Will Congress Restore ACA Subsidies? Early Retiree Plan

The enhanced ACA subsidies expired at the end of 2025, and early retirees are feeling the impact — premiums have more than doubled for millions of marketplace enrollees. But there are signs Congress might act. The question for anyone planning around healthcare costs is: should you plan as if subsidies are gone forever, or bet on a legislative fix?

The answer is neither. You plan for both scenarios simultaneously.

Where Things Stand in Congress

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

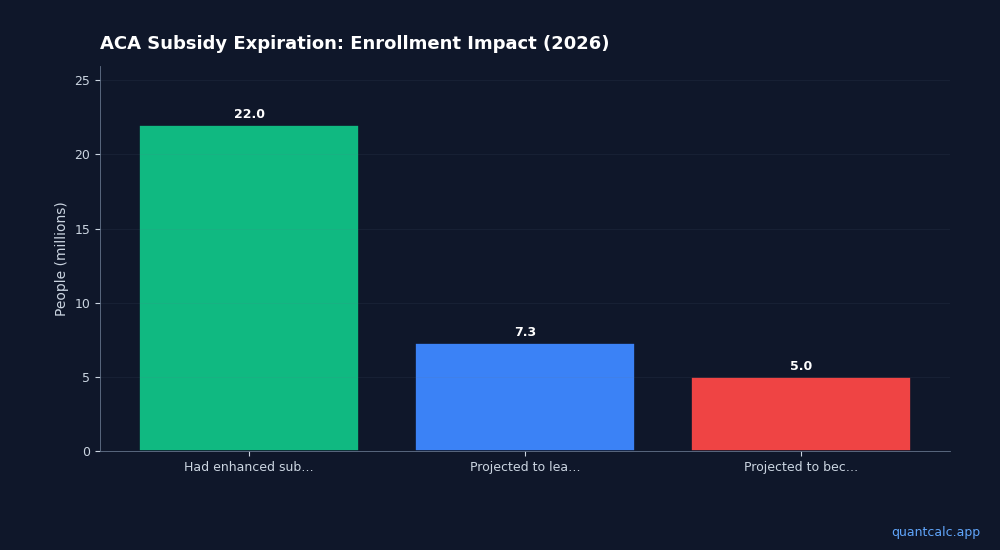

Try QuantCalc Free →The enhanced premium tax credits, which capped marketplace premiums at 8.5% of income regardless of earnings, were in place from 2021 through 2025 under the American Rescue Plan and Inflation Reduction Act. They reduced premiums for over 22 million people — more than 90% of all ACA marketplace enrollees.

Since the expiration, the Congressional Budget Office and independent groups like KFF have documented the fallout:

- Average annual premiums for consumers above the subsidy cliff jumped from roughly $4,400 to $8,500

- The Urban Institute and Commonwealth Fund estimate 7.3 million people will leave the ACA marketplace in 2026

- About 5 million of those are projected to become uninsured

These numbers have gotten attention on Capitol Hill. On January 8, 2026, the House of Representatives passed a three-year extension of enhanced premium tax credits. That was a significant step — but the Senate has not acted, and the path forward remains unclear.

The most likely vehicles are attachment to an appropriations bill or inclusion in a broader reconciliation package later in 2026. Some Senate Republicans have engaged in negotiations, but no companion bill has reached a vote. The timeline is uncertain, and the outcome is far from guaranteed.

The Problem With Waiting

For early retirees, the temptation is to delay financial decisions until Congress acts. That is a mistake for three reasons:

1. You cannot retroactively fix your 2026 MAGI. If Congress passes a subsidy extension in September, your income decisions from January through August are already locked in. Roth conversions you did in Q1 already count toward MAGI. Capital gains you realized are already on the books.

2. The cliff is real right now. Even if enhanced subsidies return, the 400% FPL cliff may remain in some form. The pre-2021 subsidy structure had this cliff — it was the enhanced version that eliminated it. A legislative compromise could restore subsidies while keeping income limits. To see exactly where your household sits relative to the threshold, run your numbers through the free ACA cliff calculator before locking in any irreversible income decisions this year.

3. Open enrollment for 2027 starts November 2026. Your 2026 income determines your 2027 subsidy eligibility under current rules. Decisions you make now compound into next year.

The Two-Scenario Strategy

Smart early retirees are running two parallel plans:

Scenario A: Subsidies stay expired (base case)

Manage your MAGI aggressively to stay below 400% FPL ($62,160 single / $84,640 couple in 2026):

- Prioritize Roth withdrawals. Roth IRA distributions do not count toward MAGI. If you have a Roth balance, use it to cover living expenses while keeping reported income below the cliff.

- Limit Roth conversions to the gap. Converting traditional IRA money to Roth is a good long-term move, but conversion income counts as MAGI. Convert only up to the amount that keeps you safely below 400% FPL.

- Spread capital gains across years. If you need to sell appreciated assets, do it in smaller chunks across multiple tax years rather than one large sale.

- Watch IRMAA thresholds. If you are within two years of Medicare eligibility, your 2026 income affects your 2028 Medicare Part B/D premiums. IRMAA surcharges start at $106,000 for individuals.

Scenario B: Congress restores enhanced subsidies

If subsidies return with the 8.5% income cap and no cliff, you have more flexibility:

- Roth conversions become more attractive because higher MAGI no longer triggers a subsidy cliff

- Capital gains harvesting can happen more freely

- The binding constraint shifts from ACA to IRMAA for those near Medicare age

The overlap

The key insight: everything you do under Scenario A is still beneficial under Scenario B. Keeping MAGI low preserves optionality. You lose nothing by being conservative now and loosening up later if the law changes.

The reverse is not true. If you assume subsidies are coming back and let your MAGI run high, you cannot undo that if Congress fails to act.

Model Both Scenarios

The QuantCalc ACA Cliff Calculator lets you model different withdrawal strategies against the current 400% FPL cliff. Input your account balances (taxable, traditional IRA, Roth), set your expected spending, and see exactly where your MAGI lands relative to the cliff under different withdrawal sequences.

Try running it twice: once with aggressive MAGI management (Scenario A), and once with a more relaxed approach (Scenario B). The dollar difference between those two scenarios is your "cliff exposure" — the amount you stand to lose if Congress does not act.

For most early retiree couples with $1-3M portfolios, that exposure is $8,000-$15,000 per year.

The Bottom Line

Bipartisan talks are encouraging but not a plan. No bill has been introduced, no vote has been scheduled, and the political dynamics make a clean extension uncertain. The smart move is to manage your 2026 income as if the cliff is permanent, while staying ready to adjust if legislation passes.

You can always convert more to Roth later. You cannot un-convert what you already did.

Sources: CNBC — ACA subsidy cliff tax bills, CNBC — ACA enhanced subsidy expiration effects, Healthinsurance.org — subsidy cliff return, MoneyGeek — ACA subsidy cliff by state