Tax-Efficient Retirement Withdrawals: Which First?

You've spent decades saving in multiple account types — 401(k), traditional IRA, Roth IRA, taxable brokerage, maybe an HSA. Now you need income. The question nobody prepared you for: which account do you pull from first?

The conventional wisdom says "taxable first, then tax-deferred, then Roth last." That advice is wrong for most early retirees in 2026 — and the mistake can cost tens of thousands in unnecessary taxes over a 30-year retirement.

The Conventional Withdrawal Order (And Why It Fails)

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →The standard recommendation:

- Taxable accounts (brokerage)

- Tax-deferred accounts (traditional IRA, 401k)

- Tax-free accounts (Roth IRA)

The logic seems sound: let tax-deferred accounts grow longer, save Roth for last. But this ignores three critical factors that changed under OBBBA:

- ACA premium tax credit cliff at 400% FPL — withdrawals from traditional accounts count as MAGI income and can trigger full subsidy repayment

- IRMAA surcharges — Medicare Part B and D premiums jump at specific MAGI thresholds ($106,000 single, $212,000 married in 2026)

- RMD time bomb — large traditional balances create forced withdrawals at age 73+ that push you into higher brackets

Run your own numbers in the free calculator →

The Tax-Aware Withdrawal Strategy for 2026

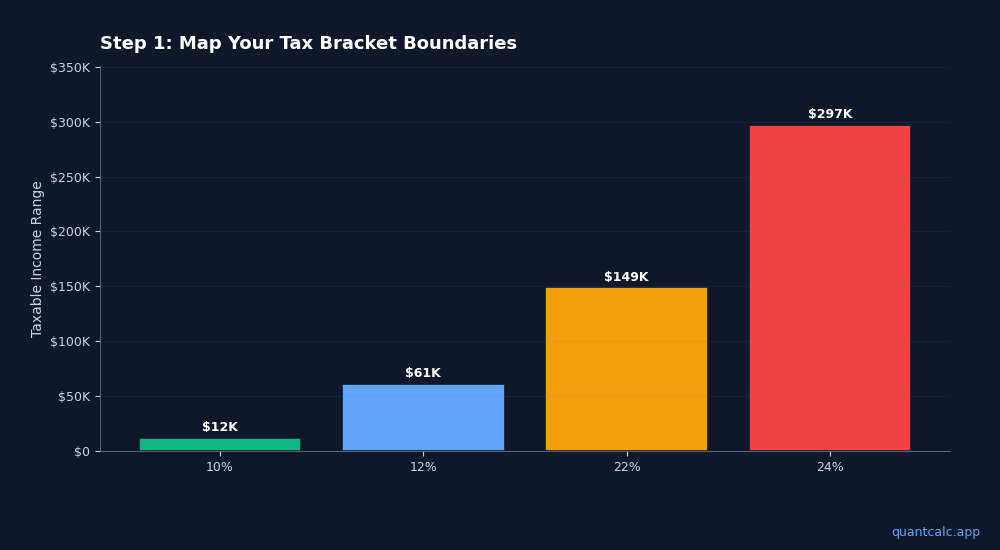

Step 1: Map Your Tax Bracket Boundaries

Under OBBBA (permanent since July 2025), the 2026 federal brackets for a married couple filing jointly are:

| Bracket | Taxable Income Range |

|---|---|

| 10% | $0 - $24,150 |

| 12% | $24,151 - $98,100 |

| 22% | $98,101 - $199,750 |

| 24% | $199,751 - $394,600 |

Your standard deduction is $32,900 (married filing jointly, 2026). That means a married couple can have $131,000 in gross income before hitting the 22% bracket.

Step 2: Fill Low Brackets Intentionally

Instead of blindly following the conventional order, fill your lowest tax brackets with traditional IRA/401(k) withdrawals first. If your annual spending is $60,000:

- Take $32,900 from traditional IRA (covered by standard deduction = 0% tax)

- Take $24,150 from traditional IRA (taxed at 10%)

- Take the remaining $2,950 from traditional IRA (taxed at 12%)

Total tax: $0 + $2,415 + $354 = $2,769 on $60,000 income (4.6% effective rate).

If you followed the conventional order and pulled from your brokerage first, your traditional IRA balance grows — and eventually forces RMDs at higher brackets.

Step 3: The Roth Conversion Bridge

The real power move: during years when your income is low (early retirement before Social Security), convert traditional IRA dollars to Roth at low rates.

Example: You need $60,000 to live. Instead of withdrawing $60,000 from traditional:

- Withdraw $60,000 from traditional IRA for spending

- Convert an additional $38,100 to Roth (filling the 12% bracket completely)

- Total MAGI: $98,100 (just under the 22% threshold)

- Tax on the conversion: ~$4,572

- Lifetime savings: That $38,100 in Roth grows tax-free forever, and you've reduced future RMDs

Step 4: Watch the ACA Cliff

If you're under 65 and buying health insurance on the ACA marketplace, your withdrawal strategy must account for the 400% FPL threshold.

For 2026, 400% FPL for a household of 2 is approximately $84,600. Exceed that by even $1 and you lose your entire premium tax credit — potentially $15,000+ in subsidies.

This means:

- Keep MAGI below 400% FPL during ACA years (before Medicare at 65)

- Use Roth withdrawals for spending above the MAGI limit (Roth doesn't count as MAGI)

- Time Roth conversions carefully — conversion income counts toward MAGI

- Consider capital gains harvesting at 0% rate within remaining MAGI headroom

Step 5: The IRMAA Trap at 65+

Once you're on Medicare, the game changes. IRMAA surcharges kick in at $106,000 (single) or $212,000 (married) in 2026. Each tier costs $1,000-$4,000+ per year in additional premiums.

Large RMDs from traditional accounts can push you over IRMAA thresholds. The withdrawals you make (or don't make) in your 50s and 60s directly impact your Medicare costs in your 70s and 80s.

The Optimal Sequence for Most Early Retirees

Here's the withdrawal priority that minimizes lifetime taxes for most FIRE retirees in 2026:

- HSA for medical expenses only (triple tax advantage)

- Roth IRA for spending above your MAGI target (preserves ACA subsidies)

- Traditional IRA/401(k) up to your target bracket ceiling (fills low brackets)

- Roth conversions with any remaining bracket space (reduces future RMDs)

- Taxable brokerage for capital gains harvesting at 0% rate

- Social Security — delay to 70 if possible (8% guaranteed return per year of delay)

Why a Spreadsheet Isn't Enough

The interactions between ACA subsidies, IRMAA brackets, Roth conversion windows, RMD schedules, and Social Security timing create a multi-variable optimization problem. A simple "which account first" rule fails because the right answer changes every year based on your income, age, and health insurance situation.

Monte Carlo simulation can model thousands of market scenarios to stress-test your withdrawal plan. Combined with ACA cliff analysis, you can find the exact withdrawal mix that maximizes after-tax income while protecting your subsidies.

Our free retirement planning tools let you model these scenarios with 10,000 Monte Carlo simulations, forward-looking forecast data from CME, BlackRock, JPMorgan, Vanguard, GMO, Schwab, and Invesco — and integrated ACA/IRMAA awareness that most calculators ignore.

The Bottom Line

The "right" withdrawal order depends on your specific tax situation, not a one-size-fits-all rule. The conventional advice to drain taxable accounts first often costs early retirees $50,000-$100,000+ in unnecessary lifetime taxes.

The three questions that determine your optimal strategy:

- Are you buying ACA health insurance? (If yes, MAGI management is priority #1)

- How large is your traditional IRA/401(k) balance relative to future RMDs?

- What's your current marginal tax bracket vs. your expected bracket at 73+?

Start with those three answers and work backward. Your future self will thank you.

Related reading: