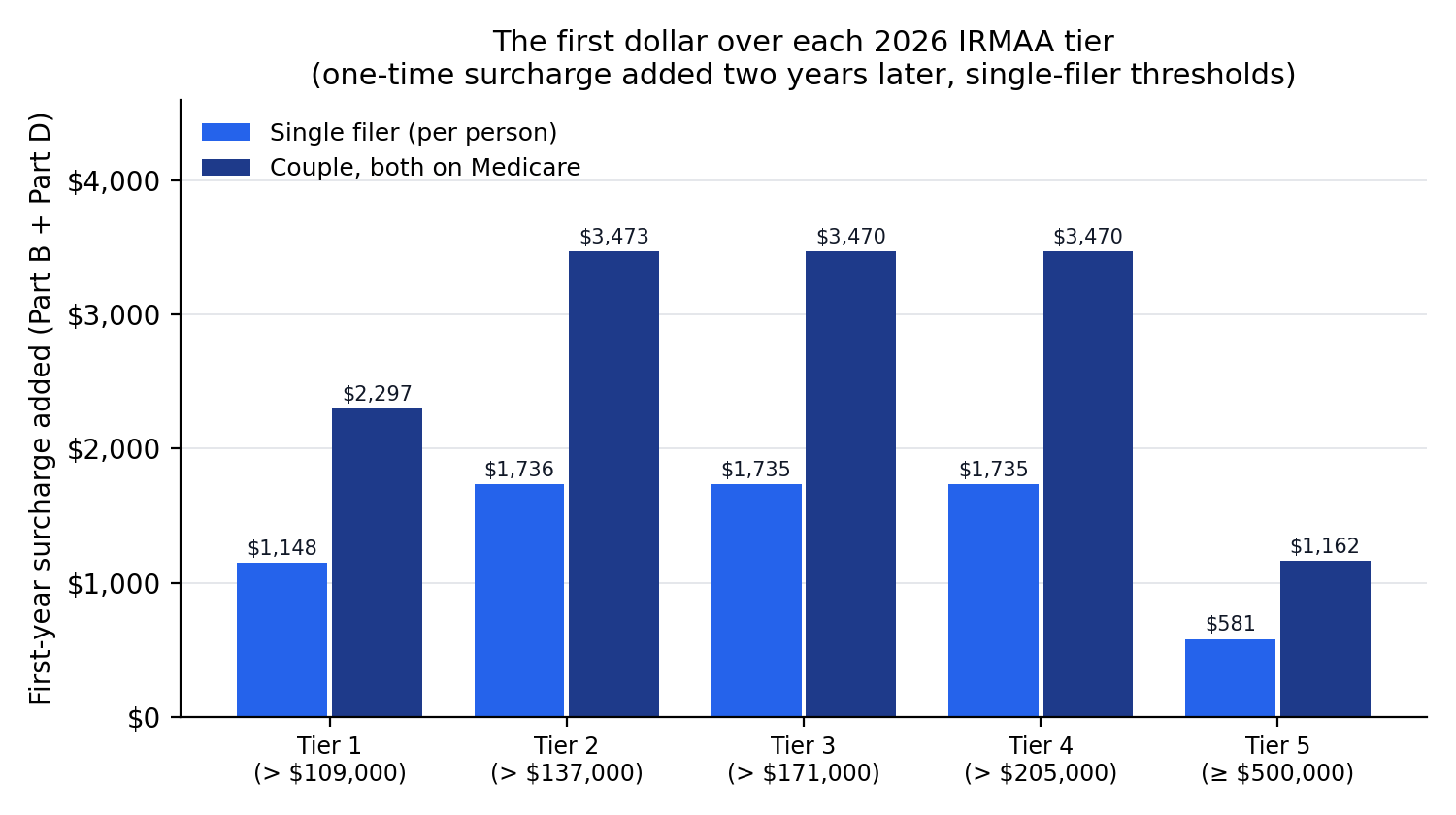

The first dollar over Tier 1: $1,148.40 a year For 2026, a single filer whose income (MAGI) tips just over $109,000 pays $1,148.40 in extra Medicare Part B and Part D premiums for the year; a couple who both have Medicare pays $2,296.80. It is a cliff, not a ramp: one dollar over the line triggers the whole year’s surcharge, billed two years later. That makes a small Roth conversion which just clips a new tier the most expensive kind — in our worked example a $5,000 conversion would need a future tax rate above 42.8% to pay off, while a $30,000 conversion that fills the same tier needs only 25.5%.

The question

A Roth conversion moves money from a traditional IRA into a Roth, paying income tax now so the balance grows and comes out tax-free later. For anyone on Medicare it carries a second, easy-to-miss price tag: the conversion adds to your modified adjusted gross income (MAGI), and once MAGI crosses an IRMAA threshold — the Income-Related Monthly Adjustment Amount — your Medicare Part B and Part D premiums jump for a full year. Medicare reads your MAGI from two years earlier, so a conversion this year shows up as higher premiums two years later.

The 2026 standard Part B premium is $202.90 a month. Above the thresholds, IRMAA adds a per-tier surcharge on top. We priced the first dollar over every 2026 tier — per person and per couple — measured the room between common income positions and the next tier, and then asked the planning question that matters: when a conversion has to cross a tier, when is it still the right move?

The 2026 IRMAA surcharge schedule

Surcharges apply per person. The thresholds below use the official convention — the surcharge for a tier applies only when MAGI is greater than that tier’s floor, so income landing exactly on a round threshold stays in the lower tier, with one exception: the top tier’s floor is inclusive. CMS states the highest band as “greater than or equal to” $500,000 (single) / $750,000 (married filing jointly), so a MAGI of exactly $500,000 already pays the top surcharge, and Tier 4 runs from over $205,000 to under $500,000. The annual figures are the Part B add-on plus the Part D add-on, times twelve; the couple column assumes both spouses have Medicare.

| Tier | Single MAGI | Married filing jointly MAGI | Part B add-on /mo | Part D add-on /mo | Annual surcharge, per person | Annual, couple (both on Medicare) |

|---|---|---|---|---|---|---|

| Tier 1 | Over $109,000 to $137,000 | Over $218,000 to $274,000 | $81.20 | $14.50 | $1,148.40 | $2,296.80 |

| Tier 2 | Over $137,000 to $171,000 | Over $274,000 to $342,000 | $202.90 | $37.50 | $2,884.80 | $5,769.60 |

| Tier 3 | Over $171,000 to $205,000 | Over $342,000 to $410,000 | $324.60 | $60.40 | $4,620.00 | $9,240.00 |

| Tier 4 | Over $205,000 and under $500,000 | Over $410,000 and under $750,000 | $446.30 | $83.30 | $6,355.20 | $12,710.40 |

| Tier 5 | $500,000 and above | $750,000 and above | $487.00 | $91.00 | $6,936.00 | $13,872.00 |

Married filing separately is different: it uses a compressed schedule, not this ladder. A separate filer with MAGI over $109,000 jumps straight to the fourth-tier add-on ($446.30 Part B plus $83.30 Part D per month), and MAGI of $391,000 and above reaches the top — only two steps, so the same income can cost a separate filer far more than a single filer.

What the first dollar over each tier costs

Because each tier is a cliff, the meaningful number is the jump when you cross into it. Crossing into Tier 1 adds the full Tier-1 surcharge; each higher crossing adds only the difference from the tier below. Per person, and per couple when both have Medicare (single-filer thresholds shown):

| Crossing | Added, per person | Added, couple (both on Medicare) | Total surcharge at that tier, per person |

|---|---|---|---|

| Into Tier 1 (MAGI over $109,000) | $1,148.40 | $2,296.80 | $1,148.40 |

| Into Tier 2 (MAGI over $137,000) | $1,736.40 | $3,472.80 | $2,884.80 |

| Into Tier 3 (MAGI over $171,000) | $1,735.20 | $3,470.40 | $4,620.00 |

| Into Tier 4 (MAGI over $205,000) | $1,735.20 | $3,470.40 | $6,355.20 |

| Into Tier 5 (MAGI of $500,000 and above) | $580.80 | $1,161.60 | $6,936.00 |

The pattern matters for conversion planning: the very first crossing (into Tier 1) is a large standalone step, the middle crossings each add roughly $1,736.40 per person, and the surcharge tops out at $6,936.00 a year. None of it is proportional to how far over the line you land — a dollar over and a thousand over cost the same.

How much room to the next tier?

The flip side of a cliff is the flat ground before it. If your income sits below a threshold, every dollar of conversion up to that threshold adds zero surcharge. Here is the room from a few common positions to the next IRMAA boundary, and what the next step would cost:

| Filer | Pre-conversion MAGI | Next tier floor | Room before crossing | Cost of the next step, per person |

|---|---|---|---|---|

| Single | $105,000 (below all tiers) | $109,000 | $4,000 | $1,148.40 |

| Single | $130,000 (in Tier 1) | $137,000 | $7,000 | $1,736.40 |

| Single | $165,000 (in Tier 2) | $171,000 | $6,000 | $1,735.20 |

| Couple (MFJ) | $210,000 (below all tiers) | $218,000 | $8,000 | $1,148.40 |

| Couple (MFJ) | $265,000 (in Tier 1) | $274,000 | $9,000 | $1,736.40 |

| Couple (MFJ) | $335,000 (in Tier 2) | $342,000 | $7,000 | $1,735.20 |

This “fill the tier” room is the cheapest conversion space you have: a single filer at $105,000 can convert $4,000 with no IRMAA at all before the first cliff.

When is crossing a tier still worth it?

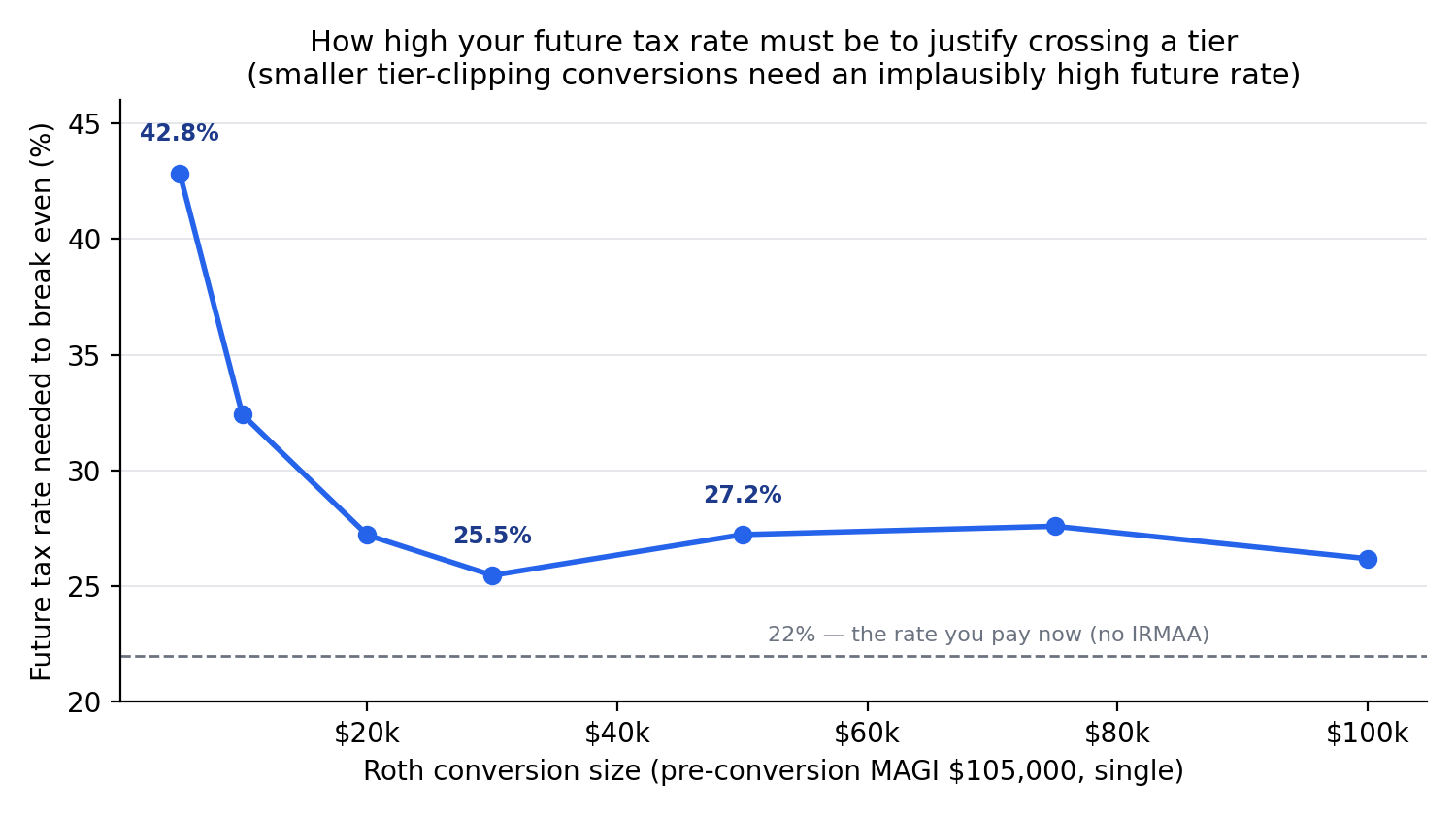

Sometimes you want to convert more than the room allows — to shrink future required minimum distributions (RMDs), which begin at age 75, or to move money while today’s tax rate is low. A conversion that crosses a tier is worth it when the tax rate you would otherwise pay later is high enough to outweigh the one-time surcharge. Because the surcharge is a flat dollar amount, its bite per converted dollar shrinks as the conversion grows — so the break-even future tax rate falls fast with size.

Worked example: a single filer, age 65, with a pre-conversion MAGI of $105,000, converting at a 22% marginal rate today, money growing at 5% real to age 90 (assumptions in Methodology). The “break-even future rate” is the tax rate your later withdrawals would need to face for the conversion to come out ahead once the IRMAA surcharge is counted:

| Conversion | Ending MAGI | Tier reached | IRMAA surcharge (one year) | Surcharge as % of conversion | Break-even future rate | Worth it? |

|---|---|---|---|---|---|---|

| $5,000 | $110,000 | Tier 1 | $1,148.40 | 23.0% | 42.8% | Rarely |

| $10,000 | $115,000 | Tier 1 | $1,148.40 | 11.5% | 32.4% | Rarely |

| $20,000 | $125,000 | Tier 1 | $1,148.40 | 5.7% | 27.2% | Only if future rate is high |

| $30,000 | $135,000 | Tier 1 | $1,148.40 | 3.8% | 25.5% | Only if future rate is high |

| $50,000 | $155,000 | Tier 2 | $2,884.80 | 5.8% | 27.2% | Only if future rate is high |

| $75,000 | $180,000 | Tier 3 | $4,620.00 | 6.2% | 27.6% | Only if future rate is high |

| $100,000 | $205,000 | Tier 3 | $4,620.00 | 4.6% | 26.2% | Only if future rate is high |

Two lessons fall out. First, size dominates: the same Tier-1 crossing that demands an implausible 42.8% future rate on a $5,000 conversion needs only 25.5% on a $30,000 one. Second, stop inside your tier: filling Tier 1 up to its ceiling keeps the break-even at 25.5%, but spilling a little into Tier 2 pushes the surcharge up and the break-even back to 27.2%. The worst case in the full grid is a small conversion that clips a mid-tier boundary — there a one-year surcharge of $3,472.80 eats 34.7% of the converted amount.

One rate-side nuance for tax years 2025–2028: a 65+ filer inside the OBBBA senior-deduction phase-out band (MAGI over $75,000 single / $150,000 married filing jointly, until the $6,000-per-filer deduction is exhausted) also loses 6 cents of that deduction per converted dollar, making the true marginal rate about 1.06× the bracket rate — add roughly 1.3 percentage points to the “rate now” and break-even columns while a conversion sits in that band.

What it implies for your conversion plan

- Know your room first. Convert up to the top of your current IRMAA tier before you consider crossing — that space carries no surcharge at all.

- If you cross, cross with size. A flat-dollar surcharge spread over a large conversion is minor; spread over a sliver it can exceed a fifth of the converted amount. Small tier-clipping conversions are the ones to avoid.

- Match the crossing to your future rate. Crossing a tier pays off only when the rate your later RMDs would face clears the break-even rate — roughly your current rate plus the surcharge spread across the conversion.

Plan your conversion around the tiers

The Roth Conversion Planner sizes the conversion that fills your current IRMAA tier, prices the next crossing, and weighs it against your future required distributions — with your own income and balances.

Open the Roth Conversion Planner →Or explore year-by-year conversions in the Roth Conversion Optimizer →

Methodology

The IRMAA schedule is the 2026 Medicare Part B and Part D announcement from the Centers for Medicare & Medicaid Services (published in the Federal Register, 2025-11-19), with a standard Part B premium of $202.90 a month. Each tier’s annual surcharge is its Part B add-on plus its Part D add-on, times twelve. Married-filing-jointly thresholds are the paired figures; married-filing-separately uses the compressed schedule described above. The couple figures assume both spouses are enrolled in Part B and Part D.

The lifetime comparison prices a one-time Roth conversion against leaving the same dollars in a traditional IRA. The full conversion compounds tax-free in the Roth; income tax on the conversion and the one-time IRMAA surcharge are paid from outside cash; the traditional-IRA alternative grows the same dollars and is taxed on withdrawal at a future rate. Under this convention the outside balances cancel, and a conversion that crosses a tier is net-positive exactly when the future rate exceeds a break-even equal to the current rate plus the surcharge amortized over the conversion. Documented assumptions and limitations:

- Two-year lookback. 2026 IRMAA is set from 2024 MAGI (20 CFR 418.1105); a one-time conversion is charged one year of surcharge, not a recurring one. Conversion ladders repeat the surcharge each year they keep MAGI in the tier.

- Reference thresholds. The 2026 tier dollar figures are held constant as the reference grid. They are inflation-indexed and will differ for future lookback years; the structure of the findings does not depend on the exact future numbers.

- Growth and horizon. 5% real growth, start age 65, RMDs from age 75, horizon age 90; all amounts in real (today’s) dollars.

- Single-rate tax side. The later withdrawal is taxed at one marginal rate standing in for the blended rate RMDs would face. Full bracket stacking, the taxation of Social Security benefits, and state income tax are outside the model; taxable-account tax drag is ignored (neutral to the comparison).

- Senior-deduction interaction (2025–2028). The “rate now” is the statutory bracket rate. For tax years 2025–2028, a filer aged 65 or older whose conversion runs through the OBBBA §70103 senior-deduction phase-out band (MAGI over $75,000 single / $150,000 married filing jointly, until the $6,000-per-filer deduction is exhausted) loses 6 cents of deduction per converted dollar there, so the effective marginal rate in that band is about 1.06× the bracket rate — roughly 1.3 percentage points above the 22%/24% cases shown. The surcharge grid itself is tax-rate-agnostic and unaffected.

- Out of scope. The Net Investment Income Tax, the Part B late-enrollment penalty, employer-coverage exceptions, and life-changing-event IRMAA appeals (Form SSA-44) are not modeled.

Reproducibility

The full per-scenario results are published as open data under a CC0 public-domain dedication: results.csv (every conversion scenario — surcharge, cost share, and break-even rate — across 84 rows) and summary.json (headline figures). The engine (irmaa-roth-1.1.0, seed 20260710) is deterministic: two runs produce byte-identical output. Sources: 2026 CMS Medicare Part B/D IRMAA announcement (2025-11-19); IRMAA two-year lookback (20 CFR 418.1105); MAGI definition (20 CFR 418.1010); RMD age 73–75 under the SECURE 2.0 Act. See our methodology for the shared assumptions used across QuantCalc research.

FAQ

What is IRMAA and when does a Roth conversion trigger it?

IRMAA is the Income-Related Monthly Adjustment Amount — an extra charge added to your Medicare Part B and Part D premiums once your modified adjusted gross income (MAGI) rises above set thresholds. A Roth conversion adds the converted amount to your adjusted gross income, so a large conversion can push your MAGI over an IRMAA threshold. Because Medicare uses your MAGI from two years earlier, a conversion done in one year raises your Medicare premiums two years later, for that one year.

How much does crossing the first 2026 IRMAA tier cost?

For 2026, a single filer whose MAGI goes over $109,000 pays an extra $1,148.40 for the year in combined Part B and Part D surcharges (an $81.20 Part B add-on plus a $14.50 Part D add-on, each times twelve months). For a married couple who both have Medicare, the same crossing costs $2,296.80 because each spouse pays the surcharge. It is a cliff: one dollar of MAGI over the threshold triggers the full year's surcharge.

Is married filing separately treated the same as single for IRMAA?

No. Married filing separately uses a compressed schedule, not the single-filer ladder. For 2026, a separate filer with MAGI over $109,000 jumps straight to the fourth-tier surcharge ($446.30 Part B plus $83.30 Part D per month), and MAGI of $391,000 and above reaches the top tier. There are only two surcharge steps, so separate filers can face much larger surcharges at the same income than single filers.

When is a conversion that crosses an IRMAA tier still worth it?

The surcharge is a flat one-year dollar amount, so the cost per converted dollar shrinks as the conversion grows. A tiny conversion that just clips a new tier is punished hardest: in this study a single filer converting $5,000 across the first tier would need a future tax rate above 42.8% to come out ahead, while a $30,000 conversion that fills the same tier needs only about 25.5%. The practical rule is to convert up to the top of your current tier before crossing into the next one, and to cross a boundary only when the rate you would otherwise pay later clearly exceeds the break-even rate.

How can I model my own conversion and IRMAA?

The Roth Conversion Planner lets you enter your own income, IRA balance, and filing status and see the conversion size that fills your current IRMAA tier, the surcharge of crossing into the next one, and the long-run trade-off against future required minimum distributions. It runs in the browser with no signup.

Published 2026-07-09 by QuantCalc Research. Educational research, not financial or tax advice. Related: Roth Conversion Planner · the Roth conversion gap-years window · the ACA subsidy cliff.