72(t) SEPP Withdrawals: Access Retirement Funds Before 59.5

You're 50 years old, financially independent, ready to retire—but your nest egg is locked in traditional IRAs and 401(k)s, inaccessible until age 59½ without paying a brutal 10% early withdrawal penalty.

Except it's not quite true. There's a little-known IRS rule called 72(t) "Substantially Equal Periodic Payments" (SEPP) that lets you access your retirement funds penalty-free at ANY age—as long as you follow very specific rules.

This guide will show you exactly how 72(t) works, when it makes sense, how to calculate your payments, and the costly mistakes that can trigger massive penalties if you get it wrong.

What is a 72(t) SEPP?

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →72(t) SEPP refers to Internal Revenue Code Section 72(t), which allows penalty-free withdrawals from IRAs before age 59½ if you take "substantially equal periodic payments" based on your life expectancy.

How it works:

- You commit to taking equal (or nearly equal) annual withdrawals

- Withdrawals are calculated using IRS-approved methods

- You MUST continue for the longer of: 5 years OR until age 59½

- Follow the rules perfectly: No 10% penalty

- Break the rules: 10% penalty applies retroactively to ALL previous withdrawals + interest

Example:

- Age 50, start 72(t) SEPP

- IRA balance: $600,000

- Annual payment: $24,000 (using RMD method)

- Must continue until age 59½ (9.5 years)

- Total penalty-free withdrawals: $228,000

Key point: This is NOT tax-free. You still pay ordinary income tax on withdrawals. You're just avoiding the 10% early withdrawal penalty.

Run your own numbers in the free calculator →

When Does 72(t) SEPP Make Sense?

72(t) is powerful but rigid. Use it when:

1. You're Retiring Before 59½ and Need IRA/401(k) Money

- You've saved aggressively in tax-deferred accounts

- You don't have enough in Roth or taxable accounts to bridge to 59½

- You can't (or don't want to) do a Roth conversion ladder (which requires 5-year waiting periods)

2. You Have Stable, Predictable Expenses

- 72(t) locks you into fixed withdrawals—you can't increase them

- Best if your spending is consistent, not variable

3. You're Committed to Early Retirement (Not a Trial)

- Once you start, you MUST continue for 5+ years

- If you return to work or your needs change, you're stuck

72(t) is NOT for:

- Emergency access to funds (use Roth contributions or taxable accounts)

- Short-term needs (1-2 years of cash)

- Anyone who might need more flexibility

The Three IRS-Approved Calculation Methods

The IRS allows three methods to calculate your annual SEPP amount. Each produces different payment levels.

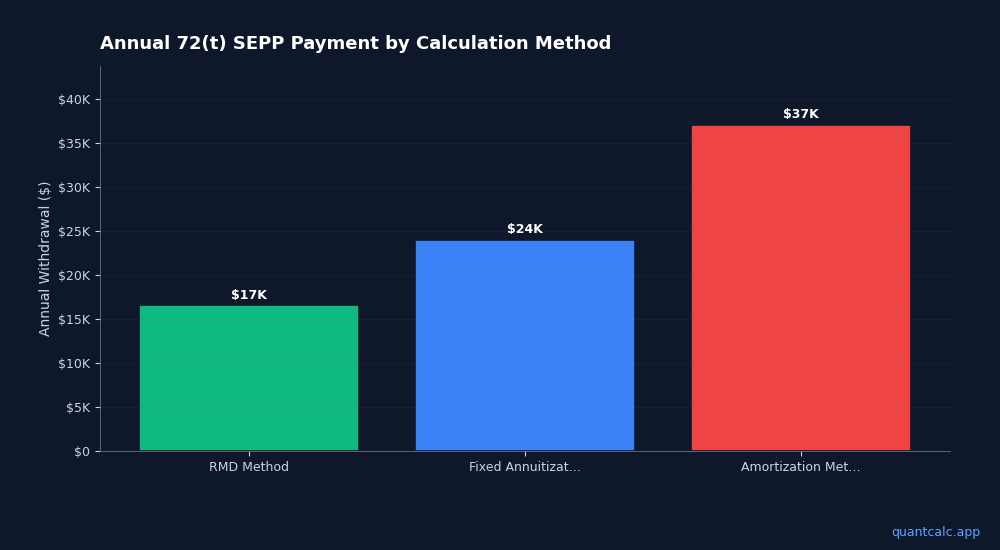

Method 1: Required Minimum Distribution (RMD)

Formula: Account balance ÷ Life expectancy factor (from IRS Single Life Table)

Example:

- Age: 50

- IRA balance: $600,000

- Life expectancy factor: 36.2 (from IRS table)

- Annual payment: $600,000 ÷ 36.2 = $16,575

Pros:

- Simplest method

- Lowest annual payment (good if you need less cash)

- Recalculates annually based on account balance (adjusts for market performance)

Cons:

- Payment varies year-to-year (not truly "equal" but IRS allows it)

- Might not provide enough income if you need more than ~2.5-3% of balance

Best for: Retirees who need modest withdrawals and want payments to adjust with market performance.

Method 2: Amortization

Formula: Account balance ÷ Present value annuity factor (based on life expectancy and interest rate)

Example:

- Age: 50

- IRA balance: $600,000

- Life expectancy: 36.2 years

- IRS interest rate: 5% (120% of federal mid-term rate)

- Annual payment: $37,080

Calculation: This uses annuity math (like a mortgage payment). The $600k is "amortized" over 36.2 years at 5%, producing fixed annual payments.

Pros:

- Higher payment than RMD method (60-100% more)

- Fixed amount (never changes)

- Better for retirees who need more income

Cons:

- Payment doesn't adjust for market crashes (you're stuck withdrawing $37k even if balance drops to $400k)

- Higher penalty risk if markets underperform

Best for: Retirees with large balances who need significant cash flow and are confident in portfolio longevity.

Method 3: Annuitization

Formula: Similar to amortization, but uses mortality table (expected lifespan accounting for probability of death).

Example:

- Age: 50

- IRA balance: $600,000

- Annual payment: ~$36,500 (slightly lower than amortization)

Difference from amortization: Annuitization assumes you might not live the full life expectancy (incorporates mortality risk), so payment is slightly lower.

Pros/Cons: Nearly identical to amortization method—rarely used because amortization is simpler and often produces higher payments.

Best for: Almost no one uses this (amortization is preferred).

How to Set Up a 72(t) SEPP

Step 1: Choose Which Account(s)

- You can start 72(t) on ONE IRA, not all of them

- Strategy: Open a separate IRA, transfer only the amount you need for SEPP, leave the rest untouched

- Why? Flexibility. You're only locked into SEPP on that one account.

Example:

- You have $800k in IRA

- You only need $25k/year from SEPP

- Transfer $400k to new "SEPP IRA"

- Start 72(t) on $400k (generates ~$25k/year)

- Leave $400k in original IRA (untouched, grows penalty-free, no SEPP restrictions)

Step 2: Choose Your Calculation Method

- RMD: If you need <3% of balance annually

- Amortization: If you need 4-6%+ annually

Run all three calculations before deciding. IRS guidance provides calculation details.

Step 3: Notify Your Custodian

- Contact your IRA custodian (Vanguard, Fidelity, Schwab, etc.)

- Inform them you're starting a 72(t) SEPP

- Provide calculation method and annual payment amount

- Request that custodian code withdrawals properly (avoid automatic 10% withholding)

Step 4: Document Everything

- Keep records of your calculation (balance, life expectancy, interest rate, method)

- Save annual distribution confirmations

- File IRS Form 5329 with your tax return (reports early distribution exception)

The 5-Year (or 59½) Rule: Don't Break It

The commitment: Once you start 72(t), you MUST continue taking the calculated payments for the LONGER of:

- 5 years, OR

- Until you reach age 59½

Examples:

- Start at age 50 → Must continue until age 59½ (9.5 years)

- Start at age 57 → Must continue until age 62 (5 years, which is longer than the 2.5 years until 59½)

- Start at age 45 → Must continue until age 59½ (14.5 years)

What happens if you break the rule:

- 10% early withdrawal penalty applies retroactively to ALL distributions

- Plus interest on the unpaid penalties

- Example: $25k/year for 5 years = $125k in distributions. Break the rule in year 6? You owe $12,500+ in penalties plus interest.

What Counts as "Breaking" the 72(t) SEPP?

You violate the SEPP if you:

1. Take more or less than the calculated amount

- If your calculation says $25,000, you must take $25,000 (not $24k, not $26k)

- Exception: RMD method recalculates annually, so amount changes each year (allowed)

2. Add money to the SEPP account

- No contributions, no rollovers into the SEPP account

- Exception: You can rollover into the account BEFORE starting SEPP, but not after

3. Take additional withdrawals outside the SEPP

- No emergency withdrawals, no loans, no exceptions

4. Stop taking distributions before the 5-year/59½ requirement

- Even if you return to work and don't need the money, you must continue

- Exception: If you die or become disabled, the SEPP ends without penalty

5. Change the calculation method mid-stream

- You're locked into your chosen method

- Exception: You can switch from amortization or annuitization to RMD method ONCE (one-time irrevocable election)

72(t) vs. Roth Conversion Ladder: Which is Better?

Both strategies provide penalty-free early access to retirement funds, but they're very different:

| Feature | 72(t) SEPP | Roth Conversion Ladder |

|---|---|---|

| Access timing | Immediate | 5 years after each conversion |

| Flexibility | None (locked in 5+ years) | High (stop/start conversions) |

| Amount control | Fixed by IRS formula | You choose how much to convert |

| Tax impact | Ordinary income on withdrawals | Ordinary income on conversions |

| Penalty risk | High if you break rules | Low (just follow 5-year rule) |

| Complexity | High (IRS calculations, strict rules) | Moderate |

When to use 72(t):

- You need money immediately (can't wait 5 years)

- You have large IRA balances and need significant income

- You're comfortable with fixed payments

When to use Roth conversion ladder:

- You have 5+ years before you need the money

- You want maximum flexibility

- You prefer lower penalty risk

Hybrid approach: Use taxable accounts or Roth contributions for years 1-5, while doing Roth conversions. Then access converted Roth funds starting in year 6. No need for 72(t).

(Full guide to Roth conversion ladders)

Common 72(t) Mistakes and How to Avoid Them

Mistake 1: Starting 72(t) Too Young

Starting at age 45 locks you in for 14.5 years. Life changes—job opportunities, inheritances, market crashes. Don't commit to SEPP unless absolutely necessary.

Solution: Use other strategies first (Roth conversions, taxable accounts, part-time work).

Mistake 2: Using Your Entire IRA for SEPP

If you start 72(t) on a $1M IRA, every dollar is subject to SEPP rules. No flexibility.

Solution: Split your IRA. Only put enough into SEPP IRA to generate the income you need. Leave the rest untouched.

Mistake 3: Choosing Amortization in a High-Valuation Market

If you lock in $40k/year withdrawals based on a $1M balance, and markets crash 50%, you're still stuck withdrawing $40k from a $500k balance—an 8% withdrawal rate that could deplete your account.

Solution: Use RMD method (recalculates annually) or be conservative with amortization (only use if you have a large buffer).

Mistake 4: Not Consulting a Professional

72(t) calculations are complex. One math error can trigger retroactive penalties.

Solution: Work with a CPA or financial advisor experienced in 72(t) planning. The cost of advice ($500-$1,500) is far less than a $10k+ penalty.

Mistake 5: Forgetting to File Form 5329

Even though you're taking penalty-free withdrawals, you must report them on Form 5329 to claim the exception.

Solution: Include Form 5329 with your annual tax return, noting exception code 02 (72(t) SEPP).

Can You Stop a 72(t) SEPP Early?

Technically, no—but there are three scenarios where it ends early without penalty:

1. You Die

The SEPP obligation dies with you. No penalty, even if 5 years haven't passed.

2. You Become Disabled

IRS-defined disability (unable to engage in substantial gainful activity) ends the SEPP without penalty.

3. You Reach Age 59½ and 5 Years Have Passed

Once you've met BOTH conditions (5 years AND age 59½), the SEPP ends. You can then take any amount penalty-free (standard IRA rules apply).

Important: Simply "wanting to stop" or returning to work is NOT an exception. You're locked in.

Modeling Your 72(t) SEPP Strategy

Before committing to 72(t), model it across market scenarios:

- What if markets return 7% annually? (Your balance grows despite withdrawals)

- What if markets crash 30% in year 2? (Will your fixed withdrawals deplete the account?)

- What if you live to 95? (Will your portfolio last?)

Use Monte Carlo simulation to test 72(t) across thousands of scenarios. See your probability of success and worst-case outcomes.

QuantCalc's retirement planner lets you model:

- Different withdrawal strategies (including custom rules like 72(t))

- Market sequence risk

- Asset allocation impact

- Success probability over 30-40 year horizons

You'll see whether 72(t) is safe for your situation or if alternative strategies (Roth ladder, taxable accounts, part-time income) are better.

The Bottom Line: Powerful But Unforgiving

72(t) SEPP is one of the few legal ways to access retirement funds before 59½ without penalties. For early retirees with large IRA balances and immediate cash needs, it's invaluable.

But it's rigid, complex, and unforgiving of mistakes. Break the rules—even accidentally—and you face retroactive penalties that can cost tens of thousands.

Before starting a 72(t) SEPP:

- Explore all alternatives (Roth conversions, taxable accounts, delay retirement 1-2 years)

- Model the strategy across market scenarios (make sure your portfolio can sustain the withdrawals)

- Consult a tax professional (the cost of advice is trivial compared to the penalty risk)

- Split your IRA (only use enough for SEPP, leave the rest flexible)

Done correctly, 72(t) can unlock financial independence years before traditional retirement age. Done wrong, it's a costly mistake.

Ready to model your early retirement strategy? Test 72(t) SEPP and alternative approaches with QuantCalc to find the safest path to financial independence.

Further Reading:

- Roth Conversion Ladder Strategy: A Step-by-Step Guide

- FIRE Movement Guide: How to Plan for Early Retirement

- The Complete Guide to Tax-Efficient Withdrawal Strategies

Frequently Asked Questions

What is IRS Rule 72(t)?

Rule 72(t) allows penalty-free withdrawals from retirement accounts before age 59½ through Substantially Equal Periodic Payments (SEPP).

Can you stop 72(t) payments early?

No. Once started, you must continue for 5 years OR until age 59½, whichever is longer. Stopping early triggers retroactive penalties on all distributions.

How much can you withdraw under 72(t)?

The amount is calculated using IRS-approved methods (RMD, amortization, or annuitization). You cannot choose an arbitrary amount.

Frequently Asked Questions

Rule 72(t) allows penalty-free withdrawals from retirement accounts before age 59½ through Substantially Equal Periodic Payments (SEPP).

No. Once started, you must continue for 5 years OR until age 59½, whichever is longer. Stopping early triggers retroactive penalties on all distributions.

The amount is calculated using IRS-approved methods (RMD, amortization, or annuitization). You cannot choose an arbitrary amount.