Bucket Strategy for Retirement: 3 Buckets to Weather Any Market

Size your three buckets

Bucket 1 (cash) and Bucket 2 (bonds) hold a set number of years of spending; Bucket 3 (growth) is whatever's left.

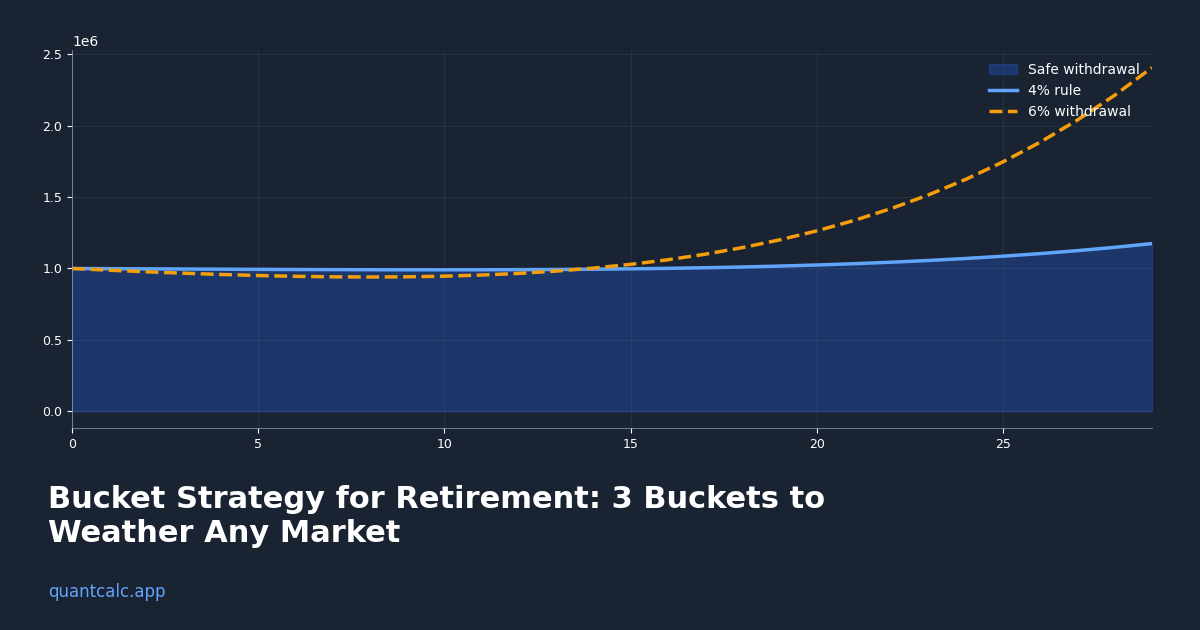

PRO models refilling the buckets and rebalancing across 10,000 market paths, so you can see how often Bucket 1 runs dry. Unlock it in the app →

Most retirement portfolios are managed as a single pool—60% stocks, 40% bonds, rebalance annually, hope for the best. But what if you're three years into retirement and stocks crash 40%? Suddenly you're forced to sell stocks at the bottom to cover living expenses.

Enter the bucket strategy: divide your portfolio into time-based segments, each with different asset allocations and purposes. Bucket 1 covers years 1-5 (cash/bonds), Bucket 2 covers years 6-15 (balanced), Bucket 3 covers years 16+ (aggressive growth).

This guide shows you exactly how to build a bucket strategy, when it makes sense, and whether it's actually better than a simple rebalanced portfolio (spoiler: the math says no, but the psychology says maybe).

What Is the Bucket Strategy?

Run your own numbers — FREE

10,000 Monte Carlo simulations. Forward-looking forecasts from BlackRock, JPMorgan, Vanguard, GMO, Schwab, Invesco. No account needed.

Try QuantCalc Free →The bucket strategy divides your retirement portfolio into three separate "buckets" based on when you'll need the money:

Bucket 1: Short-term (Years 1-5)

- Purpose: Fund living expenses for the next 5 years

- Allocation: 100% cash and short-term bonds (ultra-safe, no volatility)

- Amount: 5 years of expenses (e.g., $200k if spending $40k/year)

Bucket 2: Medium-term (Years 6-15)

- Purpose: Refill Bucket 1 after good market years

- Allocation: 50/50 stocks/bonds (balanced)

- Amount: 10 years of expenses ($400k)

Bucket 3: Long-term (Years 16+)

- Purpose: Growth for longevity, don't touch unless emergency

- Allocation: 80/20 or 70/30 stocks/bonds (aggressive)

- Amount: Remaining assets ($400k+)

Total example portfolio: $1M split into three buckets

Run your own numbers in the free calculator →

How the Bucket Strategy Works in Practice

Year 1: Spend from Bucket 1

- Withdraw $40k from Bucket 1 (cash/bonds)

- Don't touch Buckets 2 or 3

- Let Buckets 2 and 3 grow

Year 2: Good market year (stocks up 20%)

- Spend $40k from Bucket 1

- Refill Bucket 1: Sell $40k from Bucket 3 (stocks), move to Bucket 1

- Bucket 2 grows

- Bucket 3 shrinks slightly but still growing

Year 3: Bad market year (stocks down 30%)

- Spend $40k from Bucket 1

- Do NOT refill Bucket 1 (don't sell stocks at a loss)

- Let Buckets 2 and 3 recover

Years 4-5: Market recovers

- Continue spending from Bucket 1

- Once Bucket 3 has recovered, refill Bucket 1

The key rule: Only refill Bucket 1 after good market years. Never sell stocks during crashes.

The Psychology: Why the Bucket Strategy Feels Good

The bucket strategy is psychologically powerful, even if mathematically equivalent to a rebalanced portfolio.

What it provides:

1. Visible Safety

You can "see" 5 years of expenses sitting safely in cash/bonds. This is emotionally reassuring during market crashes.

Contrast with single-portfolio approach:

- 60/40 portfolio crashes 24% (60% stocks × -40% + 40% bonds × 0%)

- You're selling from a declining portfolio → Feels terrible

2. Prevents Panic Selling

Scenario: March 2020, stocks crash 35% in 3 weeks.

- Single portfolio approach: "My portfolio is down $300k! Should I sell before it gets worse?"

- Bucket approach: "Bucket 1 has 5 years of cash. I don't need to touch stocks for years. Let it recover."

The bucket strategy enforces discipline by design.

3. Clear Decision Rules

- Stocks up 20%? Refill Bucket 1.

- Stocks down 30%? Do nothing, live off Bucket 1.

No guesswork, no emotional decisions.

The Math: Is the Bucket Strategy Actually Better?

Short answer: No. It's mathematically equivalent to a balanced portfolio with systematic rebalancing.

Here's why:

Bucketing Is Just Asset Location

Bucket strategy:

- Bucket 1: $200k cash

- Bucket 2: $400k (50/50)

- Bucket 3: $400k (80/20)

Total allocation: ~55% stocks, 45% bonds (averaged across all buckets)

Single portfolio approach:

- $1M at 55/45 allocation

Mathematically, these are identical. The only difference is labeling and mental accounting.

Research Shows Minimal Performance Difference

Studies (Vanguard, Morningstar):

- Bucket strategies and rebalanced portfolios have nearly identical long-term returns

- Bucket strategies sometimes have slightly LOWER returns (due to cash drag in Bucket 1)

- Success rates (probability of not running out of money) are the same

Why use buckets then? Behavioral benefit. If it helps you stick to your plan during crashes, it's worth it.

You can test this equivalence yourself: model your 3-bucket plan as its blended overall allocation and compare success rates across thousands of simulated market paths.

(Learn more about rebalancing strategies)

How to Set Up a Bucket Strategy

Step 1: Calculate Your Annual Expenses

- Fixed expenses: Housing, insurance, utilities, food

- Discretionary: Travel, hobbies, dining out

- Total: e.g., $50,000/year

Step 2: Determine Bucket Sizes

Bucket 1 (Cash):

- 5 years of expenses (conservative) OR 3 years (moderate)

- Example: 5 × $50k = $250k

Bucket 2 (Balanced):

- 10 years of expenses

- Example: 10 × $50k = $500k

Bucket 3 (Growth):

- Remaining portfolio

- Example: $1.2M total - $250k - $500k = $450k

Step 3: Set Allocations

Bucket 1:

- 100% cash, money market, short-term bonds (1-2 year duration)

- Goal: Zero volatility

Bucket 2:

- 40-60% stocks, 40-60% bonds

- Example: 50/50

Bucket 3:

- 70-80% stocks, 20-30% bonds

- Example: 75/25

Step 4: Choose Specific Investments

Bucket 1:

- High-yield savings (4-5% as of 2026)

- Money market funds (VMMXX, SPAXX)

- Short-term bond ETF (SHV, VGSH)

Bucket 2:

- Balanced fund (VBAIX, Vanguard Balanced Index)

- OR: 50% VTI (total stock) + 50% BND (total bond)

Bucket 3:

- Stock-heavy fund (VTSAX, VTI)

- OR: 75% VTI + 25% BND

Step 5: Implement the Refill Rules

Annual review (January):

- Check Bucket 1 balance (how many years of expenses left?)

- Check Bucket 3 performance (up or down?)

- If Bucket 3 is up 10%+ AND Bucket 1 has <5 years: Refill Bucket 1

- If Bucket 3 is down: Do nothing, leave Bucket 1 alone

Spending:

- Withdraw from Bucket 1 monthly or quarterly

- Ignore Buckets 2 and 3 unless refilling

Modified Bucket Strategies

Two-Bucket Approach (Simpler)

Bucket 1: 5 years cash/bonds

Bucket 2: Everything else (70/30 stocks/bonds)

Pros: Simpler, fewer decisions

Cons: Less granular control

Four-Bucket Approach (More Complex)

Bucket 1: Years 1-3 (cash)

Bucket 2: Years 4-10 (bonds)

Bucket 3: Years 11-20 (balanced)

Bucket 4: Years 21+ (aggressive)

Pros: Even more tailored

Cons: Overkill for most retirees

Dynamic Bucket Sizing

Adjust bucket sizes based on market valuations:

- When stocks are expensive (P/E >25): Keep Bucket 1 larger (7 years)

- When stocks are cheap (P/E <15): Shrink Bucket 1 (3 years)

Why it works: You're giving yourself more time to wait out crashes when valuations are high (crashes more likely).

Bucket Strategy vs. Traditional Portfolio

| Feature | Bucket Strategy | Single Portfolio (60/40) |

|---|---|---|

| Complexity | Moderate (3 accounts) | Simple (1 account) |

| Rebalancing | Rule-based (refill after gains) | Calendar-based (annual) |

| Psychological comfort | High (visible 5-year safety) | Moderate |

| Returns | Slightly lower (cash drag) | Slightly higher |

| Sequence risk protection | Good (Bucket 1 shields from forced selling) | Moderate |

| Withdrawal strategy | Automated (always from Bucket 1) | Manual (sell proportionally or tax-optimize) |

| Tax efficiency | Harder (multiple accounts to track) | Easier |

Verdict: Bucket strategy is slightly more work, slightly lower returns, but psychologically easier for some retirees.

When the Bucket Strategy Makes Sense

Good fit for:

- Anxious investors who panic during market crashes

- Retirees with fixed expenses (need to know 5 years is "safe")

- People who want simple rules ("spend from Bucket 1, refill after gains")

- Early retirees (40-60 year horizon, need to protect against early sequence risk)

Not necessary for:

- Disciplined investors who can stick to a rebalancing plan during crashes

- Retirees with pensions/Social Security covering most expenses (portfolio is "extra")

- Those who prioritize tax efficiency (bucket strategy complicates tax-loss harvesting and asset location)

Common Bucket Strategy Mistakes

Mistake 1: Making Bucket 1 Too Large

If Bucket 1 is 10 years of expenses (100% cash), you're sacrificing $200-400k+ in long-term growth.

Optimal: 3-5 years max. Any more is unnecessary safety that costs returns.

Mistake 2: Never Refilling Bucket 1

If you follow the "only refill after gains" rule too strictly, you might never refill (especially during prolonged bear markets).

Solution: Set a minimum threshold. If Bucket 1 drops below 2 years, refill from Bucket 2 even if markets are down.

Mistake 3: Ignoring Taxes

Selling from Bucket 3 to refill Bucket 1 can trigger capital gains taxes.

Solution: Hold Bucket 3 in IRAs (tax-deferred accounts) or use tax-loss harvesting.

Mistake 4: Forgetting About Inflation

Bucket 1 in cash erodes 3%/year due to inflation. If you never refill it, purchasing power drops.

Solution: Refill Bucket 1 regularly (every 2-3 years after gains) to restore purchasing power.

Mistake 5: Over-Complicating With Too Many Buckets

Four or five buckets sound sophisticated but are a pain to manage.

Best practice: Stick with 2-3 buckets max.

Real-World Example: Bucket Strategy in Action

Meet George, age 65, $1.2M portfolio, $60k/year spending:

Setup:

- Bucket 1: $300k (5 years × $60k) in high-yield savings + short-term bonds

- Bucket 2: $450k (50/50 stocks/bonds)

- Bucket 3: $450k (75/25 stocks/bonds)

Year 1-2 (bull market):

- Spend $60k/year from Bucket 1 → Now $180k

- Bucket 3 grows to $540k (+20%)

- Action: Sell $120k from Bucket 3, refill Bucket 1 to $300k

Year 3 (crash, stocks down 35%):

- Spend $60k from Bucket 1 → Now $240k

- Bucket 3 drops to $300k

- Action: Do NOTHING. Bucket 1 still has 4 years left.

Year 4-5 (recovery):

- Spend $60k/year → Bucket 1 now $120k (2 years left)

- Bucket 3 recovers to $450k

- Action: Refill Bucket 1 to $300k

Result over 10 years:

- George never sold stocks during the crash (avoided locking in losses)

- He refilled Bucket 1 four times (every 2-3 years after gains)

- Portfolio grew from $1.2M to $1.8M despite $600k in withdrawals

- He slept well during the crash because Bucket 1 had 4 years of safety

Compare to single-portfolio approach:

- Same returns, same success rate

- BUT: George's psychological comfort was higher with buckets

How to Implement a Bucket Strategy Today

Option 1: DIY (Most Control)

- Open separate accounts at your brokerage for each bucket

- Label them: "Bucket 1 Cash," "Bucket 2 Balanced," "Bucket 3 Growth"

- Set calendar reminders to review annually

Option 2: Robo-Advisor

- Betterment and Wealthfront offer "goal-based" investing (similar to buckets)

- Automated rebalancing and withdrawals

- Cost: 0.25% annual fee

Option 3: Financial Advisor

- Advisors love bucket strategies (easy to explain to clients)

- They'll handle refilling, rebalancing, tax optimization

- Cost: 0.5-1% annual fee

Option 4: Target-Date Funds (Simplified Bucket)

- Hold a mix of target-date funds with different years

- Example: 20% in 2025 fund (near-cash), 30% in 2035 fund, 50% in 2055 fund

- Pros: Automatic glide path

- Cons: Less control, higher fees

The Bottom Line: Buckets Are for Psychology, Not Performance

The bucket strategy won't make you richer—it's mathematically equivalent to a balanced, rebalanced portfolio.

But if it helps you:

- Sleep better during market crashes

- Avoid panic selling

- Stick to your long-term plan

...then it's worth the slight extra complexity.

Best for: Anxious retirees who need to "see" safe money to stay disciplined during volatility.

Skip it if: You're comfortable with traditional rebalancing and can ignore market noise.

The hybrid approach: Keep 2-3 years of expenses in cash (mini Bucket 1) and invest the rest in a 60/40 or 70/30 portfolio. Best of both worlds—some psychological safety without overdoing the cash drag.

Ready to test whether a bucket strategy improves your retirement success? Model both approaches with QuantCalc and compare outcomes across thousands of market scenarios.

Further Reading:

- Retirement Spending Strategies: Beyond the 4% Rule

- Retirement Portfolio Rebalancing: When and How to Do It

- Retirement Asset Allocation by Age: The Glide Path Strategy

Frequently Asked Questions

The bucket strategy divides your retirement portfolio into three separate "buckets" based on when you'll need the money:

Short answer: No. It's mathematically equivalent to a balanced portfolio with systematic rebalancing.