monitor during summer. Harvest opportunistically during corrections.

- Q4: Final pass before year-end. Pair with tax-efficient withdrawal strategies for retirement accounts.

Track Everything

Tax-loss harvesting requires careful record-keeping:

- Purchase date and price for every lot

- Sale date and proceeds

- Wash sale monitoring (30-day window before and after)

- Loss carryforward tracking across tax years

- Cost basis adjustments for partial sales

A Capital Gains Tax Harvesting Planner spreadsheet with lot-by-lot tracking and wash sale alerts makes this manageable. For quick calculations on any single trade, the Capital Gains Tax Calculator Chrome extension gives you instant federal + state + NIIT tax impact.

The Bottom Line

Tax-loss harvesting is not a loophole. It is a legitimate, IRS-recognized strategy that converts paper losses into real tax savings. The math is straightforward: if you are paying 15-23.8% on capital gains, every harvested loss puts money back in your portfolio.

The catch is execution. You need to track lots, avoid wash sales, and harvest consistently throughout the year. But the payoff compounds: $5,000-10,000 in annual tax savings over a 20-year retirement is $100,000-200,000 that stays invested and growing instead of going to the IRS.

Start with your Q1 2026 portfolio review. If you have positions in the red, they might be worth more as a tax deduction than as a comeback story.