When to Claim Social Security: Early Retiree Break-Even

Every early retiree eventually faces the same question: should you claim Social Security at 62, wait until full retirement age at 67, or hold out until 70 for the maximum benefit? The standard advice — "just calculate your break-even age" — is incomplete. For FIRE retirees managing ACA subsidies, Roth conversions, and IRMAA thresholds, the claiming decision changes everything about your tax picture for decades.

Here is the real math, including the pieces most calculators leave out.

The Basic Break-Even Numbers

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

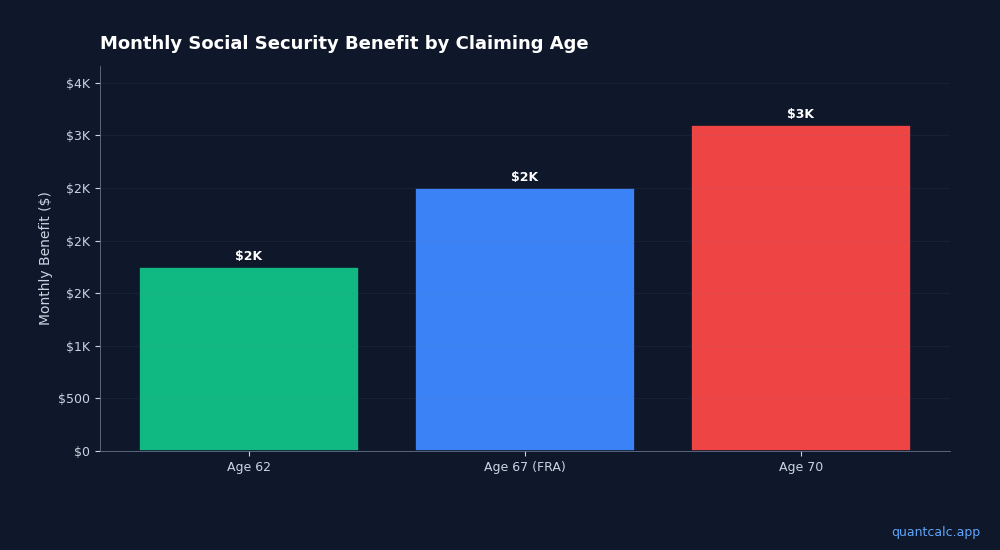

Try QuantCalc Free →Let's start with the straightforward comparison. Assume your full retirement age (FRA) benefit at 67 is $2,500/month.

Claiming at 62: Your benefit is permanently reduced by 30%. You receive $1,750/month — but you collect for five extra years before someone waiting until 67 gets their first check.

Claiming at 67: You get the full $2,500/month.

Claiming at 70: Delayed retirement credits add 8% per year past FRA. Your benefit grows to $3,100/month — a 24% bonus over the age-67 amount.

The crossover points:

- 62 vs. 67: The person who waited until 67 catches up around age 79. After that, every month favors the later claimer.

- 62 vs. 70: The age-70 claimer overtakes the age-62 claimer between age 80 and 81.

- 67 vs. 70: Waiting from 67 to 70 breaks even around age 82 to 83.

If you expect to live past your early 80s — and most healthy early retirees should — the math favors delaying. But this is where the standard analysis stops, and where it gets the FIRE case wrong.

Why Break-Even Analysis Misleads Early Retirees

The basic break-even calculation treats Social Security income in isolation. It asks: "When does total dollars received from one strategy exceed the other?" That is the wrong question for someone managing a multi-account retirement portfolio.

Here is what it misses:

1. Social Security Income Raises Your MAGI

Up to 85% of your Social Security benefits are taxable if your combined income exceeds $34,000 (single) or $44,000 (married filing jointly). For most FIRE retirees drawing from traditional IRAs, this threshold is easy to hit.

Every dollar of Social Security you receive pushes your Modified Adjusted Gross Income higher. Higher MAGI means:

- More of your Social Security is taxable (a feedback loop)

- Potential loss of ACA subsidies at the 400% FPL cliff

- Higher IRMAA surcharges on Medicare premiums

- Reduced ability to do tax-efficient Roth conversions

2. The Roth Conversion Window Closes When Benefits Start

The years between early retirement and Social Security claiming are the most valuable tax years of your life. Your taxable income is low — potentially near zero if you are living on Roth withdrawals or taxable account principal. This is your window to convert traditional IRA money to Roth at bottom-bracket tax rates.

Claim Social Security at 62 and that window shrinks by five years compared to claiming at 67. Claim at 70 and you get three more years of low-MAGI Roth conversion space.

For someone with a $750,000 traditional IRA, those extra years of conversions at the 12% bracket instead of the 22-24% bracket can save $50,000-$100,000 in lifetime taxes. That dwarfs the break-even calculation.

3. ACA Subsidy Cliffs Make Every Dollar of MAGI Count

If you retire before 65 and buy health insurance on the ACA marketplace, your subsidy depends on staying below 400% of the Federal Poverty Level. In 2026, that is roughly $62,600 for a household of one or $84,600 for a couple.

Social Security income counts toward MAGI. Claiming benefits while on ACA insurance can push you over the cliff and cost you $10,000-$20,000 per year in lost subsidies. Delaying Social Security until after Medicare kicks in at 65 eliminates this risk entirely.

Use our ACA Cliff Calculator to model exactly how Social Security income interacts with your subsidy eligibility.

The Real Decision Framework for FIRE Retirees

Forget the simple break-even chart. Here is how to think about Social Security claiming as part of your overall retirement tax strategy:

Claim Later (67-70) If:

- You have a large traditional IRA that needs Roth conversions before RMDs hit at 73

- You are on ACA insurance and need to keep MAGI below 400% FPL

- You are healthy with family longevity history suggesting you will live past 85

- You have enough in taxable and Roth accounts to bridge the gap without touching traditional IRA money

- Your spouse has a lower earning history and will rely on survivor benefits (delaying maximizes the survivor benefit)

Claim Earlier (62-64) If:

- You have minimal traditional IRA balances and no Roth conversion opportunity

- You have a serious health condition that reduces life expectancy below 78-80

- You have no ACA subsidy exposure (employer coverage, VA, or already on Medicare)

- You need the income to avoid selling investments in a down market (sequence of returns protection)

- The claiming decision is between 62 and 63, not 62 and 70 — small delays matter less

The Married Couple Strategy

For married couples, the highest earner should almost always delay to 70. Here is why: the survivor benefit equals the higher of the two spouses' benefits. If the higher earner dies first, the surviving spouse inherits that larger check for life.

The lower earner can claim earlier (62-64) to provide household income during the bridge years while the higher earner delays. This is not break-even math — it is longevity insurance for the surviving spouse.

How to Model This Properly

A break-even spreadsheet cannot capture these interactions. You need a tool that models Social Security timing alongside:

- Roth conversion amounts and tax brackets

- ACA subsidy eligibility year by year

- IRMAA thresholds and Medicare premium impacts

- Portfolio withdrawal sequencing across account types

- Monte Carlo simulation to stress-test across market scenarios

QuantCalc's retirement planner integrates Social Security modeling with all of these factors. You can toggle your claiming age and instantly see how it ripples through your tax projections, ACA eligibility, and portfolio survival probability across 10,000 simulated market scenarios.

The Bottom Line

The break-even age is a starting point, not an answer. For early retirees managing ACA subsidies, Roth conversions, and multi-account withdrawals, the tax interactions of Social Security claiming dwarf the simple "total dollars received" calculation.

Most FIRE retirees benefit from delaying Social Security — not because of break-even math, but because those extra years of low MAGI create a Roth conversion window and ACA subsidy protection worth tens of thousands of dollars.

Run the numbers with your actual portfolio. The answer depends on your specific accounts, your health, your spouse's situation, and your state taxes. But if you are making this decision with a break-even chart alone, you are almost certainly leaving money on the table.