Roth Conversion Ladder Strategy Explained (2026): Bracket-Fill Math & the 5-Year Rule

A Roth conversion ladder lets early retirees access 401(k)/IRA money before 59½ without the 10% penalty: convert a slice to a Roth IRA each year, wait 5 years, then withdraw the converted principal tax- and penalty-free. In 2026, a married couple with no other income can convert up to $133,000 a year while staying inside the 12% bracket — $11,600 of federal tax, an effective rate of roughly 8.7% on the full conversion. Build your own schedule with the free Roth Conversion Ladder Calculator.

You retired at 45. Your money is in a traditional 401(k). You can't touch it without a 10% penalty until 59½.

Or can you?

The Roth conversion ladder is the FIRE community's go-to strategy for accessing retirement funds early — completely penalty-free and often at a lower tax rate than you paid while working. Here's exactly how it works, including the 2026 tax implications most guides skip.

How a Roth Conversion Ladder Works

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →The basic mechanics are simple:

- Convert a portion of your traditional IRA or 401(k) to a Roth IRA each year

- Wait 5 years for that specific conversion to become accessible

- Withdraw the converted amount penalty-free and tax-free

The critical detail: you pay ordinary income tax on the conversion amount in the year you convert. But if you're in early retirement with little other income, you're converting at a much lower tax bracket than the one you were in while working.

The 5-Year Rule Deep Dive

The 5-year rule is the most misunderstood aspect of Roth conversion ladders. There are actually two separate 5-year rules that apply, and confusing them can cost you thousands in penalties.

The Conversion 5-Year Rule (The One That Matters for Ladders)

Each conversion has its own 5-year clock. A conversion made in January 2026 becomes accessible in January 2031. A conversion in 2027 is accessible in 2032. And so on.

The clock starts on January 1 of the tax year you make the conversion — not the actual date. A conversion on December 31, 2026 has the same 5-year clock as one made on January 2, 2026. Both become accessible January 1, 2031. This creates a planning opportunity: a late-December conversion gets nearly a full "free" year of clock time.

If you withdraw converted amounts before the 5-year clock expires, you pay the 10% early withdrawal penalty on those amounts (assuming you're under 59½). The income tax has already been paid at conversion — the penalty is the only additional cost.

The Contribution 5-Year Rule (Less Relevant)

There's a separate rule requiring your first Roth IRA to be open for 5 years before earnings qualify for tax-free treatment. If you already have a Roth IRA that's been open 5+ years, this rule is satisfied. If not, open one now — even with $1 — to start the clock.

Building Your 5-Year Bridge

This means you need a 5-year bridge — enough accessible money in taxable brokerage accounts, Roth contributions (not earnings), or cash to cover living expenses while your first conversions season.

Most FIRE planners build this bridge during their accumulation phase by directing some savings to taxable brokerage accounts alongside maxing out tax-advantaged space. A common target: 5 years of living expenses (typically $200,000-$400,000 for a couple) in taxable accounts before retiring.

Sources of bridge funding, in order of tax efficiency:

- Taxable brokerage accounts — long-term capital gains taxed at 0% if your taxable income is below $98,900 (MFJ 2026)

- Roth IRA contributions — always accessible tax-free and penalty-free (not earnings, just original contributions)

- Cash reserves — no tax impact, but inflation drag

- HSA funds — tax-free if used for qualified medical expenses (keep receipts from prior years)

- 72(t) SEPP — as a backup if bridge runs short (see comparison below)

2026 Tax Bracket Filling Strategy

The One Big Beautiful Bill Act (OBBBA, signed July 2025) permanently extended the TCJA tax brackets. This creates a window for Roth conversion ladders that may not get better.

Optimal Conversion Amounts by Filing Status

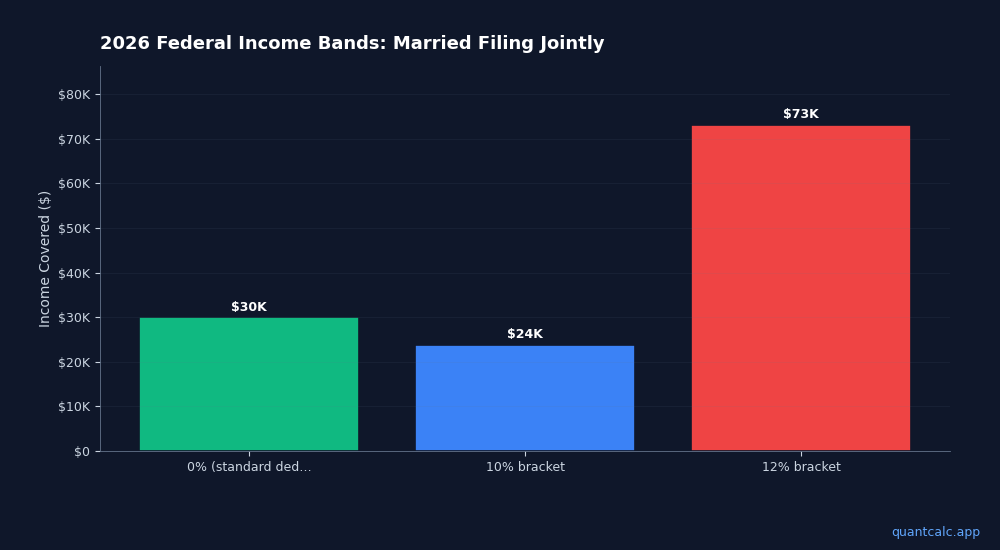

The key is converting enough to fill a low bracket without spilling into a higher one. Here are the 2026 numbers:

| Filing Status | Standard Deduction | Top of 10% Bracket | Top of 12% Bracket | Max Conversion at 12% |

|---|---|---|---|---|

| Single | $16,100 | $12,400 | $50,400 | $66,500 |

| Married Filing Jointly | $32,200 | $24,800 | $100,800 | $133,000 |

| Head of Household | $24,150 | $17,700 | $67,450 | $91,600 |

Max conversion at 12% = standard deduction + top of 12% bracket (taxable income). Assumes no other income. Source: IRS Rev. Proc. 2025-32.

A married couple in early retirement with no other income can convert up to $133,000 per year while staying in the 12% bracket — $11,600 of federal tax, an effective rate of roughly 8.7% on the full conversion.

Interactive version: the free Roth Conversion Ladder Calculator builds your full year-by-year schedule — federal tax per rung, the 5-year seasoning timeline, and ACA/IRMAA warnings — from the same verified 2026 dataset behind this table.

Compare that to the 22-24% marginal bracket they likely paid while working. Over a decade of conversions at $100,000/year, the tax savings versus converting at the 22% bracket exceed $100,000 in total.

The 22% Bracket Trap

Some planners suggest filling the 22% bracket for faster conversions. The math rarely supports this for ACA enrollees:

- The 22% bracket starts at $100,800 of taxable income (MFJ) — $133,000 gross once the standard deduction is added back

- At that income level, you've already lost ACA subsidies (400% FPL is $84,600 for a couple)

- You're paying 22% federal + state tax + losing $15,000-$25,000 in ACA subsidies

- Effective marginal rate: 40-60% when subsidy loss is included

The 12% bracket is the sweet spot for almost every early retiree on marketplace insurance.

The ACA Cliff Trap

Here's where most Roth conversion guides fail: they ignore health insurance.

If you're under 65 and buying insurance on the ACA marketplace, your conversion income counts as Modified Adjusted Gross Income (MAGI). Push your MAGI above 400% of the Federal Poverty Level and you fall off the ACA subsidy cliff, losing thousands in premium tax credits.

For 2026, the 400% FPL threshold for a married couple is $84,600. A couple converting $133,000 would blow past this threshold, potentially losing $15,000-$25,000 in ACA subsidies.

The optimal strategy: convert up to just below the ACA cliff threshold, not up to the top of the 12% bracket. Your MAGI needs to stay below 400% FPL while you're on marketplace insurance.

Our ACA Cliff Calculator models this exact tradeoff — it shows you the precise conversion amount that maximizes tax efficiency without sacrificing healthcare subsidies.

IRMAA: The Other Cliff

If you're within two years of Medicare eligibility (age 63+), large Roth conversions today can trigger Income-Related Monthly Adjustment Amount (IRMAA) surcharges on your Medicare premiums. IRMAA uses a 2-year lookback, so a big conversion at age 63 hits your Medicare premiums at age 65.

The planning window matters. Use the years between early retirement and age 63 for aggressive conversions, then throttle back as Medicare approaches.

3 Costly Roth Conversion Mistakes

Mistake 1: Converting Too Much and Triggering IRMAA

IRMAA surcharges use a 2-year income lookback. A $150,000 Roth conversion at age 63 shows up as income when Medicare premiums are set at age 65. The first IRMAA bracket starts at $109,000 (single) / $218,000 (MFJ) for 2026. Exceeding it costs about $974/person/year in Part B surcharges plus $174/person/year in Part D — roughly $2,297/year extra for a couple.

The fix: front-load conversions before age 63. Every year between early retirement and age 63 is prime conversion territory where neither the ACA cliff nor IRMAA lookback limits you. After 63, throttle back to stay under IRMAA thresholds.

Mistake 2: Forgetting the Pro-Rata Rule

If you have both pre-tax and after-tax (non-deductible) money in your traditional IRA, the pro-rata rule applies to every conversion. You cannot selectively convert only the after-tax portion.

Example: Your traditional IRA has $400,000 pre-tax and $100,000 after-tax (non-deductible contributions). That's 80% pre-tax. Every $50,000 conversion is taxed on $40,000 (80%) regardless of which dollars you intended to convert.

The workaround: Roll the pre-tax balance into a current employer's 401(k) before converting. This isolates the after-tax IRA money, allowing a tax-free conversion of the basis. This is the "backdoor Roth" cleanup step that many early retirees skip.

Mistake 3: Ignoring State Taxes on Conversions

Federal tax is only part of the picture. In states like California (13.3% top rate), New York (10.9%), or Oregon (9.9%), Roth conversion income is taxed at your marginal state rate. State tax can add thousands per conversion on top of the $7,640 of federal tax a couple pays on a $100,000 conversion with no other income.

Some states exempt retirement income or have lower rates on it. And nine states have no income tax at all. For early retirees with geographic flexibility, relocating before starting conversions can save $50,000+ over a decade. The Roth conversion ladder is most powerful in zero-income-tax states: Florida, Texas, Nevada, Wyoming, Washington, South Dakota, Alaska, Tennessee, and New Hampshire. See exactly how your state treats conversion income in our retirement tax by state guide — all 51 jurisdictions covered.

Step-by-Step: Building Your Ladder

Years 1-5 (Bridge Period):

- Live off taxable brokerage accounts, Roth contributions, and cash

- Convert an amount each year that stays below the ACA cliff (if on marketplace insurance) or fills the 12% bracket (if you have other coverage)

- Pay the tax on each conversion from non-retirement funds

Year 6+:

- Your Year 1 conversion is now accessible

- Withdraw that amount tax-free and penalty-free

- Continue converting each year to keep the ladder going

- Each subsequent year, another rung becomes accessible

Example: A couple retiring at 45 converts $75,000/year (staying below the ACA cliff). They pay $4,640 in federal tax per conversion — a 6.2% effective rate. Starting at age 50, they can withdraw $75,000/year from those seasoned conversions — tax-free and penalty-free. Meanwhile, they continue converting, creating a self-sustaining income stream.

What About 72(t) SEPP?

The alternative to a Roth conversion ladder is a 72(t) Substantially Equal Periodic Payment plan, which also avoids the 10% early withdrawal penalty. But 72(t) is inflexible — once you start, you're locked in for 5 years or until age 59½ (whichever is longer). Change the payment amount and the penalty applies retroactively to every withdrawal.

The Roth conversion ladder gives you far more control over timing and amounts. Most FIRE planners prefer it for that reason.

Case Study: Couple Retiring at 45 With $800K Traditional IRA

Meet Sarah and David. Both 45. Combined traditional IRA: $800,000. Taxable brokerage: $250,000. Annual spending: $65,000. They plan to use the Roth conversion ladder to access their retirement funds.

Years 1-5 (Bridge Period, ages 45-50):

- Live off taxable brokerage: $65,000/year ($325,000 total, exhausting taxable by year 5)

- Convert $75,000/year to Roth IRA (staying below the $84,600 ACA cliff for a couple)

- Federal tax on conversion: $4,640/year (6.2% effective; 12% marginal bracket)

- Maintain ACA subsidies: ~$12,000/year in premium tax credits preserved

- After 5 years: $375,000 converted to Roth, ~$425,000 remaining in traditional IRA (with growth)

Year 6+ (Ladder Active, age 50+):

- Year 1 conversion ($75,000) is now accessible — withdraw tax-free, penalty-free

- Continue converting $75,000/year from traditional IRA

- Each year, another rung of the ladder matures

- Traditional IRA gradually draws down while Roth balance grows

10-Year Summary (ages 45-55):

- Total converted: $750,000

- Total federal tax paid on conversions: $46,400 (6.2% effective)

- ACA subsidies preserved: ~$120,000

- Net tax cost versus converting the same $750,000 at a 22% marginal rate ($165,000): savings of $118,000+

- Traditional IRA remaining (with 6% growth): ~$300,000

- Roth IRA balance (with growth on converted amounts): ~$550,000

The conversion ladder transforms their retirement from "locked until 59½" to "fully funded and tax-optimized by 50." By the time they reach 59½, most of their wealth is in Roth accounts — permanently tax-free.

Running the Numbers

The variables that matter: your current tax bracket, expected retirement tax bracket, ACA subsidy amount, IRMAA exposure, bridge period length, and expected investment returns during the 5-year waiting period.

A Monte Carlo retirement simulator that accounts for all of these factors — especially the ACA cliff interaction — can show you the probability-weighted outcome of different conversion strategies. Our methodology uses 10,000 simulations with forward-looking return forecasts from CME, BlackRock, JPMorgan, Vanguard, GMO, Schwab, and Invesco.

Key Takeaways

- The Roth conversion ladder lets early retirees access 401(k)/IRA money before 59½, penalty-free

- Convert during low-income years to pay tax at 10-12% instead of 22-24%

- Each conversion has its own 5-year clock starting January 1 of the conversion year

- The 12% bracket is the sweet spot — filling the 22% bracket rarely makes sense for ACA enrollees

- Watch the ACA cliff: convert below 400% FPL ($84,600 for a couple in 2026)

- Front-load conversions before age 63 to avoid IRMAA lookback issues

- Watch for the pro-rata rule if you have mixed pre-tax and after-tax IRA money

- Build your year-by-year schedule with the free Roth Conversion Ladder Calculator, then stress-test it with a Monte Carlo simulator that models tax-aware withdrawal sequencing

Frequently Asked Questions

What is a Roth conversion ladder?

A Roth conversion ladder is a strategy where you convert money from a traditional IRA or 401(k) to a Roth IRA each year during early retirement, then withdraw those converted amounts tax-free and penalty-free after a 5-year waiting period. It is the primary method FIRE (Financial Independence, Retire Early) community members use to access retirement funds before age 59½ without paying the 10% early withdrawal penalty.

How does the 5-year rule work for Roth conversion ladders?

Each Roth conversion has its own separate 5-year clock. The clock starts on January 1 of the tax year you make the conversion — a December 31, 2026 conversion and a January 2, 2026 conversion both become accessible on January 1, 2031. If you withdraw converted amounts before the 5-year period ends and you are under 59½, you pay a 10% early withdrawal penalty on those amounts. The income tax on the conversion itself is paid in the year you convert, regardless of when you withdraw.

How much should I convert each year in a Roth conversion ladder?

The optimal conversion amount depends on your tax bracket, ACA subsidy eligibility, and IRMAA exposure. For 2026, a married couple with no other income can convert up to $133,000 while staying in the 12% federal bracket. However, if you rely on ACA marketplace insurance, the practical limit is lower — $84,600 (400% FPL for a couple) to preserve premium tax credits worth $15,000-$25,000/year. The Roth Conversion Ladder Calculator flags both limits for your exact filing status and household size.

Can a Roth conversion ladder affect my ACA health insurance subsidies?

Yes. Roth conversion income is included in Modified Adjusted Gross Income (MAGI) for ACA purposes. If your MAGI exceeds 400% of the Federal Poverty Level ($62,600 single / $84,600 couple in 2026), you lose all ACA premium tax credits and must repay any advance credits received. A single large conversion can trigger a $15,000-$25,000 clawback. Use QuantCalc's ACA Cliff Calculator to model the exact conversion amount that stays below the cliff.

Is a Roth conversion ladder better than 72(t) SEPP?

For most early retirees, yes. A 72(t) Substantially Equal Periodic Payment plan also avoids the 10% penalty but locks you into fixed withdrawals for 5 years or until age 59½ — whichever is longer. Change the payment amount and the penalty applies retroactively to every prior withdrawal. The Roth conversion ladder offers more flexibility: you control the conversion amount each year, can adjust for tax bracket changes, and the withdrawn amounts are completely tax-free after the 5-year period. The main advantage of 72(t) is that it provides immediate access without a 5-year wait.

Frequently Asked Questions

A Roth conversion ladder is a strategy where you convert money from a traditional IRA or 401(k) to a Roth IRA each year during early retirement, then withdraw those converted amounts tax-free and penalty-free after a 5-year waiting period. It is the primary method FIRE (Financial Independence, Retire Early) community members use to access retirement funds before age 59½ without paying the 10% early withdrawal penalty.

Each Roth conversion has its own separate 5-year clock. The clock starts on January 1 of the tax year you make the conversion — a December 31, 2026 conversion and a January 2, 2026 conversion both become accessible on January 1, 2031. If you withdraw converted amounts before the 5-year period ends and you are under 59½, you pay a 10% early withdrawal penalty on those amounts. The income tax on the conversion itself is paid in the year you convert, regardless of when you withdraw.

The optimal conversion amount depends on your tax bracket, ACA subsidy eligibility, and IRMAA exposure. For 2026, a married couple with no other income can convert up to $133,000 while staying in the 12% federal bracket. However, if you rely on ACA marketplace insurance, the practical limit is lower — $84,600 (400% FPL for a couple) to preserve premium tax credits worth $15,000-$25,000/year. The Roth Conversion Ladder Calculator flags both limits for your exact filing status and household size.

Yes. Roth conversion income is included in Modified Adjusted Gross Income (MAGI) for ACA purposes. If your MAGI exceeds 400% of the Federal Poverty Level ($62,600 single / $84,600 couple in 2026), you lose all ACA premium tax credits and must repay any advance credits received. A single large conversion can trigger a $15,000-$25,000 clawback. Use QuantCalc's ACA Cliff Calculator to model the exact conversion amount that stays below the cliff.

For most early retirees, yes. A 72(t) Substantially Equal Periodic Payment plan also avoids the 10% penalty but locks you into fixed withdrawals for 5 years or until age 59½ — whichever is longer. Change the payment amount and the penalty applies retroactively to every prior withdrawal. The Roth conversion ladder offers more flexibility: you control the conversion amount each year, can adjust for tax bracket changes, and the withdrawn amounts are completely tax-free after the 5-year period. The main advantage of 72(t) is that it provides immediate access without a 5-year wait.