Social Security Tax Torpedo 2026: $1 Income, $0.85 Tax

Most retirees know Social Security benefits can be taxable. What catches people off guard is the tax torpedo — a zone where $1 of additional income causes up to $0.85 of your Social Security benefits to become newly taxable.

That means a retiree in the 12% federal bracket can face an effective marginal tax rate of 22.2% on their next dollar of IRA withdrawal. In the 22% bracket, the effective rate jumps to 40.7%. This isn't a theoretical problem — it hits millions of retirees every year, and the math got worse in 2026.

What Is the Social Security Tax Torpedo?

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

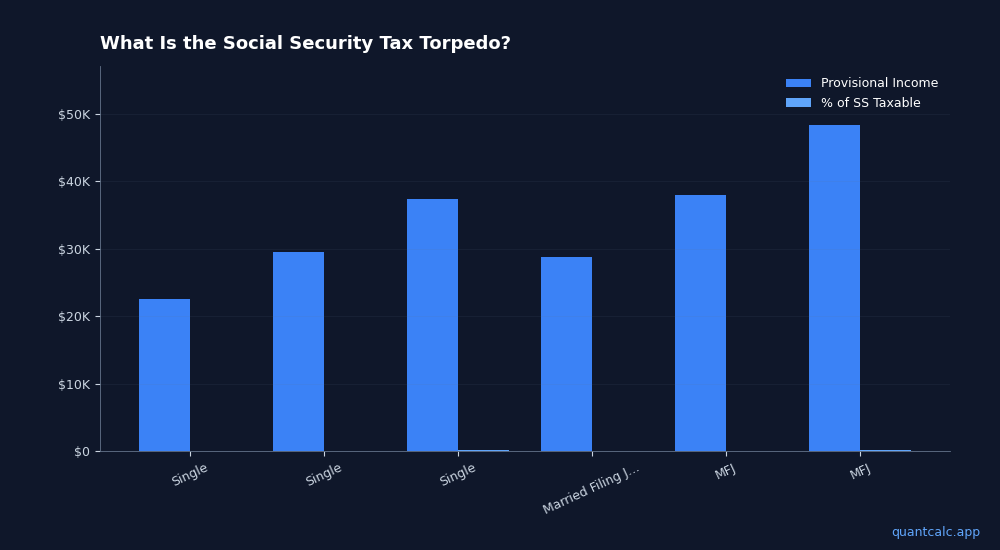

Try QuantCalc Free →Social Security taxation works on a two-tier system based on your provisional income:

Provisional Income = AGI + Tax-Exempt Interest + 50% of Social Security Benefits

| Filing Status | Provisional Income | % of SS Taxable |

|---|---|---|

| Single | Below $25,000 | 0% |

| Single | $25,000 – $34,000 | Up to 50% |

| Single | Above $34,000 | Up to 85% |

| Married Filing Jointly | Below $32,000 | 0% |

| MFJ | $32,000 – $44,000 | Up to 50% |

| MFJ | Above $44,000 | Up to 85% |

The "torpedo" happens in the transition zones. When you cross from the 50% tier into the 85% tier, each additional dollar of income doesn't just get taxed at your marginal rate — it also drags $0.85 of previously untaxed Social Security benefits into taxable income.

Run your own numbers in the free calculator →

Why 2026 Makes It Worse

The thresholds have never been adjusted for inflation. The $25,000/$32,000 and $34,000/$44,000 thresholds were set in 1984 and 1993 respectively. In 1984, $32,000 for a married couple was a comfortable middle-class income. In 2026, it catches nearly every retiree with any income beyond Social Security.

The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, made TCJA tax brackets permanent. Good news: rates stayed at 10-37% instead of reverting to higher pre-2017 levels. But the law left Social Security taxation thresholds completely untouched.

New in 2026: OBBBA did add a temporary $4,000 bonus senior standard deduction for filers age 65+, effective through 2028. This reduces the number of retirees who owe tax on their total income — but it does NOT change the provisional income thresholds that determine how much of your SS is taxable in the first place.

The Math That Surprises People

Consider a married couple, both 67, filing jointly:

- Social Security: $40,000/year combined

- Traditional IRA withdrawals: $30,000/year

- No other income

Provisional income: $30,000 (AGI from IRA) + $20,000 (50% of SS) = $50,000

At $50,000 provisional income, they're well into the 85% tier. Roughly $28,500 of their $40,000 in Social Security benefits is taxable.

Now imagine they withdraw an extra $5,000 from their IRA to cover an unexpected expense:

- The $5,000 gets taxed at their marginal rate (12%)

- PLUS $4,250 of additional Social Security becomes taxable (85% x $5,000)

- Total new taxable income: $9,250 from a $5,000 withdrawal

- Tax on that $9,250 at 12%: $1,110

- Effective tax rate on the $5,000 IRA withdrawal: 22.2%

They think they're in the 12% bracket. They're actually paying 22.2%. In the 22% bracket, this effect pushes the effective rate to 40.7%.

How the Torpedo Zone Looks Across Income Levels

For a married couple claiming $40,000 in SS benefits (2026):

| IRA Withdrawal | Provisional Income | SS Taxable | Federal Tax | Effective Rate |

|---|---|---|---|---|

| $10,000 | $30,000 | $0 | $0 | 0% |

| $20,000 | $40,000 | ~$6,800 | ~$680 | 3.4% |

| $30,000 | $50,000 | ~$28,500 | ~$3,420 | 11.4% |

| $40,000 | $60,000 | ~$34,000 | ~$5,660 | 14.2% |

| $50,000 | $70,000 | ~$34,000 | ~$7,860 | 15.7% |

The steepest jump happens between $20K and $30K in IRA withdrawals — that's the torpedo zone where each dollar pulls the most SS into taxation.

Five Strategies to Defuse the Torpedo

1. Roth Conversions Before Social Security Starts

Roth IRA withdrawals do NOT count toward provisional income. If you retire early (before age 62-67), you have a window to convert Traditional IRA funds to Roth at low tax rates. Each dollar converted now is a dollar that won't trigger the torpedo later.

This is the single most powerful torpedo avoidance strategy, and it works best for early retirees with 5-10 years before claiming Social Security. Our guide to Roth conversion ladders for early retirement covers the mechanics.

2. Manage Your Withdrawal Mix

Instead of pulling everything from your Traditional IRA, blend withdrawals across account types:

- Taxable account: Long-term capital gains may qualify for the 0% capital gains rate (up to $98,900 MFJ in 2026)

- Roth IRA: Tax-free, invisible to provisional income

- Traditional IRA: Only what's needed to fill low brackets

The tax-efficient withdrawal order isn't always "Traditional first" — in the torpedo zone, Roth-first may save more in total taxes.

3. Delay Social Security to Reduce the Window

Larger SS benefits from delaying (up to 124% of PIA at age 70) mean higher provisional income — but you collect for fewer years. The break-even math depends on your longevity expectations and other income sources. Our Social Security claiming age guide walks through the trade-offs.

4. Keep Provisional Income Below $32,000 (MFJ)

If you can keep provisional income under $32,000 for married filing jointly ($25,000 single), zero percent of your Social Security is taxable. This is achievable if most of your income comes from Roth accounts and you've done conversions during early retirement.

5. Use the OBBBA Senior Deduction While It Lasts

The new $4,000 senior deduction (2026-2028) doesn't change your provisional income, but it reduces your taxable income after SS is added. This can drop you into a lower bracket on the tax you do owe. Plan conversions and withdrawals to maximize this temporary benefit before it expires.

Model Your Exact Torpedo Exposure

The torpedo zone is different for every household — it depends on your SS benefit amount, other income sources, filing status, and which accounts you draw from.

Start with our free Tax Torpedo Calculator to see your marginal rate through the torpedo zone. QuantCalc's Monte Carlo retirement planner models Social Security taxation alongside your full retirement projection with 10,000 scenarios. For a hands-on approach, our Social Security Claiming Strategy Calculator includes a Tax Torpedo Analysis tab showing your exact exposure at 10 different income levels.

The Bottom Line

The Social Security tax torpedo is a design flaw frozen in place since 1984. Inflation has dragged millions of middle-income retirees into a tax trap that was originally meant for high earners. In 2026, with OBBBA locking in tax rates but leaving these thresholds untouched, strategic withdrawal planning isn't optional — it's the difference between a 12% effective rate and a 40% one.

Previously posted topics: last-minute-tax-moves-before-april-15, freelancer-vs-w2-tax-difference-2026, best-free-retirement-calculators-2026-comparison, side-hustle-tax-guide-2026, how-much-do-i-need-to-retire-math-2026, estimated-tax-payment-schedule-2026, when-to-claim-social-security-early-retirement-break-even, irs-underpayment-penalty-2026, 2026-tax-brackets-obbba-freelancers, self-employment-tax-calculator-2026, roth-conversion-ladder-early-retirement-2026