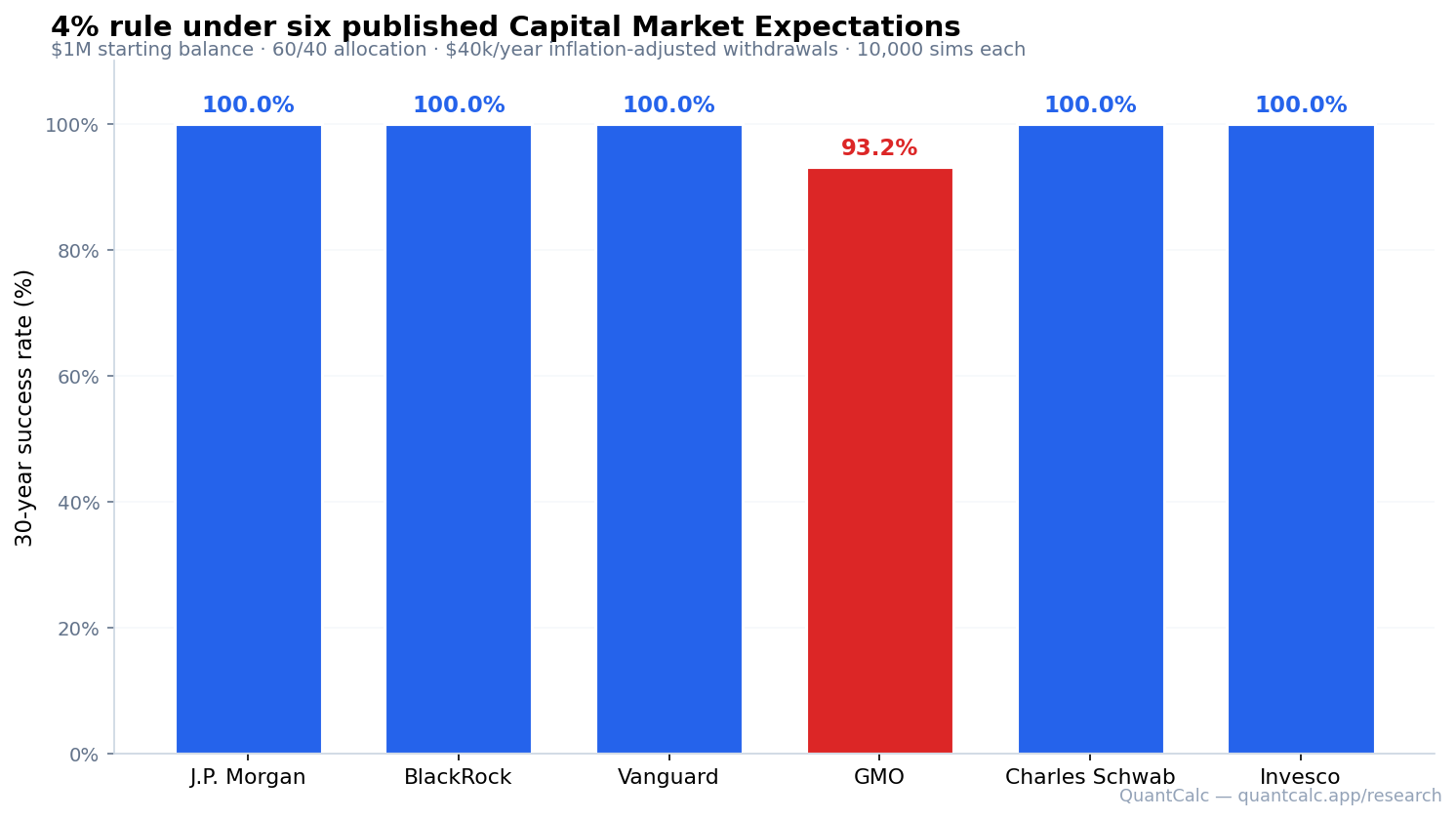

Under six published institutional capital-market forecasts, the classic 4% rule — $1M, 60/40, inflation-adjusted withdrawals over 30 years, no other income — reaches 100% success in none of 10,000-path Monte Carlo runs. Five forecasts cluster between 78.5% and 90.8% 30-year success; GMO's mean-reverting forecast breaks the rule outright at 2.5%. Among the surviving forecasts, median terminal wealth spans 2.3×, from $339,503 to $766,828, so the bequest you leave depends heavily on the forecast you anchor to. Run the same test on your own plan at quantcalc.app.

Key findings

- No forecast produces a 100% 30-year success rate for the canonical no-other-income 4%-rule scenario. Five cluster between 78.5% and 90.8% success (Charles Schwab 90.8%, J.P. Morgan 85.6%, Invesco 85.4%, BlackRock 84.4%, Vanguard 78.5%) — a real 1-in-10 to 1-in-5 chance of running out over 30 years.

- GMO's mean-reverting forecast breaks the rule outright: 2.5% success rate (97.5% of paths run out before year 30). GMO's published forecast assumes US equities revert from currently elevated valuations to a negative real return.

- Median terminal balance spans 2.3× across the five surviving forecasts: from $339,503 (Vanguard) to $766,828 (J.P. Morgan). Under GMO the median path ends at $0. Your "legacy" portfolio is even more sensitive to the forecast than your survival outcome.

- Direction of risk: under forward-looking forecasts, the 4% rule's safety margin is materially thinner than the historical backtest implies — the question is not just whether it survives but how often it doesn't.

The question

William Bengen's 1994 paper showed that a 4% inflation-adjusted withdrawal from a 50/50 stock-bond portfolio survived every rolling 30-year window in US history from 1926 to 1976. The "4% rule" became shorthand for safe retirement spending.

That study used historical US returns. Major asset managers — J.P. Morgan, BlackRock, Vanguard, GMO, Charles Schwab, Invesco — now publish forward-looking Capital Market Expectations: their best estimates of returns over the next 7 to 20 years. These forecasts often differ materially from historical averages, especially at current valuation levels.

So the question is concrete: when you swap historical returns for forward-looking expectations, does the 4% rule still hold?

This piece runs the same retirement plan through 10,000 Monte Carlo simulations under each of the six publicly-available forecasts and reports the result.

The plan

One canonical scenario, identical across all six forecasts:

| Parameter | Value |

|---|---|

| Starting balance | $1,000,000 |

| Asset allocation | 60/40 (45% US equity, 15% international equity, 40% bonds) |

| Initial withdrawal | $40,000 / year (4.0% of starting balance) |

| Withdrawal indexing | 2.5% / year (CPI-anchored) |

| Horizon | 30 years (age 65 → 95) |

| Simulations per forecast | 10,000 |

| Sampling | Pseudo-random (Mersenne Twister) — accurate tail estimation |

| Volatility & correlations | J.P. Morgan published values (used uniformly across all 6 return forecasts so only the return assumption varies) |

Holding volatility and correlations constant across runs is deliberate: it isolates the effect of each firm's return expectation. Some firms publish their own volatility and correlation estimates; others do not. Using one consistent set lets the comparison be apples-to-apples on the input that varies most across forecasts.

The forecasts

One sentence per source. Each links to its publicly available original. We use only data that has been reported publicly by the firm itself or in widely-circulated financial press; we do not source from paywalled or registration-gated portals.

| Forecast | US equity (nom.) | Bonds (nom.) | Source |

|---|---|---|---|

| J.P. Morgan | 6.7% | 4.8% | As published in Long-Term Capital Market Assumptions (annual). am.jpmorgan.com |

| BlackRock | 5.2% | 4.1% | As reported in Morningstar's annual Capital Market Expectations roundup (Christine Benz, "Experts Forecast Stock and Bond Returns: 2026 Edition") and other public financial media. |

| Vanguard | 4.5% | 4.2% | As published in Economic and Market Outlook (annual). corporate.vanguard.com |

| GMO | −3.5% | 3.8% | Headline figures from 7-Year Asset Class Forecasts (quarterly), as widely reported in financial press (Reuters, Bloomberg, FT). Real returns converted to nominal by adding 2.5% expected inflation. |

| Charles Schwab | 5.9% | 4.8% | As published in Schwab's Long-Term Capital Market Expectations. schwab.com/learn |

| Invesco | 5.3% | 4.5% | As published in Invesco's Capital Market Assumptions (annual). invesco.com |

Of the six, GMO is the outlier — a deliberate one. GMO's framework is mean-reverting: it adjusts current asset prices toward historical fair value over a 7-year horizon. With US large-cap equities trading at elevated cyclically-adjusted earnings multiples (Shiller P/E above 30 in late 2025), GMO's model produces negative real return forecasts for US stocks. The other five firms use building-block approaches that pencil in more modest valuation adjustments.

Result 1: success rate

Probability the portfolio survives 30 years without depletion, by forecast:

No forecast produces a 100% success rate. The five mainstream forecasts land between 78.5% (Vanguard) and 90.8% (Charles Schwab); GMO produces 2.5%, meaning 9,754 of 10,000 simulated paths exhausted the portfolio before year 30.

This is the instructive result. The forward-looking forecasts are lower than the long-run historical 1926–2025 averages (~10.2% nominal for US equity), and once the historical tailwind is removed the 4% rule's margin visibly thins: even the strongest forecast here leaves a roughly 1-in-11 chance of depletion over 30 years, and the weakest mainstream forecast a better-than-1-in-5 chance. Why does it still mostly hold?

Because the 4% rule's historical safety margin was wide to begin with. Bengen 1994's 100% historical success rate at 4% on a 50/50 portfolio held with room to spare — but that cushion was built on ~10% nominal US equity returns. Reducing the expected return to the 4.5–6.7% nominal that every forward-looking forecast here pencils in shrinks the margin enough that a 30-year run now carries a real, single-digit-to-low-double-digit failure probability under all five mainstream forecasts.

GMO breaks rank entirely because its US equity forecast goes negative. A portfolio whose largest single holding has a negative real expected return is a different mathematical object: not a smaller margin, but one that drifts in the wrong direction — and the near-total failure rate reflects it.

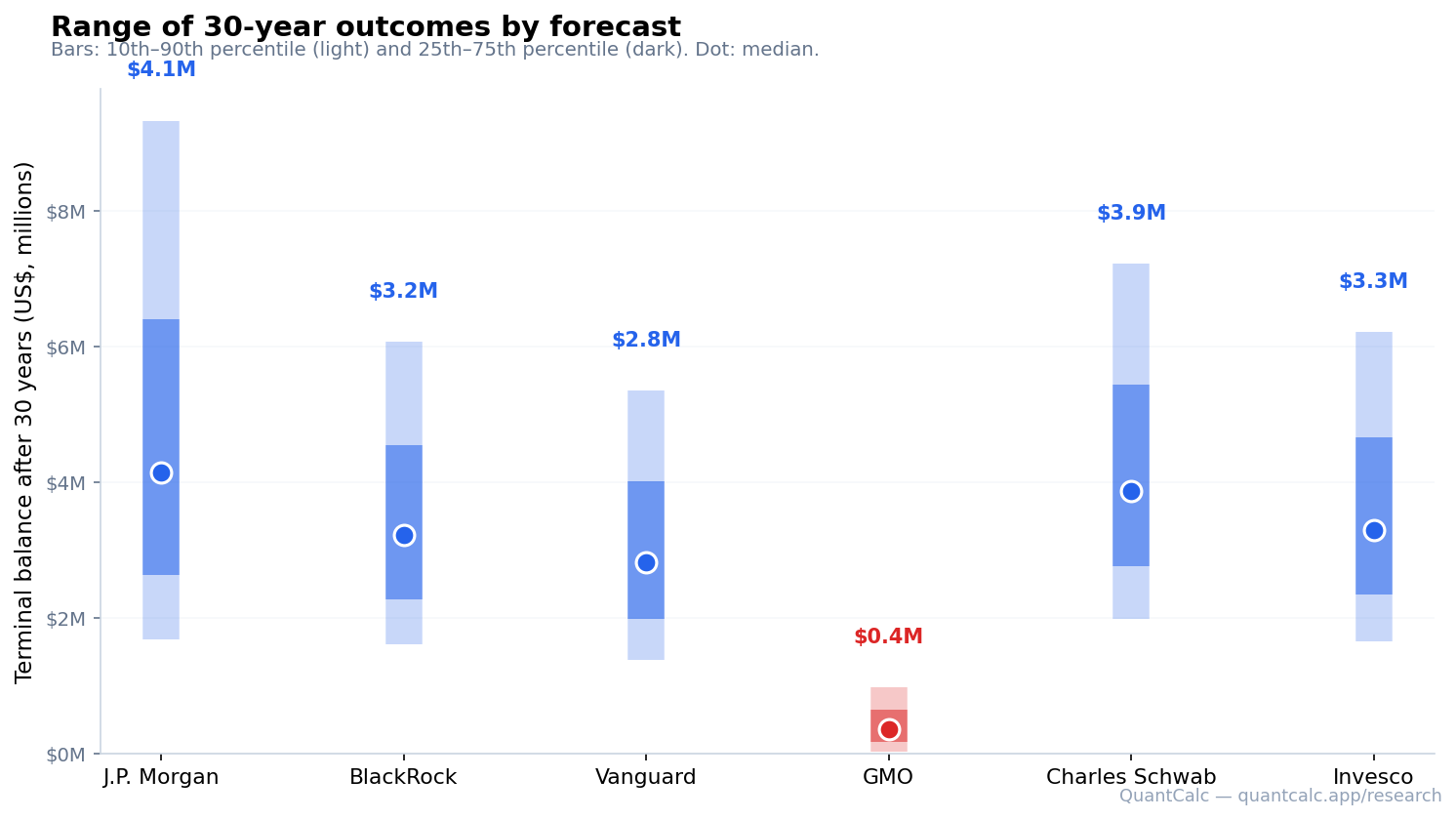

Result 2: terminal balance

The success-rate chart conceals most of what's interesting. Below: the distribution of terminal balances (after 30 years, in nominal US dollars) under each forecast. The dot is the median; the dark band is the 25th–75th percentile; the light band is the 10th–90th percentile.

The medians:

| Forecast | Median terminal balance | p10 | p90 |

|---|---|---|---|

| J.P. Morgan | $766,828 | $0 | $2,708,856 |

| Charles Schwab | $691,352 | $17,751 | $1,928,560 |

| Invesco | $498,086 | $0 | $1,564,214 |

| BlackRock | $471,499 | $0 | $1,513,260 |

| Vanguard | $339,503 | $0 | $1,261,060 |

| GMO | $0 | $0 | $0 |

The headline: even among the five forecasts that keep meaningful survival odds, median terminal balance spans 2.3× — from $339,503 (Vanguard) to $766,828 (J.P. Morgan) — for an identical plan. Under GMO the median path ends at $0, and every reported percentile through the 95th is $0.

That is a $427,325 difference in median legacy balance between Vanguard and J.P. Morgan for the same plan, the same allocation, the same withdrawal — and it sits on top of survival probabilities that themselves range from 78.5% to 90.8%. Note that the 10th percentile is $0 for five of six forecasts: in the worst tenth of outcomes, most of these forecasts leave nothing behind.

Why GMO is different

GMO is not pessimistic for its own sake. The firm's framework is explicit and reproducible: forecast US equity returns by reverting current valuations (P/E, Shiller CAPE, dividend yield) to a long-run mean over seven years.

At late-2025 valuation levels — Shiller CAPE above 30, well above the 1926–2024 historical mean near 17 — that mean-reversion implies several years of below-average price returns. Combined with mediocre starting dividend yields, the model produces a 7-year US equity total return forecast that GMO publishes as a negative real number. After conversion to nominal at a 2.5% inflation assumption, US equity is still roughly −3.5% per year.

For a portfolio that's 45% US equity, that is the difference between marginally building the portfolio and slowly bleeding it. The 4% rule does not survive a sustained negative real return on the largest equity holding, because the inflation-adjusted withdrawal grows at 2.5% per year while the asset shrinks. Sequence-of-returns risk amplifies it.

GMO's model has been historically right and historically wrong. They were notably correct that the late-1990s tech bubble would mean-revert, and notably early — and therefore wrong for years — about the 2010s bull market. We make no claim about whether their current forecast will turn out to be right. The point is that their model produces these numbers, the model is publicly documented, and a 4% retirement plan needs to address what happens if their forecast is correct.

What this implies for retirees

Three takeaways. None are advice — they're observations from the data.

1. Under forward-looking forecasts, the 4% rule carries real failure risk.

With no other income, none of the six forecasts reproduce the near-100% success rate the historical US record implies. The five mainstream forecasts fail in roughly 1-in-10 to 1-in-5 of 30-year paths. If your prior was that the 4% rule is close to a guarantee, this data says: only against historical returns. Against every published forward-looking forecast, the margin is meaningfully thinner.

2. It breaks entirely if a mean-reverting forecast is right about US equity valuations.

GMO's forecast is the extreme case, at 2.5% success. If you believe equity returns over the next decade will reflect mean reversion from elevated valuations rather than continued historical-average growth, a 4% withdrawal on a 60/40 portfolio is close to a coin flip that lands the wrong way — you would want a materially lower withdrawal rate or a different allocation.

3. Supplemental income and the bequest distribution both change the picture.

This scenario deliberately models a portfolio-only retirement — no Social Security, no pension. Most households have some floor of guaranteed income, which lifts these numbers; the calculator lets you add it. And the legacy distribution is wide: median terminal balance spans more than 2× across the surviving forecasts, and the 10th-percentile outcome is $0 for most of them. Retirees with bequest motives, or with longer-than-30-year horizons, get more decision-relevant signal from the full distribution than from the headline success rate alone.

Methodology

Engine

QuantCalc's Monte Carlo simulation engine, written in C, with correlated lognormal asset-return modeling via Cholesky decomposition of the published correlation matrix. Withdrawals are inflation-adjusted at a 2.5% deterministic CPI rate consistent with the post-1990 anchored inflation regime; further methodology on inflation available. Each simulation runs the full month-by-month portfolio path for 360 months (30 years).

Sampling

Pseudo-random (Mersenne Twister) draws were used as the canonical run rather than the engine's faster default Sobol quasi-Monte Carlo, because QMC is known to converge faster on means but to bias estimates of tail probabilities. The article numbers come from pseudo-random sampling. We re-ran the same scenario under both QMC variants as a robustness check; the comparison appears below.

| Forecast | Sobol QMC | Sobol QMC (scrambled) | Pseudo-random |

|---|---|---|---|

| J.P. Morgan | 87.12% | 85.43% | 85.56% |

| BlackRock | 86.13% | 84.21% | 84.37% |

| Vanguard | 80.21% | 78.60% | 78.46% |

| GMO | 2.07% | 2.79% | 2.46% |

| Charles Schwab | 91.77% | 90.32% | 90.85% |

| Invesco | 87.02% | 85.12% | 85.35% |

The success rates are stable across all three sampling regimes; the maximum cross-regime spread is 1.92 percentage points (BlackRock, default QMC versus scrambled). Default Sobol QMC runs slightly higher than pseudo-random on the five surviving forecasts — consistent with QMC's known tendency to underestimate tail-failure probability — so pseudo-random is the appropriate default for tail-sensitive outcomes.

Volatility & correlation matrix

Annual volatility per asset class: US equity 15.2%, international equity 18.0%, bonds 5.0%, real estate 15.0%, cash 1.0% (J.P. Morgan published values). Correlation matrix: J.P. Morgan published values, full 5×5. Held constant across all six return-forecast runs so that only the return assumption varies. The five other firms either don't publish a complete correlation matrix or use modestly different volatility estimates within typical empirical ranges (US equity 15–19%, bonds 5–7%); using one consistent set isolates the return-forecast variable.

Inflation

Deterministic 2.5% CPI applied uniformly to withdrawals across all runs. Stochastic inflation models (AR(1), regime-switching) are available in the QuantCalc engine and produce qualitatively similar conclusions, with slightly higher tail-failure rates under regime-switching. We chose deterministic for this piece to keep the comparison clean and the methodology reproducible by other researchers.

What this analysis does not model

- Guaranteed income floors (Social Security, pensions, annuities). This scenario is deliberately portfolio-only; adding any fixed income raises every success rate above, because less of the $40k/yr need is drawn from the portfolio. The calculator supports these inputs — they are simply not assumed here unless specified.

- Sequence-of-returns risk beyond what i.i.d. monthly returns naturally produce. The engine does not impose macro regimes or autocorrelation.

- Tax drag on withdrawals (no Roth/Traditional/taxable distinction at this layer).

- Healthcare cost shocks, long-term care events, or other lumpy out-of-distribution spending.

- Behavioral changes — actual retirees often dynamically adjust withdrawals in response to portfolio performance.

- Time-varying volatility (GARCH-style), fat-tailed return distributions (Student-t), or regime-shift correlation increases during crises. The QuantCalc engine supports these; this piece does not enable them.

Reproducibility

The full simulation outputs are available below as machine-readable downloads. Anyone with the QuantCalc free CLI or the public API can re-run the exact same scenario and get the same numbers (modulo random-seed differences in the pseudo-random regime).

{kind=link}

{kind=link}

To reproduce in QuantCalc, run a Monte Carlo simulation with these parameters:

{

"currentAge": 65,

"retirementAge": 65,

"endAge": 95,

"initialSavings": 1000000,

"monthlyWithdrawal": 3333.33,

"allocations": [0.45, 0.15, 0.40, 0.0, 0.0],

"numSimulations": 10000,

"adjustForInflation": true,

"useQMC": false,

"cme_source": "vanguard", // change per run

"correlations_source": "jpmorgan",

"volatility_source": "jpmorgan"

}Set cme_source to one of: jpmorgan, blackrock, vanguard, gmo, schwab, invesco. The resulting successRate and percentiles match the figures in this article within sampling noise.

FAQ

Why use 60/40 instead of Bengen's 50/50?

60/40 is the more common modern reference allocation for retirement and what most contemporary retirement calculators default to. Re-running the analysis at 50/50 (or 70/30) shifts the absolute numbers but not the ranking of forecasts or the qualitative conclusions. The terminal-balance spread tightens slightly at 50/50 because of the lower equity weight, but the GMO outlier persists.

Does the answer change at a 4.5% or 3.5% withdrawal rate?

Yes — and materially. Lowering the withdrawal to 3.5% improves every forecast's odds; raising it to 4.5% worsens them, and GMO remains a near-certain failure at any of these rates. Adding any guaranteed-income floor (Social Security, a pension) improves them further, because less of the annual need is drawn from the portfolio. Because the pseudo-random draws are unseeded, a precise per-rate figure is best generated live — run the withdrawal-rate sweep on your own inputs at quantcalc.app rather than relying on a single quoted number.

Why isn't there a "Historical 1926–2025" comparison?

Because adding it would distract from the main question — how do forward-looking forecasts treat the 4% rule? The historical rolling-window answer is well-known: Bengen-style backtests on actual US return sequences show effectively 100% 30-year survival at 4%. Monte Carlo resampling is a stricter test — it draws returns independently, without the mean reversion embedded in real sequences. For completeness, under the same 60/40 no-other-income plan with QuantCalc's historical 1926–2025 return and volatility inputs, the Monte Carlo success rate is 95.9%, with a median terminal balance of about $1.45M nominal — higher than any of the published forward-looking forecasts, but still short of a guarantee once the full withdrawal is drawn from the portfolio.

Disclosures & sources

Not financial advice. This piece is for research and educational purposes only. Individual retirement circumstances vary; consult a qualified advisor before making withdrawal-rate or allocation decisions.

Non-affiliation. QuantCalc is an independent educational tool. Not affiliated with, endorsed by, or sponsored by any referenced firm including BlackRock, J.P. Morgan, Vanguard, GMO, Schwab, Invesco, Morningstar, or Fidelity. Return assumptions are derived from publicly available research publications and widely-circulated public financial media. All trademarks belong to their respective owners.

Data licensing. The simulation outputs (data.json, summary.csv) are released under CC0 (public domain). Article text is released under CC-BY 4.0 with attribution to QuantCalc.

Reproducibility. Re-running this analysis requires the QuantCalc Monte Carlo engine (free CLI / web app at quantcalc.app) and one of the publicly-available CMEs above. The numbers in this article were regenerated with QuantCalc backend version 2.0.0 on 2026-07-10.

Methodology note (2026-07-10). These results reflect the QuantCalc engine as of 2026-07-10, whose withdrawal modeling assumes no supplemental income unless it is specified. This scenario carries no Social Security or pension, so the entire $40,000/yr inflation-adjusted withdrawal is met from the portfolio — which is what the "$1M, 60/40, $40k/yr withdrawals" description above intends. Earlier figures on this page were higher; the current numbers are the like-for-like result for a portfolio-only plan.

Found this useful? Run your own retirement plan against multiple forecasts at quantcalc.app. Or read more research: ACA cliff Monte Carlo (2026) · Three problems with the 4% rule · 2026 safe-withdrawal-rate research · Full simulation methodology.

Related research

Two companion Monte Carlo studies that extend the framework above:

- 510,000-path 51-State Retirement Monte Carlo (2026) — the state-tax companion. The 4% rule survives differently depending on residence: California retirees pay $167,580 more in 30-year state tax than Wyoming, with a 9.16pp lower success rate. Open dataset, CC-BY-4.0.

- Monte Carlo ACA Cliff 2026: $212k Cost to Early Retirees — what happens to the 4% withdrawal in the pre-Medicare bridge years when the 400% FPL cliff is back. 80,000-path study across four retiree profiles.