11 Days Left: Last-Minute Tax Moves Before April 15, 2026

The April 15, 2026 tax deadline is not just for filing your 2025 return. It is also the due date for your Q1 2026 estimated tax payment, your IRA and HSA contribution deadline for tax year 2025, and potentially the most expensive day of the year if you get the math wrong.

Here is what still matters with 11 days left on the clock.

1. File or Extend — But Do Not Just Ignore It

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →If you cannot file by April 15, file Form 4868 for an automatic 6-month extension. This is free, takes 5 minutes through IRS Free File, and eliminates the failure-to-file penalty (which is 5% of unpaid taxes per month, up to 25%).

The catch: An extension to file is not an extension to pay. You still owe any taxes due by April 15. Estimate what you owe, pay at least 90% of it, and file the full return by October 15.

The failure-to-pay penalty is 0.5% per month — much smaller than the failure-to-file penalty. If you are going to be late, at least file the extension.

Run your own numbers in the free calculator →

2. Make Your Q1 2026 Estimated Tax Payment

If you are self-employed, freelancing, or have significant investment income in 2026, your first quarterly estimated tax payment is due April 15. This covers income earned January through March 2026.

Miss this payment and you start accumulating underpayment penalties from day one. The current IRS underpayment rate is 7% annually — compounded daily.

Safe harbor rule: If you pay at least 100% of your 2025 tax liability across four equal quarterly payments (110% if your AGI exceeded $150,000), you avoid penalties regardless of how much you actually owe for 2026. This is the simplest strategy for freelancers with variable income.

Use the Freelancer Tax Estimator Chrome extension to calculate your exact quarterly payment in 30 seconds — it covers 2026 OBBBA-permanent brackets, self-employment tax, and all four quarterly deadlines.

3. Max Out Your 2025 IRA Contribution

You have until April 15, 2026 to make IRA contributions that count for tax year 2025. The 2025 limit is $7,000 ($8,000 if you are 50 or older).

For Traditional IRA: this may reduce your 2025 taxable income if you qualify for the deduction. For Roth IRA: no tax deduction now, but tax-free growth forever.

If you are an early retiree managing your MAGI for ACA subsidy eligibility, a Traditional IRA contribution directly reduces your MAGI and may keep you below the 400% FPL cliff.

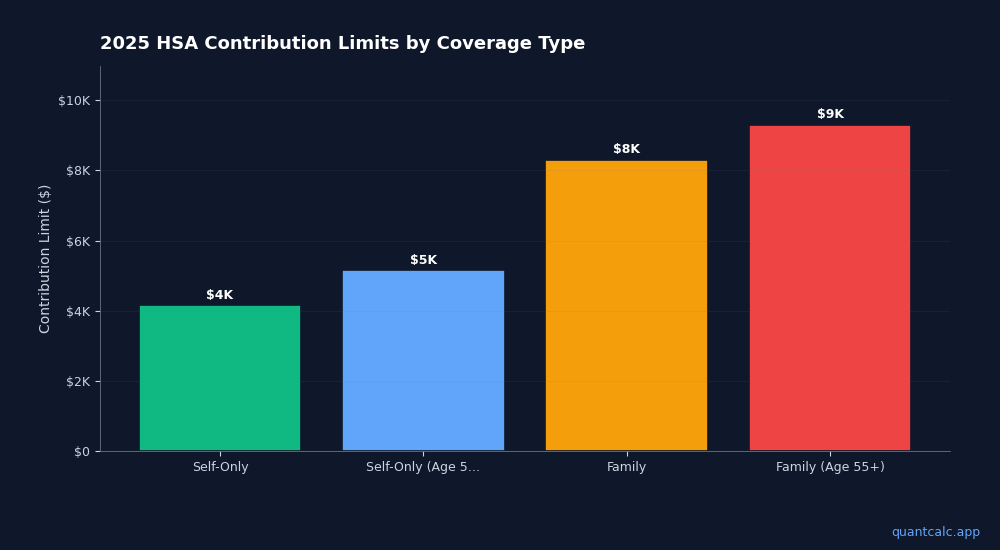

4. Fund Your HSA for 2025

Same April 15 deadline applies to Health Savings Account contributions for 2025. The 2025 limits were $4,150 (self-only) or $8,300 (family), with an additional $1,000 catch-up if you were 55 or older.

HSA contributions are triple-tax-advantaged: tax-deductible going in, tax-free growth, and tax-free withdrawals for qualified medical expenses. For FIRE planners, the HSA is the most tax-efficient account available.

New for 2026: Under the OBBBA, all ACA Bronze and catastrophic plans are now HSA-eligible starting January 1, 2026. This opens HSA contributions to 7.3 million newly eligible Americans.

5. Check Your Withholding for 2026

If you owed a large amount on your 2025 return, fix it now for 2026. Submit a new W-4 to your employer to increase withholding before Q2. The IRS Tax Withholding Estimator at irs.gov is free and takes about 15 minutes.

For W-2 employees who also freelance: your W-2 withholding counts toward your total tax liability for estimated payment purposes. If your W-2 job withholds enough to cover the safe harbor threshold, you may not need to make separate estimated payments at all.

The Paycheck Tax Calculator extension shows your exact federal and state tax on every paycheck — useful for verifying your W-4 is set correctly.

6. Side Hustlers: Do Not Forget Self-Employment Tax

If you earned $400 or more from self-employment in 2025 (or expect to in 2026), you owe self-employment tax at 15.3% on top of income tax. This catches many first-time freelancers by surprise.

The self-employment tax calculator breaks down exactly how much you owe, and the Side Hustle Tax Calculator Chrome extension handles multi-stream income, quarterly payments, and state tax.

Read the full guide: Side Hustle Taxes 2026: How to Keep More of Your Money.

7. Retirees: Plan Your 2026 Roth Conversions Now

April is when smart retirees start planning their Roth conversion strategy for the year. Why now? Because you need to know your expected income for the full year before deciding how much to convert.

Key considerations:

- Stay below the ACA cliff if you are on marketplace insurance

- Avoid IRMAA surcharges by managing your MAGI

- Convert enough to fill lower tax brackets without spilling into the next one

The Roth Conversion Calculator Chrome extension models the federal tax impact of different conversion amounts — critical for getting the math right.

For a comprehensive retirement plan that models all of this together, run a Monte Carlo simulation with forward-looking forecasts at QuantCalc.

The Bottom Line

April 15 is a hard deadline for five separate things: filing your 2025 return (or extension), paying your 2025 tax balance, making your Q1 2026 estimated payment, contributing to your 2025 IRA, and funding your 2025 HSA. Missing any of them triggers penalties that compound daily.

The math is not complicated — but it is specific to your situation. Use the free tools linked above to get your exact numbers before the deadline hits.